Advertisement

- United Kingdom

- /

- Entertainment

- /

- AIM:DEVO

Devolver Digital Full Year 2024 Earnings: EPS Misses Expectations

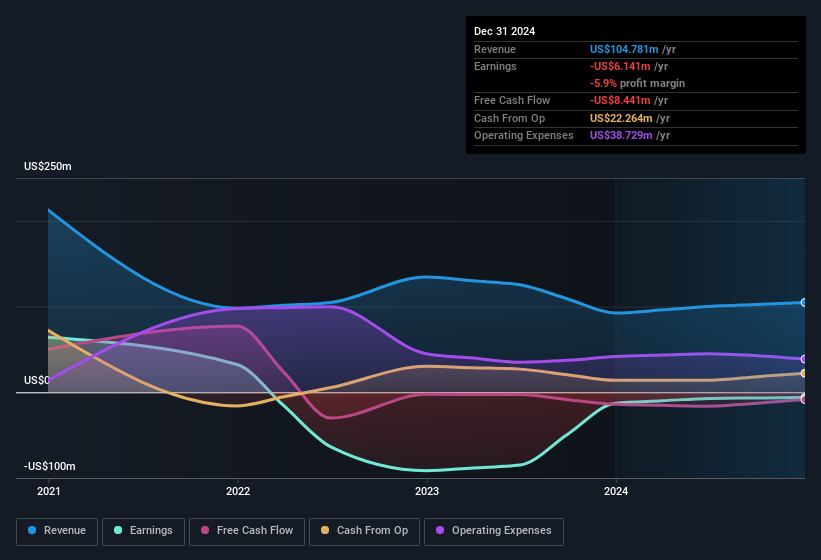

Devolver Digital (LON:DEVO) Full Year 2024 Results

Key Financial Results

- Revenue: US$104.8m (up 14% from FY 2023).

- Net loss: US$6.14m (loss narrowed by 52% from FY 2023).

- US$0.013 loss per share (improved from US$0.029 loss in FY 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Devolver Digital EPS Misses Expectations

Revenue was in line with analyst estimates. Earnings per share (EPS) missed analyst estimates by 33%.

Looking ahead, revenue is forecast to grow 8.2% p.a. on average during the next 3 years, compared to a 4.5% growth forecast for the Entertainment industry in the United Kingdom.

Performance of the British Entertainment industry.

The company's shares are up 3.8% from a week ago.

Balance Sheet Analysis

While earnings are important, another area to consider is the balance sheet. We have a graphic representation of Devolver Digital's balance sheet and an in-depth analysis of the company's financial position.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:DEVO

Devolver Digital

Develops and publishes digital video games for PC, console, and mobile platforms in Europe, North America, the Asia Pacific, Latin America, the United Kingdom, the Middle East, and North Africa.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

156 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AB

Abhishekgarg on Pidilite Industries ·

High quality compounder, but current valuation leaves limited margin of safety.

Fair Value:₹1.31k2.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PA

Paddy_Ho on PaySauce ·

NZ company with gumption aims to provide services to SMEs across The Ditch

Fair Value:NZ$0.3623.6% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JC

JCAPITAL on Security Bank ·

YoY Percentage Growth: +5.8%

Fair Value:₱22169.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0