Mondi (LON:MNDI) Is Reinvesting At Lower Rates Of Return

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Having said that, from a first glance at Mondi (LON:MNDI) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Mondi, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

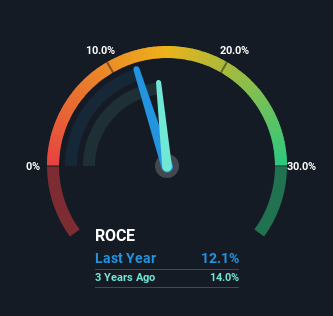

0.12 = €972m ÷ (€10b - €2.2b) (Based on the trailing twelve months to June 2023).

So, Mondi has an ROCE of 12%. That's a relatively normal return on capital, and it's around the 13% generated by the Forestry industry.

View our latest analysis for Mondi

Above you can see how the current ROCE for Mondi compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Mondi.

The Trend Of ROCE

When we looked at the ROCE trend at Mondi, we didn't gain much confidence. Around five years ago the returns on capital were 18%, but since then they've fallen to 12%. On the other hand, the company has been employing more capital without a corresponding improvement in sales in the last year, which could suggest these investments are longer term plays. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

What We Can Learn From Mondi's ROCE

Bringing it all together, while we're somewhat encouraged by Mondi's reinvestment in its own business, we're aware that returns are shrinking. Unsurprisingly then, the total return to shareholders over the last five years has been flat. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

If you'd like to know more about Mondi, we've spotted 3 warning signs, and 1 of them is potentially serious.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you're looking to trade Mondi, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:MNDI

Mondi

Engages in the manufacture and sale of packaging and paper solutions in Africa, Western Europe, Emerging Europe, Russia, North America, South America, Asia, and Australia.

Flawless balance sheet slight.

Similar Companies

Market Insights

Community Narratives