Advertisement

- United Kingdom

- /

- Chemicals

- /

- AIM:HAYD

Haydale Graphene Industries (LON:HAYD) Has Debt But No Earnings; Should You Worry?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Haydale Graphene Industries plc (LON:HAYD) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Haydale Graphene Industries

How Much Debt Does Haydale Graphene Industries Carry?

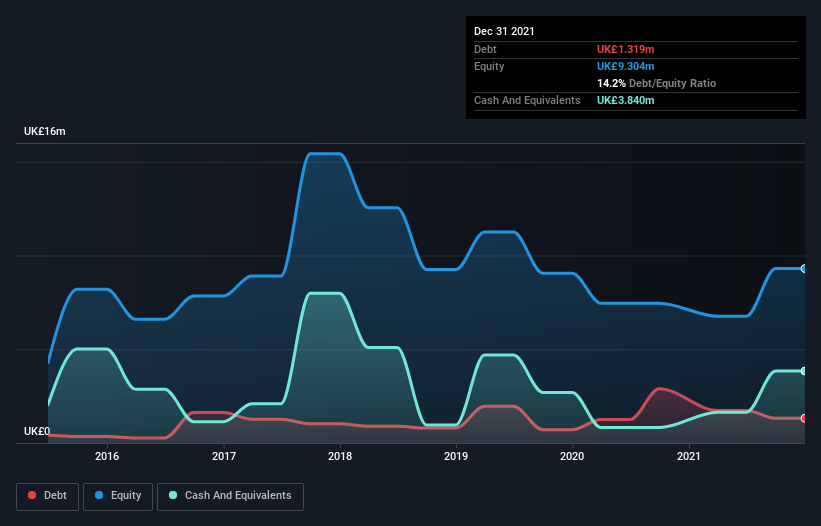

You can click the graphic below for the historical numbers, but it shows that Haydale Graphene Industries had UK£1.32m of debt in December 2021, down from UK£1.73m, one year before. But on the other hand it also has UK£3.84m in cash, leading to a UK£2.52m net cash position.

A Look At Haydale Graphene Industries' Liabilities

Zooming in on the latest balance sheet data, we can see that Haydale Graphene Industries had liabilities of UK£1.71m due within 12 months and liabilities of UK£4.81m due beyond that. On the other hand, it had cash of UK£3.84m and UK£1.52m worth of receivables due within a year. So it has liabilities totalling UK£1.15m more than its cash and near-term receivables, combined.

Given Haydale Graphene Industries has a market capitalization of UK£27.8m, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Haydale Graphene Industries boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Haydale Graphene Industries can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Haydale Graphene Industries had a loss before interest and tax, and actually shrunk its revenue by 2.1%, to UK£2.8m. We would much prefer see growth.

So How Risky Is Haydale Graphene Industries?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Haydale Graphene Industries had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through UK£2.3m of cash and made a loss of UK£3.9m. Given it only has net cash of UK£2.52m, the company may need to raise more capital if it doesn't reach break-even soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 6 warning signs with Haydale Graphene Industries (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Haydale Graphene Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:HAYD

Haydale Graphene Industries

Through its subsidiaries, engages in the design, development, and commercialization of advanced materials using graphene and other nanomaterials in United Kingdom, Europe, the United States, China, Thailand, South Korea, Japan, and internationally.

Medium-low risk with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets