Advertisement

- United Kingdom

- /

- Basic Materials

- /

- LSE:BREE

We Think The Compensation For Breedon Group plc's (LON:BREE) CEO Looks About Right

Key Insights

- Breedon Group will host its Annual General Meeting on 29th of April

- CEO Rob Wood's total compensation includes salary of UK£662.0k

- Total compensation is similar to the industry average

- Over the past three years, Breedon Group's EPS grew by 6.1% and over the past three years, the total shareholder return was 23%

Performance at Breedon Group plc (LON:BREE) has been reasonably good and CEO Rob Wood has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 29th of April. Based on our analysis of the data below, we think CEO compensation seems reasonable for now.

See our latest analysis for Breedon Group

How Does Total Compensation For Rob Wood Compare With Other Companies In The Industry?

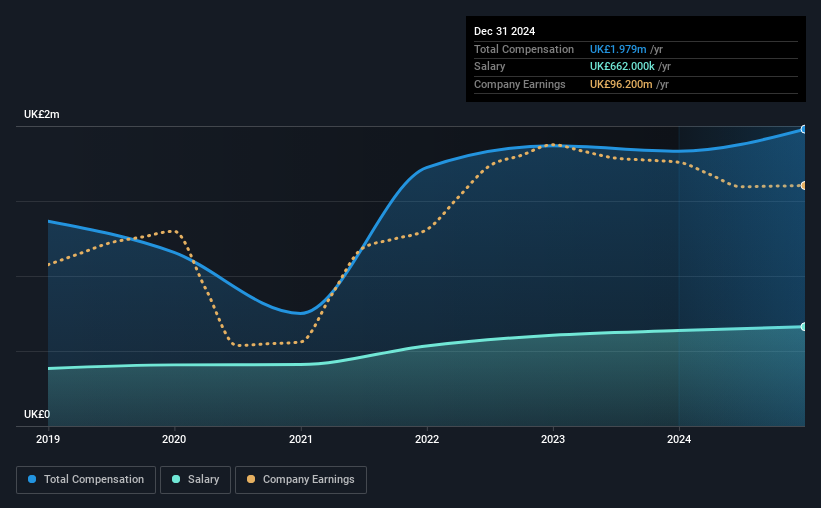

Our data indicates that Breedon Group plc has a market capitalization of UK£1.5b, and total annual CEO compensation was reported as UK£2.0m for the year to December 2024. Notably, that's an increase of 8.0% over the year before. While we always look at total compensation first, our analysis shows that the salary component is less, at UK£662k.

On examining similar-sized companies in the British Basic Materials industry with market capitalizations between UK£746m and UK£2.4b, we discovered that the median CEO total compensation of that group was UK£2.8m. This suggests that Breedon Group remunerates its CEO largely in line with the industry average. What's more, Rob Wood holds UK£2.1m worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£662k | UK£636k | 33% |

| Other | UK£1.3m | UK£1.2m | 67% |

| Total Compensation | UK£2.0m | UK£1.8m | 100% |

On an industry level, around 47% of total compensation represents salary and 53% is other remuneration. In Breedon Group's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Breedon Group plc's Growth Numbers

Over the past three years, Breedon Group plc has seen its earnings per share (EPS) grow by 6.1% per year. Its revenue is up 6.0% over the last year.

We'd prefer higher revenue growth, but we're happy with the modest EPS growth. So there are some positives here, but not enough to earn high praise. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Breedon Group plc Been A Good Investment?

Breedon Group plc has served shareholders reasonably well, with a total return of 23% over three years. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. Despite the pleasing results, we still think that any proposed increases to CEO compensation will be examined based on a case by case basis and linked to performance outcomes.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for Breedon Group that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Breedon Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BREE

Breedon Group

Engages in the quarrying, manufacture, and sale of construction materials and building products primarily in the United Kingdom and internationally.

Very undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor