Advertisement

- United Kingdom

- /

- Chemicals

- /

- AIM:DCTA

Investors Aren't Entirely Convinced By Directa Plus Plc's (LON:DCTA) Revenues

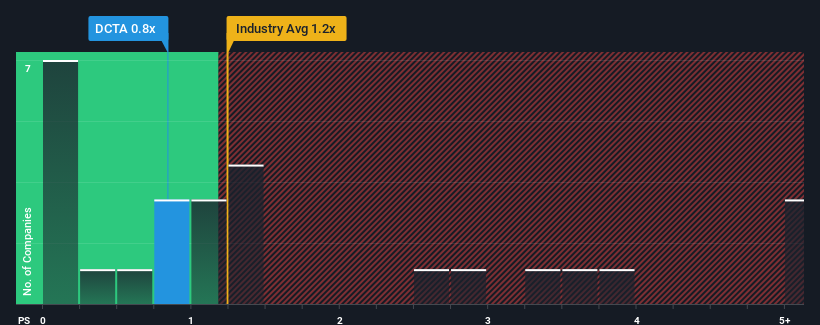

With a median price-to-sales (or "P/S") ratio of close to 1.2x in the Chemicals industry in the United Kingdom, you could be forgiven for feeling indifferent about Directa Plus Plc's (LON:DCTA) P/S ratio of 0.8x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Directa Plus

How Directa Plus Has Been Performing

With revenue that's retreating more than the industry's average of late, Directa Plus has been very sluggish. It might be that many expect the dismal revenue performance to revert back to industry averages soon, which has kept the P/S from falling. If you still like the company, you'd want its revenue trajectory to turn around before making any decisions. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

Keen to find out how analysts think Directa Plus' future stacks up against the industry? In that case, our free report is a great place to start.How Is Directa Plus' Revenue Growth Trending?

Directa Plus' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 6.1%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 23% overall rise in revenue. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 5.3% as estimated by the sole analyst watching the company. Meanwhile, the industry is forecast to moderate by 15%, which indicates the company should perform better regardless.

In light of this, the fact Directa Plus' P/S sits in line with the majority of other companies is unanticipated but certainly not shocking. Even though the company may outperform the industry, shrinking revenues are unlikely to lead to a stable P/S long-term. Even just maintaining these prices could be difficult to achieve as the weak outlook is already weighing down the shares.

The Key Takeaway

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Despite Directa Plus' analyst forecasts being a less shaky outlook than the rest of the industry, its P/S is a bit lower than we expected. Even though it's revenue prospects are better than the wider industry, we assume there are several risk factors might be placing downward pressure on the P/S, bringing it in line with the industry average. Amidst challenging industry conditions, a key concern is whether the company can sustain its superior revenue growth trajectory. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Plus, you should also learn about these 5 warning signs we've spotted with Directa Plus.

If you're unsure about the strength of Directa Plus' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:DCTA

Directa Plus

Manufactures and sells graphene-based products for industrial and commercial applications in Italy, Romania, and internationally.

Slight risk with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor