Advertisement

Unveiling Ashmore Group And 2 Other Top Undervalued Small Caps On UK With Insider Buying

Simply Wall St

Reviewed by Simply Wall St

In the current climate, the UK market is grappling with challenges as evidenced by the recent declines in both the FTSE 100 and FTSE 250 indices, largely influenced by weak trade data from China and its impact on commodity prices. Amidst this backdrop, investors are increasingly seeking opportunities within small-cap stocks that may offer potential for growth despite broader market uncertainties. Identifying such stocks requires a focus on those with strong fundamentals and resilience in challenging economic conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Headlam Group | NA | 0.2x | 36.19% | ★★★★★☆ |

| Sabre Insurance Group | 11.7x | 1.5x | 9.28% | ★★★★☆☆ |

| iomart Group | 26.9x | 0.7x | 27.03% | ★★★★☆☆ |

| Optima Health | NA | 1.2x | 36.80% | ★★★★☆☆ |

| Dr. Martens | 25.3x | 0.9x | 3.25% | ★★★☆☆☆ |

| Telecom Plus | 18.5x | 0.7x | 28.58% | ★★★☆☆☆ |

| Treatt | 19.9x | 1.9x | 47.27% | ★★★☆☆☆ |

| Gooch & Housego | 42.3x | 1.0x | 30.51% | ★★★☆☆☆ |

| Reach | 6.6x | 0.5x | -129.39% | ★★★☆☆☆ |

| THG | NA | 0.4x | -1160.07% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

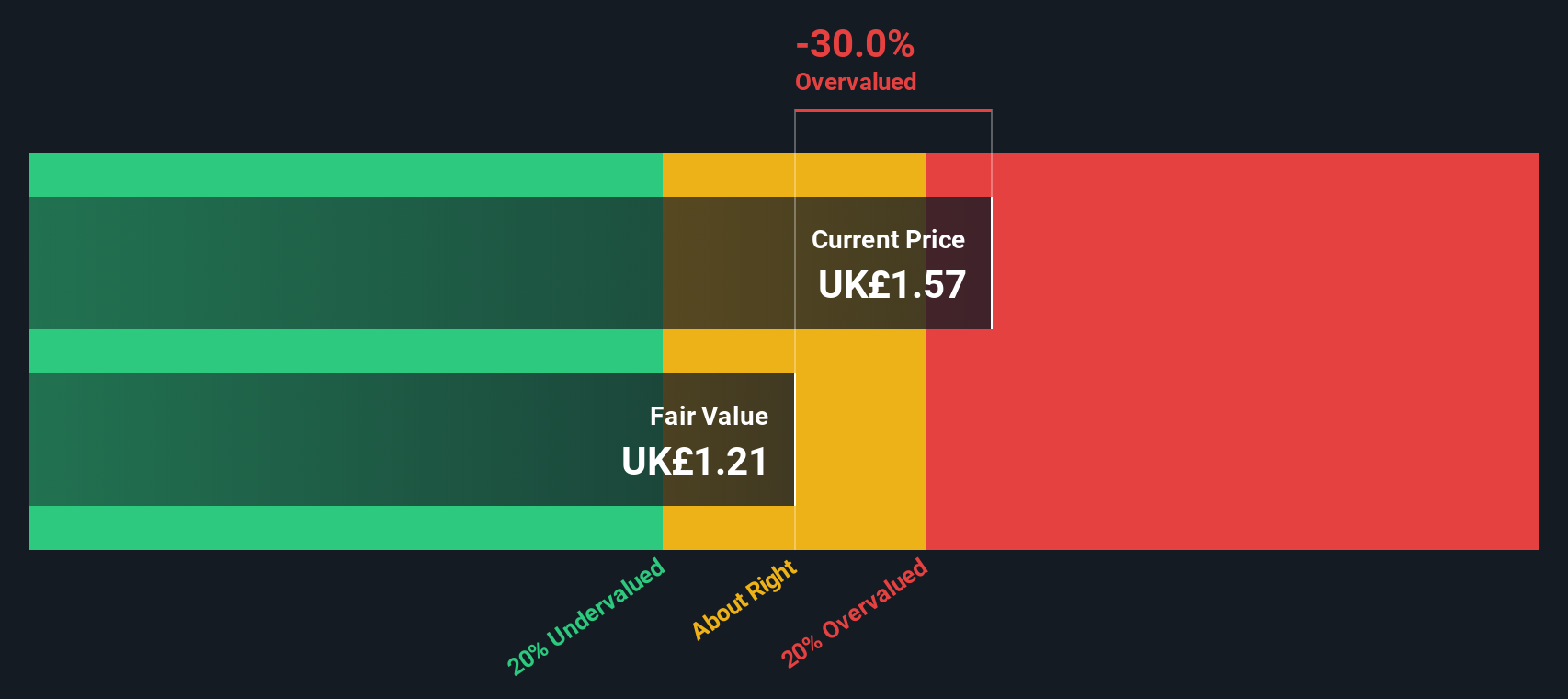

Ashmore Group (LSE:ASHM)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Ashmore Group is a specialist investment manager focused on emerging markets, with operations centered around providing investment management services and a market capitalization of approximately £1.55 billion.

Operations: Ashmore Group's revenue primarily comes from investment management services, with a recent revenue figure of £186.8 million. The company has experienced fluctuations in its net income margin, which was most recently recorded at 50.16%. Operating expenses have been relatively stable around £29.8 million, while the gross profit margin has shown a declining trend, reaching 54.44% in the latest period.

PE: 11.7x

Ashmore Group, a UK-based investment manager, recently declared a final dividend of £0.12 per share for the fiscal year ending June 2024. Despite its small size in the market, insider confidence is evident with recent share purchases by company leaders in November 2024. However, potential investors should note that earnings are projected to decline by 5.8% annually over the next three years due to reliance on external borrowing for funding.

- Take a closer look at Ashmore Group's potential here in our valuation report.

Examine Ashmore Group's past performance report to understand how it has performed in the past.

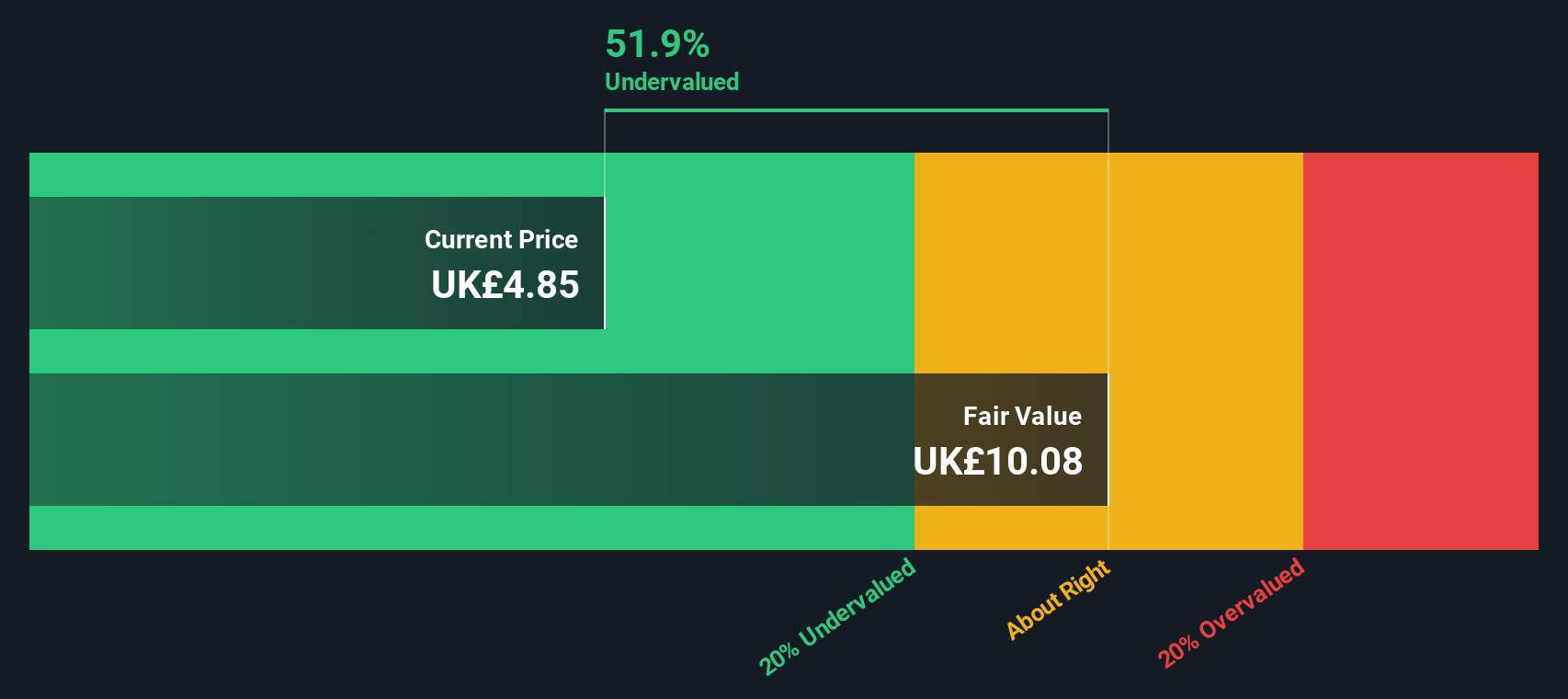

Bloomsbury Publishing (LSE:BMY)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bloomsbury Publishing is a UK-based independent publishing house known for its diverse range of operations, including consumer and non-consumer segments like special interest and academic & professional publishing, with a market cap of approximately £0.89 billion.

Operations: Revenue is primarily driven by the Non-Consumer segments, with Academic & Professional contributing significantly. The gross profit margin has shown an increasing trend, reaching 57.16% in August 2024. Operating expenses are substantial, led by General & Administrative and Sales & Marketing costs.

PE: 14.5x

Bloomsbury, a UK-based publisher with a strong financial footing, is actively seeking acquisitions to leverage its position. Recent half-year results reveal sales of £179.8 million and net income of £16.6 million, reflecting growth from the previous year. The company increased its interim dividend by 5% to 3.89 pence per share, showcasing commitment to shareholder returns despite potential earnings decline over the next three years due to reliance on external borrowing for funding.

- Click to explore a detailed breakdown of our findings in Bloomsbury Publishing's valuation report.

Explore historical data to track Bloomsbury Publishing's performance over time in our Past section.

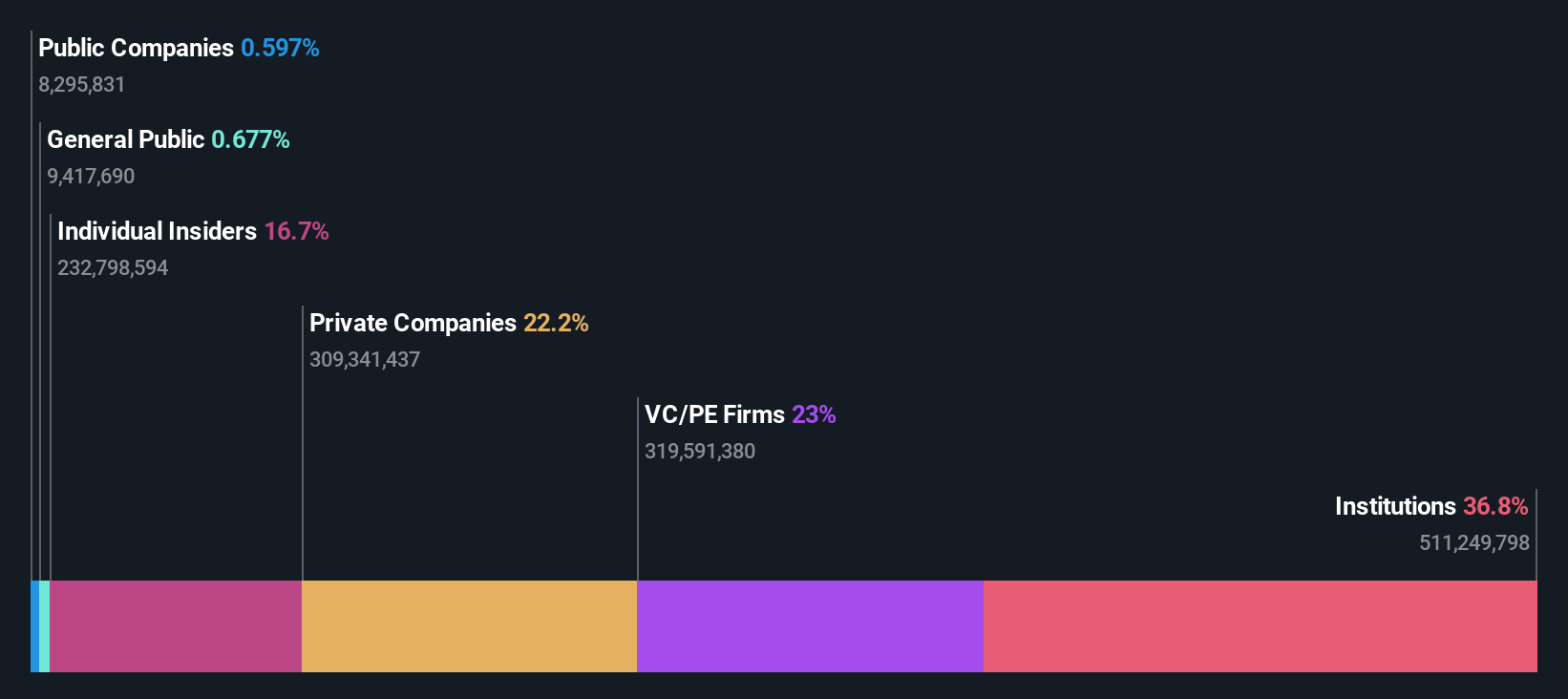

THG (LSE:THG)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: THG operates as a global consumer brand group with divisions in beauty, nutrition, and technology services, and has a market capitalization of £1.26 billion.

Operations: THG generates revenue primarily from its Beauty, Ingenuity, and Nutrition segments, with the Beauty segment contributing the largest share. The company has experienced fluctuations in its gross profit margin, which reached 41.83% as of December 2023. Operating expenses are significant and include substantial allocations to sales and marketing as well as general and administrative costs.

PE: -3.3x

THG, a smaller UK-based company, has seen insider confidence with Charles Allen purchasing 542,000 shares recently. Despite reporting a net loss of £121 million for the first half of 2024 and facing shareholder dilution due to recent equity offerings totaling over £100 million, the company is exploring strategic alternatives like demerging THG Ingenuity. The business remains unprofitable and highly volatile but anticipates revenue growth of 3.53% annually. Future prospects hinge on restructuring efforts to enhance shareholder value.

Taking Advantage

- Dive into all 30 of the Undervalued UK Small Caps With Insider Buying we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if THG might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:THG

THG

Operates as an online retailer in the United Kingdom, the United States, Europe, and internationally.

Undervalued with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor