Advertisement

What does Mondi plc's (LON:MNDI) Balance Sheet Tell Us About Its Future?

Want to participate in a short research study? Help shape the future of investing tools and receive a $20 prize!

The size of Mondi plc (LON:MNDI), a UK£9.1b large-cap, often attracts investors seeking a reliable investment in the stock market. Market participants who are conscious of risk tend to search for large firms, attracted by the prospect of varied revenue sources and strong returns on capital. However, the key to extending previous success is in the health of the company’s financials. I will provide an overview of Mondi’s financial liquidity and leverage to give you an idea of Mondi’s position to take advantage of potential acquisitions or comfortably endure future downturns. Note that this information is centred entirely on financial health and is a high-level overview, so I encourage you to look further into MNDI here.

Check out our latest analysis for Mondi

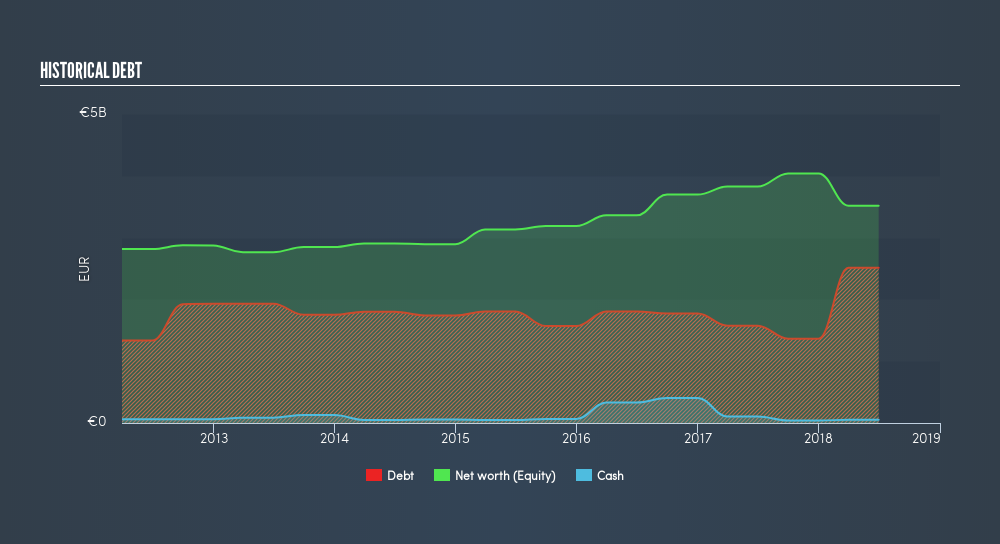

Does MNDI produce enough cash relative to debt?

Over the past year, MNDI has ramped up its debt from €1.6b to €2.5b , which accounts for long term debt. With this rise in debt, MNDI's cash and short-term investments stands at €54m , ready to deploy into the business. On top of this, MNDI has produced cash from operations of €1.2b over the same time period, resulting in an operating cash to total debt ratio of 50%, signalling that MNDI’s operating cash is sufficient to cover its debt. This ratio can also be interpreted as a measure of efficiency as an alternative to return on assets. In MNDI’s case, it is able to generate 0.5x cash from its debt capital.

Can MNDI meet its short-term obligations with the cash in hand?

With current liabilities at €1.6b, the company has been able to meet these commitments with a current assets level of €2.3b, leading to a 1.39x current account ratio. Generally, for Forestry companies, this is a reasonable ratio since there's a sufficient cash cushion without leaving too much capital idle or in low-earning investments.

Is MNDI’s debt level acceptable?

With a debt-to-equity ratio of 71%, MNDI can be considered as an above-average leveraged company. This isn’t surprising for large-caps, as equity can often be more expensive to issue than debt, plus interest payments are tax deductible. Accordingly, large companies often have an advantage over small-caps through lower cost of capital due to cheaper financing. By measuring how many times MNDI’s earnings can cover interest payments, we can evaluate whether its level of debt is sustainable or not. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. For MNDI, the ratio of 21.51x suggests that interest is comfortably covered. High interest coverage is seen as a responsible and safe practice, which highlights why most investors believe large-caps such as MNDI is a safe investment.

Next Steps:

MNDI’s high cash coverage means that, although its debt levels are high, the company is able to utilise its borrowings efficiently in order to generate cash flow. Since there is also no concerns around MNDI's liquidity needs, this may be its optimal capital structure for the time being. This is only a rough assessment of financial health, and I'm sure MNDI has company-specific issues impacting its capital structure decisions. You should continue to research Mondi to get a better picture of the large-cap by looking at:

- Future Outlook: What are well-informed industry analysts predicting for MNDI’s future growth? Take a look at our free research report of analyst consensus for MNDI’s outlook.

- Valuation: What is MNDI worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether MNDI is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:MNDI

Mondi

Engages in the manufacture and sale of packaging and paper solutions in Africa, Western Europe, Emerging Europe, Russia, North America, South America, Asia, and Australia.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor