- United Kingdom

- /

- Oil and Gas

- /

- LSE:HBR

Why We're Not Concerned About Harbour Energy plc's (LON:HBR) Share Price

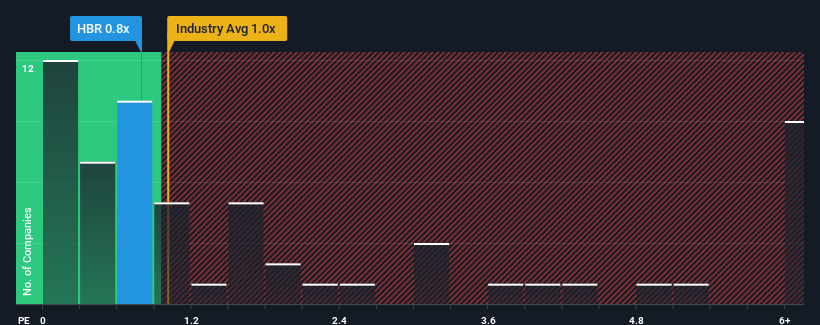

There wouldn't be many who think Harbour Energy plc's (LON:HBR) price-to-sales (or "P/S") ratio of 0.8x is worth a mention when the median P/S for the Oil and Gas industry in the United Kingdom is similar at about 1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Harbour Energy

How Has Harbour Energy Performed Recently?

Harbour Energy has been struggling lately as its revenue has declined faster than most other companies. One possibility is that the P/S is moderate because investors think the company's revenue trend will eventually fall in line with most others in the industry. If you still like the company, you'd want its revenue trajectory to turn around before making any decisions. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

Want the full picture on analyst estimates for the company? Then our free report on Harbour Energy will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The P/S?

In order to justify its P/S ratio, Harbour Energy would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 30% decrease to the company's top line. Even so, admirably revenue has lifted 55% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Shifting to the future, estimates from the eight analysts covering the company are not great, suggesting revenue should decline by 1.3% per year over the next three years. Meanwhile, the industry is forecast to moderate by 0.1% each year, which suggests the company won't escape the wider industry forces.

With this in consideration, it's clear to see why Harbour Energy's P/S stacks up closely with its industry peers. However, we think shrinking revenues are unlikely to lead to a stable P/S over the longer term, which could set up shareholders for future disappointment. Maintaining these prices will be difficult to achieve as the weak outlook is likely to weigh down the shares eventually.

The Bottom Line On Harbour Energy's P/S

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Harbour Energy's analyst forecasts revealed that its equally shaky outlook against the industry is keeping its P/S in line with the industry too. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to justify a high or low P/S ratio. Although, we are somewhat concerned whether the company can maintain this level of performance under these tough industry conditions. For now though, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 1 warning sign for Harbour Energy you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Harbour Energy, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Harbour Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:HBR

Harbour Energy

Engages in the acquisition, exploration, development, and production of oil and gas reserves in Norway, the United Kingdom, Germany, Mexico, Argentina, North Africa, and Southeast Asia.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Community Narratives