Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Benchmark Holdings plc (LON:BMK) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Benchmark Holdings

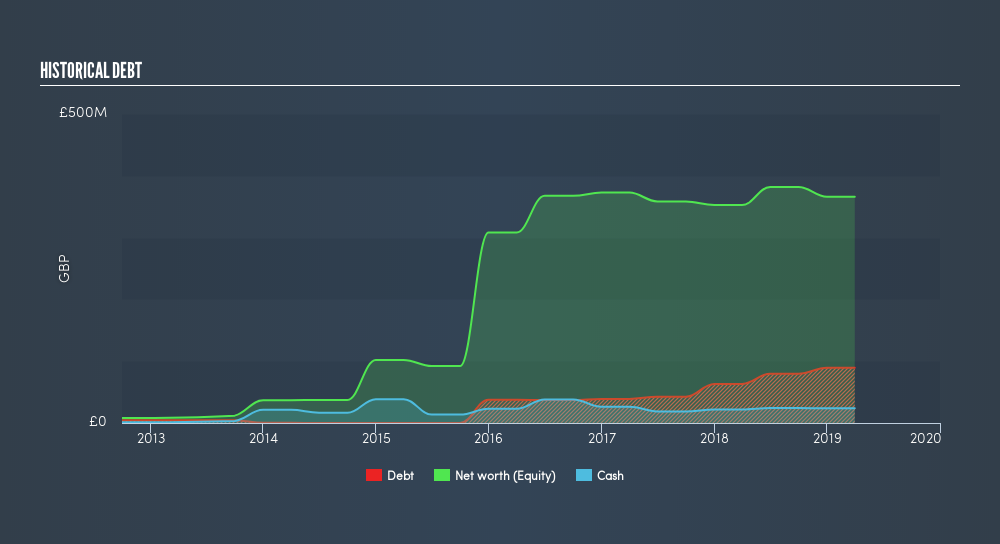

What Is Benchmark Holdings's Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Benchmark Holdings had UK£89.4m of debt, an increase on UK£63.2m, over one year. However, it also had UK£23.8m in cash, and so its net debt is UK£65.5m.

How Healthy Is Benchmark Holdings's Balance Sheet?

According to the last reported balance sheet, Benchmark Holdings had liabilities of UK£42.2m due within 12 months, and liabilities of UK£127.4m due beyond 12 months. Offsetting these obligations, it had cash of UK£23.8m as well as receivables valued at UK£37.0m due within 12 months. So it has liabilities totalling UK£108.9m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Benchmark Holdings has a market capitalization of UK£293.1m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Benchmark Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Benchmark Holdings reported revenue of UK£154m, which is a gain of 5.0%. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Over the last twelve months Benchmark Holdings produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at UK£6.8m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled UK£21m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. For riskier companies like Benchmark Holdings I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About AIM:BMK

Benchmark Holdings

Engages in the provision of technical services, products, and specialist knowledge that supports the development of food and farming industries.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor