- United Kingdom

- /

- Retail Distributors

- /

- LSE:INCH

3 UK Dividend Stocks Yielding Up To 4.8%

Reviewed by Simply Wall St

The United Kingdom's FTSE 100 index recently experienced a downturn, influenced by weak trade data from China, highlighting the interconnectedness of global markets and the challenges facing economies striving to recover post-pandemic. In this climate of uncertainty, dividend stocks can offer a measure of stability and potential income for investors seeking to navigate these turbulent times.

Top 10 Dividend Stocks In The United Kingdom

| Name | Dividend Yield | Dividend Rating |

| James Latham (AIM:LTHM) | 5.94% | ★★★★★★ |

| Impax Asset Management Group (AIM:IPX) | 7.99% | ★★★★★☆ |

| 4imprint Group (LSE:FOUR) | 3.13% | ★★★★★☆ |

| OSB Group (LSE:OSB) | 9.39% | ★★★★★☆ |

| Plus500 (LSE:PLUS) | 6.41% | ★★★★★☆ |

| Man Group (LSE:EMG) | 6.33% | ★★★★★☆ |

| Big Yellow Group (LSE:BYG) | 3.80% | ★★★★★☆ |

| Dunelm Group (LSE:DNLM) | 6.98% | ★★★★★☆ |

| DCC (LSE:DCC) | 3.99% | ★★★★★☆ |

| Grafton Group (LSE:GFTU) | 3.68% | ★★★★★☆ |

Click here to see the full list of 58 stocks from our Top UK Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

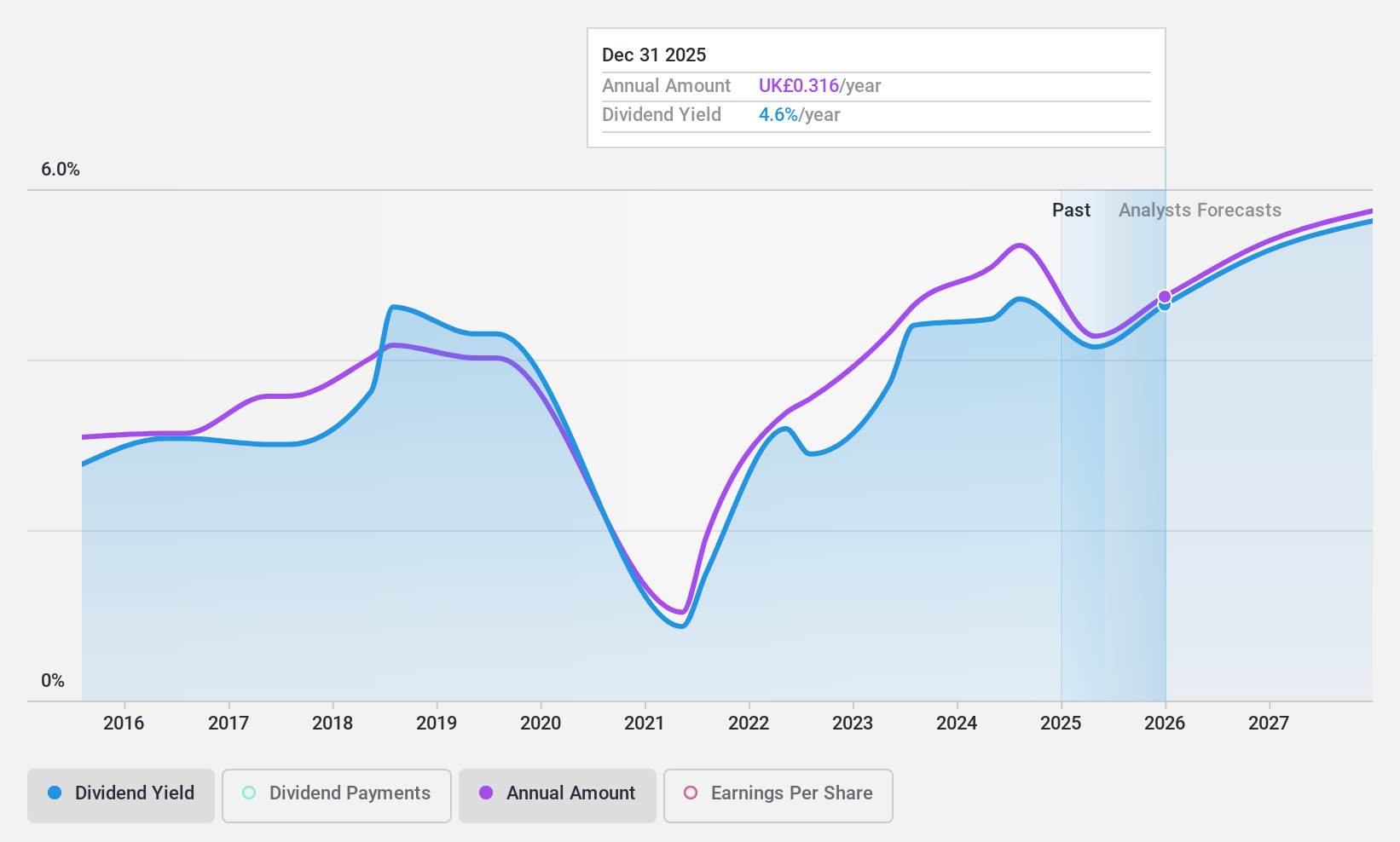

Helios Underwriting (AIM:HUW)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Helios Underwriting plc, along with its subsidiaries, offers shareholders limited liability investment opportunities in the Lloyd’s insurance market in the UK and has a market cap of £133.41 million.

Operations: Helios Underwriting plc generates its revenue primarily through Syndicate Participation (£258.32 million) and Investment Management (£4.62 million) in the Lloyd’s insurance market.

Dividend Yield: 3.2%

Helios Underwriting has experienced significant earnings growth, with revenue increasing to £132.64 million for the half year ended June 2024. Despite a low dividend yield of 3.21%, its dividends are well-covered by earnings and cash flows, reflecting a sustainable payout ratio of 25.3% and cash payout ratio of 8.2%. However, dividend payments have been volatile over the past decade, impacting reliability for investors seeking stable income streams.

- Dive into the specifics of Helios Underwriting here with our thorough dividend report.

- Our valuation report here indicates Helios Underwriting may be undervalued.

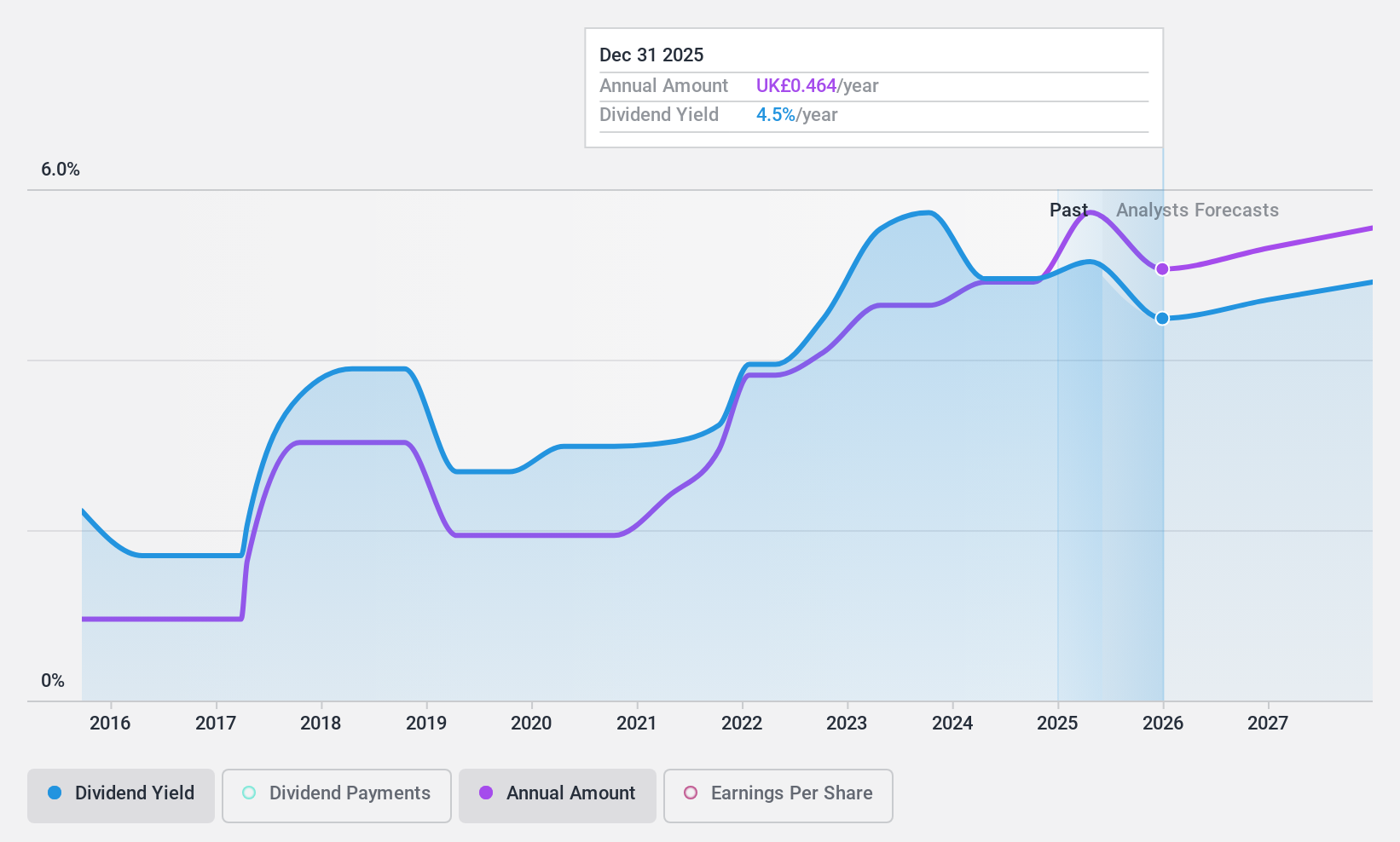

M.P. Evans Group (AIM:MPE)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: M.P. Evans Group PLC operates through its subsidiaries in the ownership and development of oil palm plantations in Indonesia and Malaysia, with a market cap of £487.66 million.

Operations: The company's revenue primarily comes from its plantation operations in Indonesia, amounting to $336.59 million.

Dividend Yield: 4.6%

M.P. Evans Group has shown robust earnings growth, with net income rising to US$30.08 million for the half year ended June 2024, supporting a 20% increase in its interim dividend to 15 pence per share. Despite past volatility in dividend payments, the current payout is well-covered by earnings and cash flows, with payout ratios of 48.9% and 33.3% respectively. The company is trading at a good value relative to peers and analysts anticipate further price appreciation.

- Unlock comprehensive insights into our analysis of M.P. Evans Group stock in this dividend report.

- The valuation report we've compiled suggests that M.P. Evans Group's current price could be quite moderate.

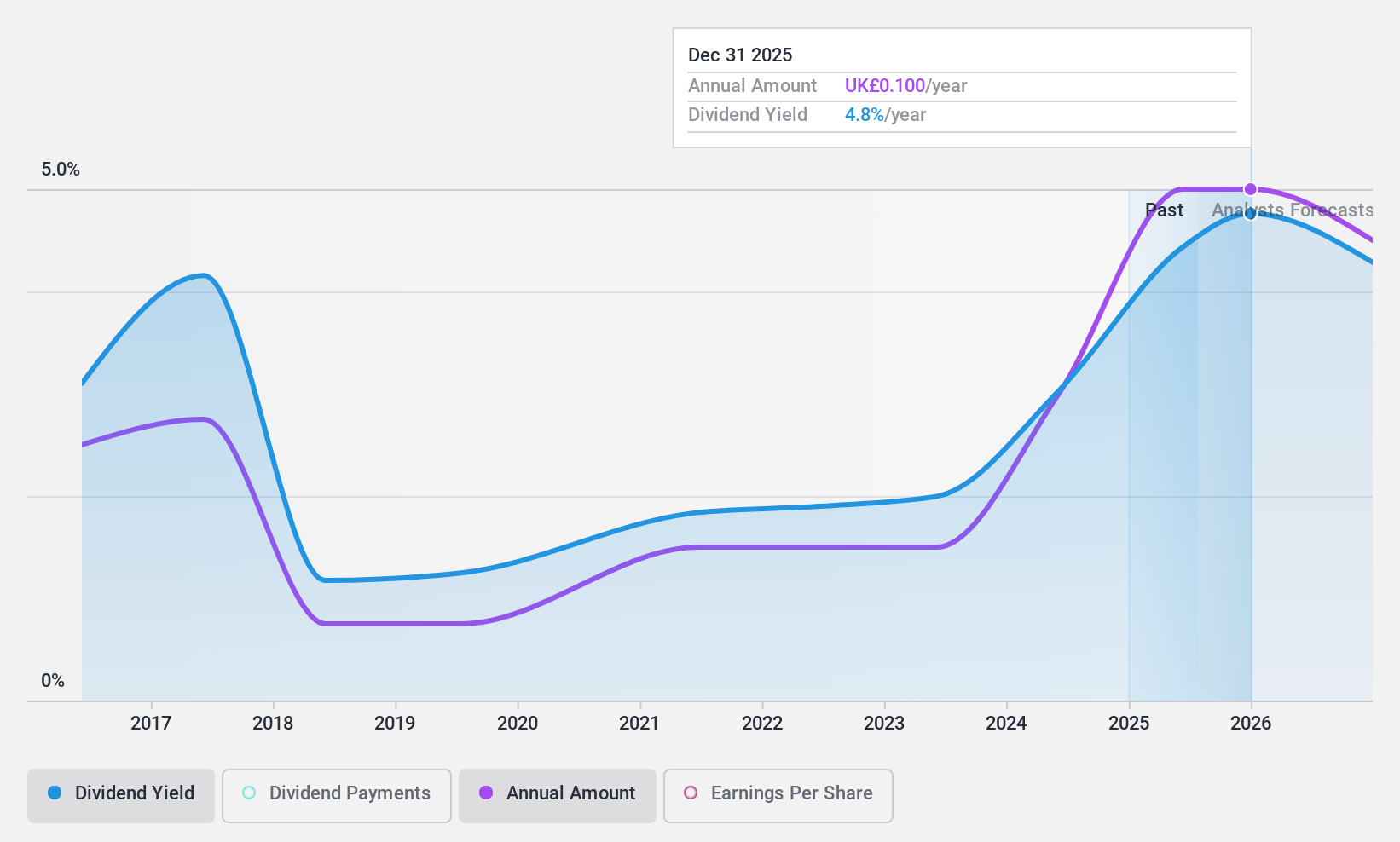

Inchcape (LSE:INCH)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Inchcape plc operates as an automotive distributor and retailer with a market cap of £2.96 billion.

Operations: Inchcape plc generates its revenue from several segments: £3.07 billion from Distribution in APAC, £3.44 billion from Distribution in the Americas, and £2.75 billion from Distribution in Europe & Africa.

Dividend Yield: 4.8%

Inchcape's dividend history has been unreliable, with volatility over the past decade, but current payouts are well-covered by earnings and cash flows, with a payout ratio of 52.5%. Despite trading at a significant discount to estimated fair value and good relative value compared to peers, the dividend yield is below top-tier UK market payers. Recent third-quarter revenue reached £2.2 billion amid ongoing acquisition plans, which may impact future cash outflows towards mid-2025.

- Get an in-depth perspective on Inchcape's performance by reading our dividend report here.

- Our expertly prepared valuation report Inchcape implies its share price may be lower than expected.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 55 Top UK Dividend Stocks now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:INCH

Very undervalued with solid track record and pays a dividend.