Stock Analysis

- United Kingdom

- /

- Banks

- /

- LSE:TBCG

UK Growth Companies With High Insider Ownership Highlighted

Reviewed by Simply Wall St

Over the past week, the United Kingdom stock market has shown stability with no significant changes, while it has experienced a modest growth of 5.4% over the past year. In this context of anticipated earnings growth and steady market conditions, companies with high insider ownership can be particularly compelling as they often signal strong confidence in the company's future from those who know it best.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Plant Health Care (AIM:PHC) | 36.8% | 121.3% |

| Petrofac (LSE:PFC) | 16.6% | 120.1% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 74.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 23.5% |

| Helios Underwriting (AIM:HUW) | 23.1% | 14.7% |

| Foresight Group Holdings (LSE:FSG) | 31.9% | 27.9% |

| Belluscura (AIM:BELL) | 38.6% | 117.8% |

| Velocity Composites (AIM:VEL) | 27.8% | 173.3% |

| B90 Holdings (AIM:B90) | 24.4% | 142.7% |

| Hochschild Mining (LSE:HOC) | 38.4% | 42.6% |

Here we highlight a subset of our preferred stocks from the screener.

Craneware (AIM:CRW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Craneware plc, a company engaged in developing, licensing, and supporting software for the healthcare sector primarily in the United States, has a market capitalization of approximately £856.36 million.

Operations: The company generates its revenue primarily from its healthcare software segment, totaling $180.56 million.

Insider Ownership: 17%

Craneware, a UK-based growth company with significant insider ownership, is poised for substantial earnings growth, forecasted at 29.39% annually over the next three years. While its revenue growth is slower at 6.7% annually, it still outpaces the UK market average. Recent strategic initiatives include a partnership with Microsoft to enhance its Trisus Platform through Azure, boosting its technological edge and market reach in healthcare analytics and AI applications. However, its projected return on equity of 11.2% suggests moderate efficiency in generating profits from shareholders' equity.

- Click to explore a detailed breakdown of our findings in Craneware's earnings growth report.

- Our valuation report here indicates Craneware may be overvalued.

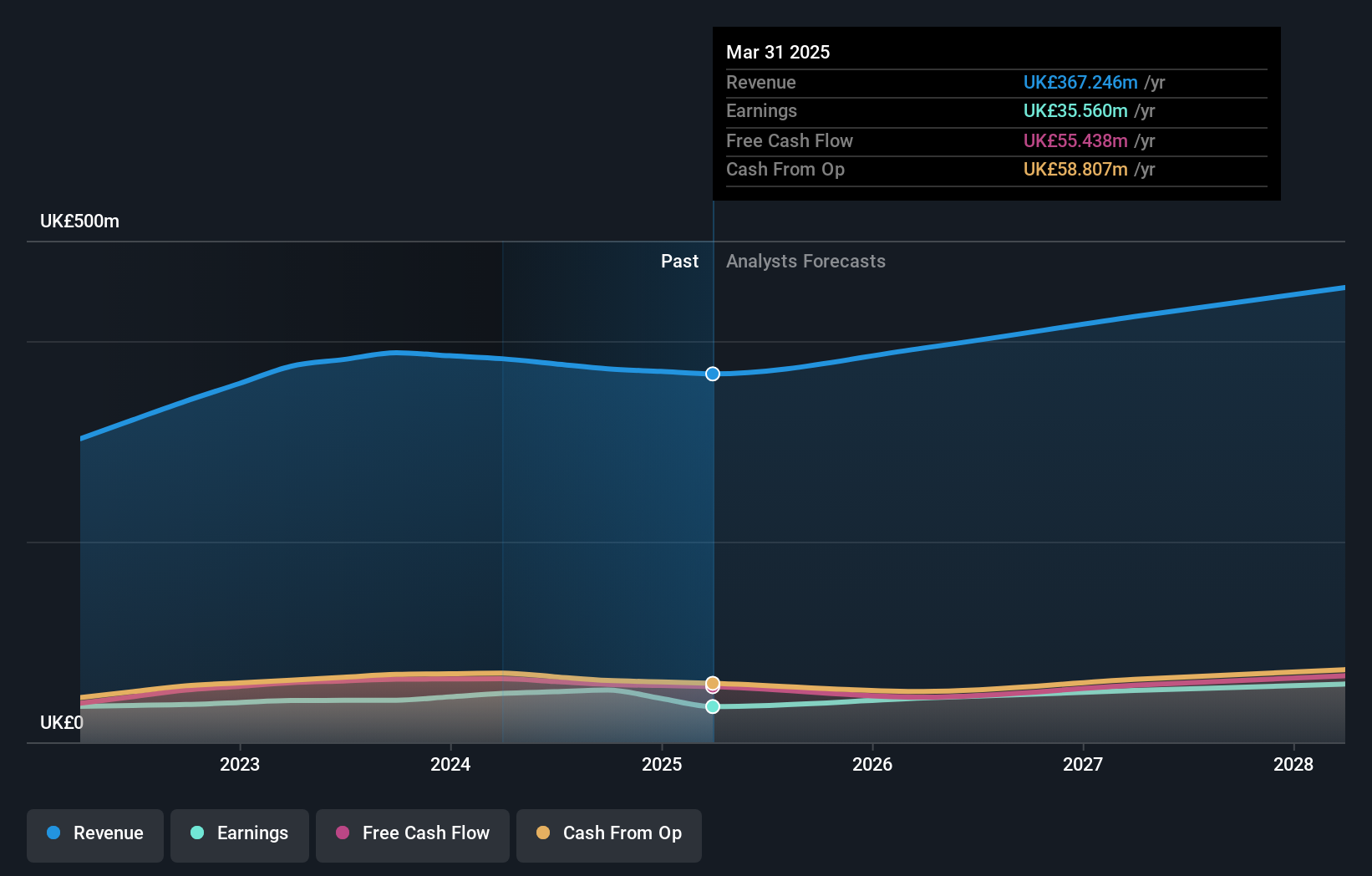

Kainos Group (LSE:KNOS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kainos Group plc is a provider of digital technology services across the United Kingdom, Ireland, North America, and Central Europe with a market capitalization of approximately £1.40 billion.

Operations: The company generates revenue through three primary segments: Digital Services (£213.10 million), Workday Products (£57.25 million), and Workday Services (£112.04 million).

Insider Ownership: 23.3%

Kainos Group, a UK-based company with substantial insider ownership, is expected to see its revenue grow by 8.8% annually, outpacing the UK market average. While this growth rate does not reach the high threshold of 20%, it is complemented by an earnings forecast increase of 13.1% per year. Recently, Kainos entered a strategic partnership with Pulsora to enhance corporate ESG reporting through digital solutions, marking a significant move towards sustainability leadership in its sector.

- Dive into the specifics of Kainos Group here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Kainos Group is priced higher than what may be justified by its financials.

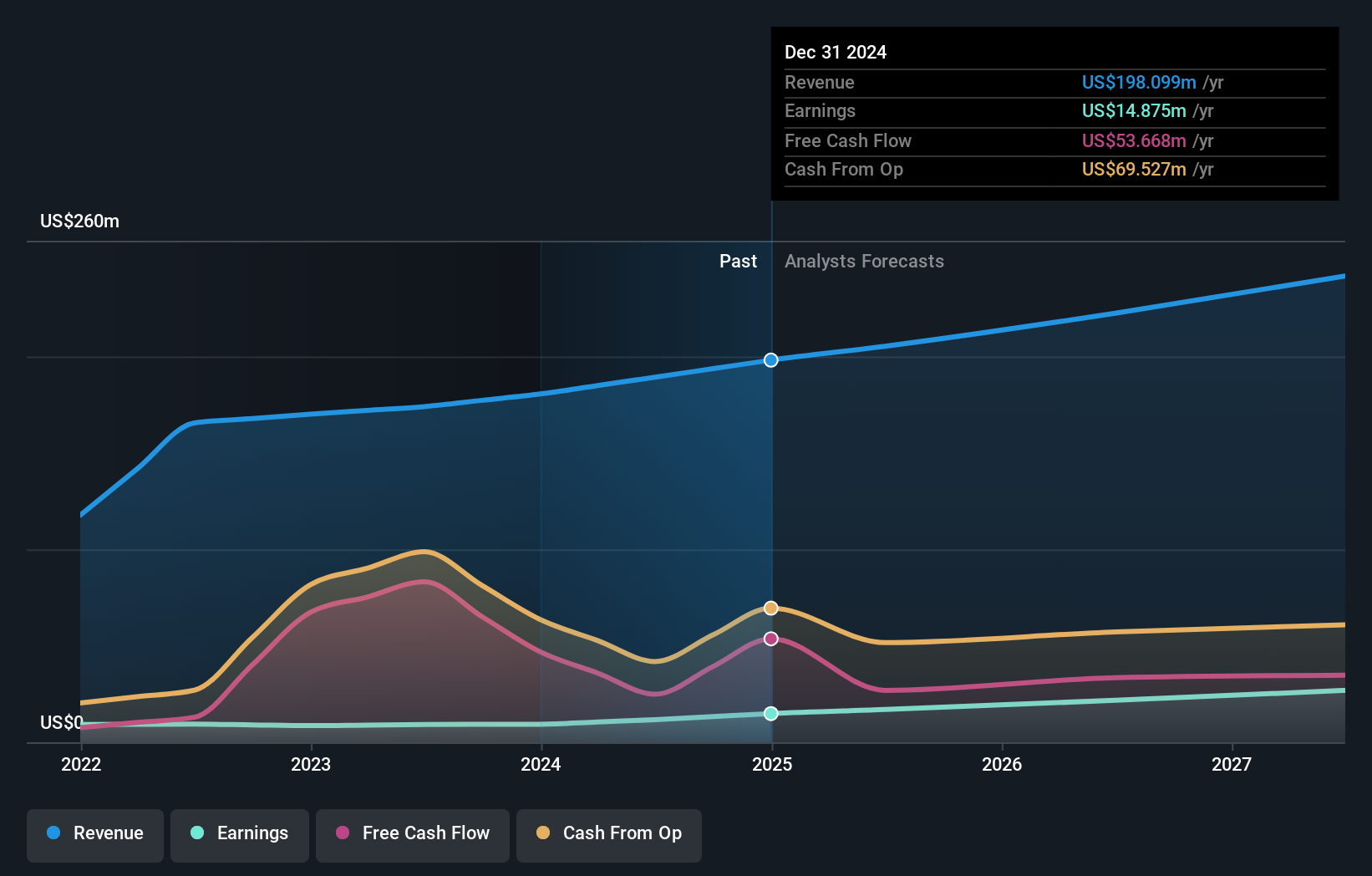

TBC Bank Group (LSE:TBCG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC operates in Georgia, Azerbaijan, and Uzbekistan, offering a range of services including banking, leasing, insurance, brokerage, and card processing to both corporate and individual clients with a market cap of approximately £1.65 billion.

Operations: The company generates revenue through banking, leasing, insurance, brokerage, and card processing services across Georgia, Azerbaijan, and Uzbekistan.

Insider Ownership: 18%

TBC Bank Group, a UK entity with considerable insider ownership, reported a robust first quarter in 2024 with net interest income and net income showing significant increases from the previous year. Despite this growth, the bank faces challenges such as a high bad loans ratio at 2.1% and an inadequate allowance for bad loans at 74%. The company's earnings are expected to grow by 15.22% annually, outstripping the UK market average. However, it is trading at 38.6% below its estimated fair value, suggesting potential undervaluation despite high volatility in its share price over the past three months.

- Take a closer look at TBC Bank Group's potential here in our earnings growth report.

- The analysis detailed in our TBC Bank Group valuation report hints at an deflated share price compared to its estimated value.

Seize The Opportunity

- Reveal the 61 hidden gems among our Fast Growing UK Companies With High Insider Ownership screener with a single click here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether TBC Bank Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:TBCG

TBC Bank Group

Through its subsidiaries, provides banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan.

Undervalued with reasonable growth potential and pays a dividend.