- United Kingdom

- /

- Software

- /

- AIM:GBG

3 UK Stocks That May Be Undervalued By Up To 20.8%

Reviewed by Simply Wall St

As the FTSE 100 and FTSE 250 indices face downward pressure due to weak trade data from China, investors in the United Kingdom are navigating a challenging market environment. In such conditions, identifying undervalued stocks can be crucial, as they may offer potential value opportunities despite broader economic uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Gaming Realms (AIM:GMR) | £0.37 | £0.73 | 49.1% |

| Fevertree Drinks (AIM:FEVR) | £7.10 | £13.12 | 45.9% |

| GlobalData (AIM:DATA) | £2.02 | £3.71 | 45.6% |

| Barratt Redrow (LSE:BTRW) | £4.29 | £7.35 | 41.6% |

| On the Beach Group (LSE:OTB) | £1.716 | £3.01 | 42.9% |

| Informa (LSE:INF) | £8.596 | £15.41 | 44.2% |

| Videndum (LSE:VID) | £2.54 | £4.61 | 44.9% |

| Foxtons Group (LSE:FOXT) | £0.60 | £1.03 | 41.9% |

| St. James's Place (LSE:STJ) | £9.035 | £16.34 | 44.7% |

| Genel Energy (LSE:GENL) | £0.881 | £1.58 | 44.1% |

Here we highlight a subset of our preferred stocks from the screener.

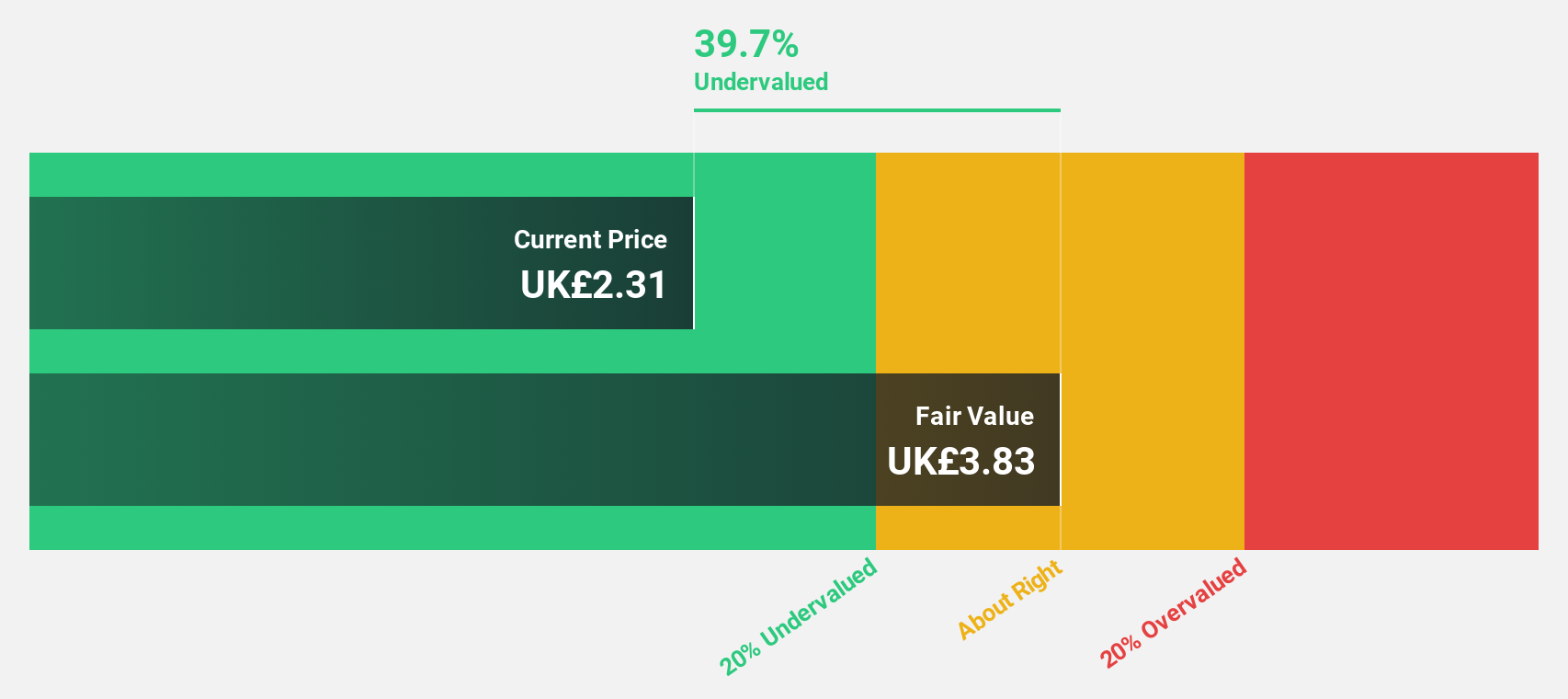

GB Group (AIM:GBG)

Overview: GB Group plc, along with its subsidiaries, offers identity data intelligence products and services across the United Kingdom, the United States, Australia, and internationally, with a market cap of £958.55 million.

Operations: The company's revenue segments include £38.14 million from fraud solutions, £159.78 million from identity services, and £83.94 million from location-based offerings.

Estimated Discount To Fair Value: 20.8%

GB Group plc's recent earnings report shows a return to profitability with net income of £1.58 million, contrasting last year's loss. The stock is currently trading at approximately 20.8% below its estimated fair value of £4.8, highlighting potential undervaluation based on cash flows. Despite low forecasted Return on Equity, projected earnings growth of 36.6% annually outpaces the UK market average, while revenue growth is also expected to exceed market rates at 6.9%.

- Our expertly prepared growth report on GB Group implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of GB Group here with our thorough financial health report.

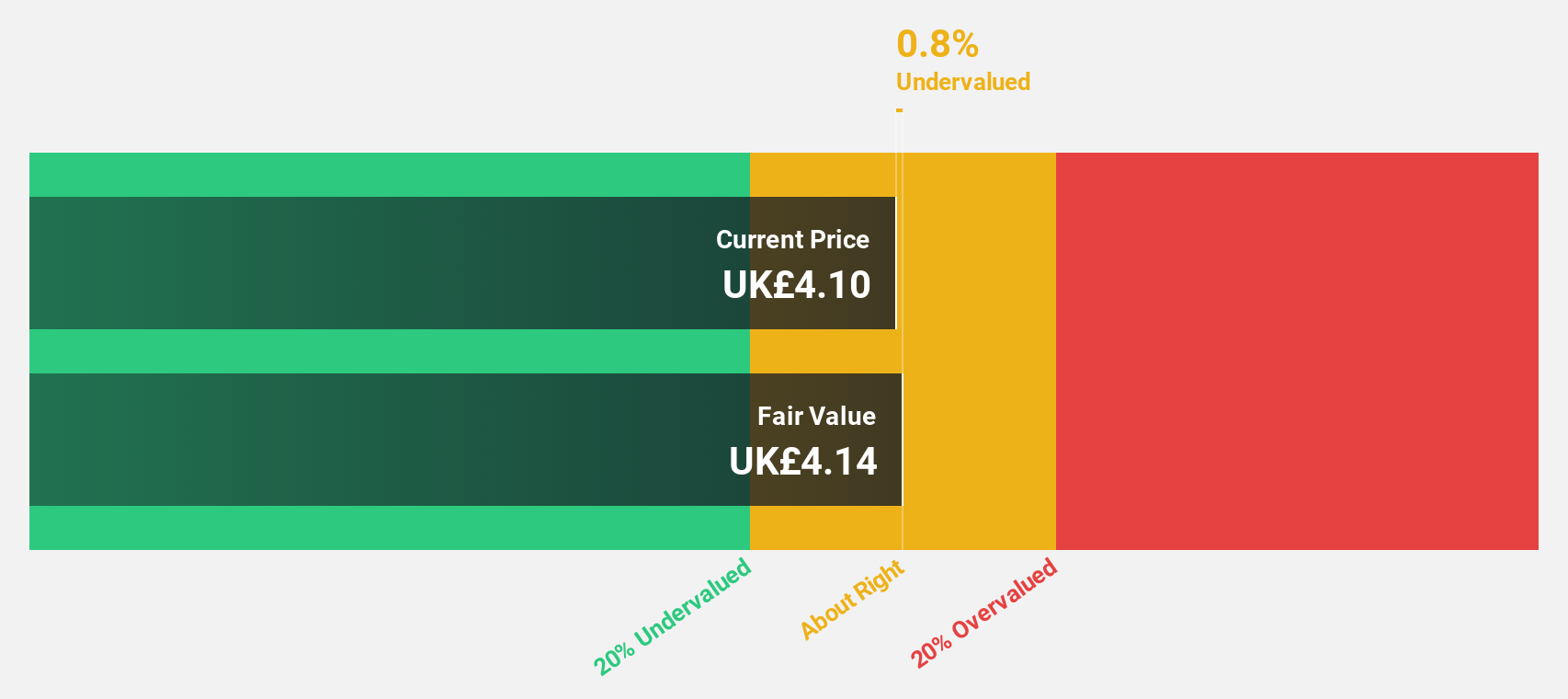

Tristel (AIM:TSTL)

Overview: Tristel plc develops, manufactures, and sells infection prevention products in the United Kingdom, Australia, Germany, Western Europe, and internationally with a market cap of £200.31 million.

Operations: The company's revenue is primarily derived from Hospital Medical Device Decontamination (£36.34 million) and Hospital Environmental Surface Disinfection (£3.44 million).

Estimated Discount To Fair Value: 10.6%

Tristel's recent earnings report highlights a net income increase to £6.49 million, with the stock trading at 10.6% below its estimated fair value of £4.7. Earnings grew by 45.5% over the past year, and future revenue growth is projected at 10.5% annually, outpacing the UK market average of 3.6%. Despite this growth potential, significant insider selling has been noted recently, and dividends are not well covered by earnings, indicating some financial caution is warranted.

- Insights from our recent growth report point to a promising forecast for Tristel's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Tristel.

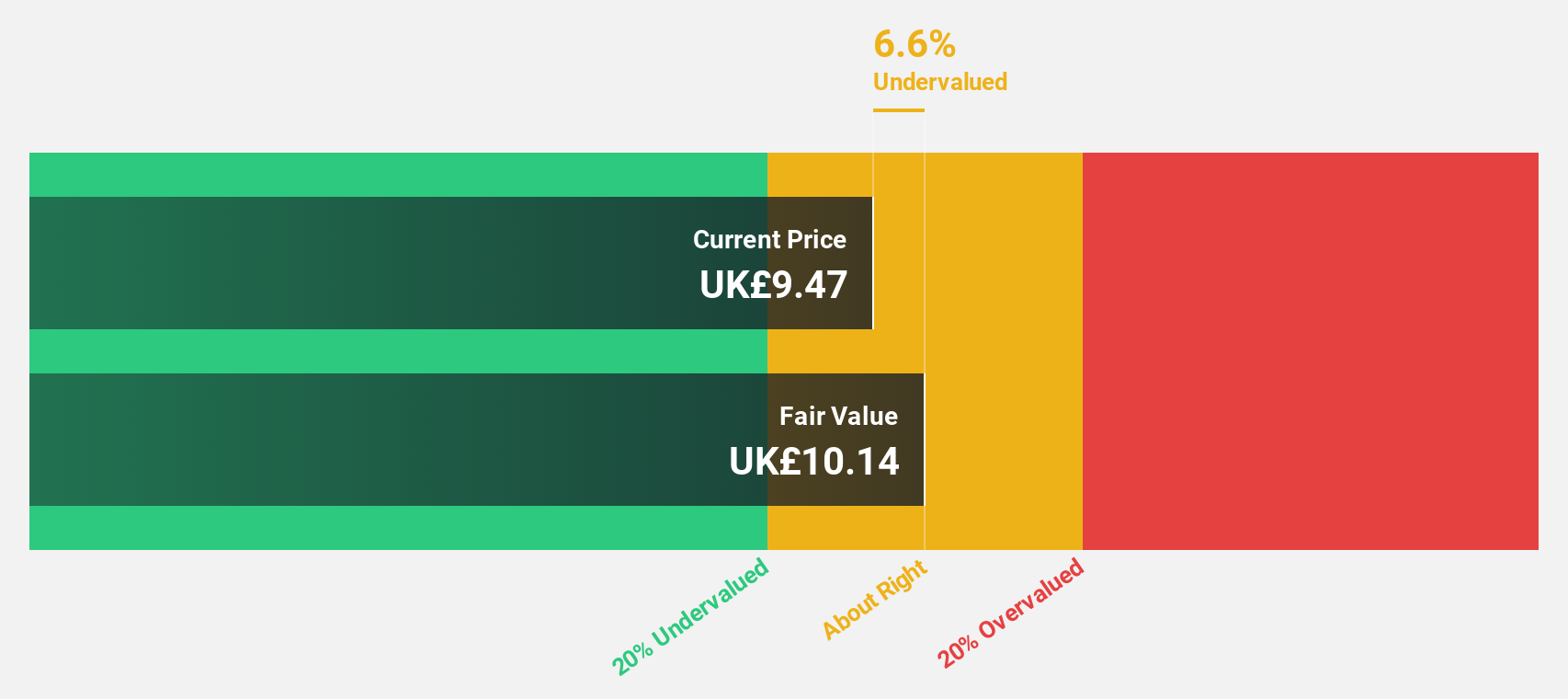

Young's Brewery (AIM:YNGA)

Overview: Young & Co.'s Brewery, P.L.C. operates and manages pubs and hotels in the United Kingdom with a market cap of £516.44 million.

Operations: Revenue Segments (in millions of £): Young & Co.'s Brewery generates its revenue through the operation and management of pubs and hotels across the United Kingdom.

Estimated Discount To Fair Value: 11.1%

Young's Brewery reported a sales increase to £250 million for the half year, with net income rising to £20 million. Despite trading at 11.1% below its fair value estimate of £10.71, profit margins have decreased from last year. Earnings are projected to grow significantly at 28.7% annually, surpassing the UK market average of 14.7%. However, shareholder dilution and low dividend coverage by earnings present concerns regarding financial sustainability despite recent dividend increases and operational changes in leadership structure.

- Upon reviewing our latest growth report, Young's Brewery's projected financial performance appears quite optimistic.

- Take a closer look at Young's Brewery's balance sheet health here in our report.

Key Takeaways

- Discover the full array of 54 Undervalued UK Stocks Based On Cash Flows right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:GBG

GB Group

Provides identity data intelligence products and services in the United Kingdom, the United States, Australia, and internationally.

Reasonable growth potential with mediocre balance sheet.