Advertisement

- United Kingdom

- /

- Diversified Financial

- /

- LSE:WISE

Wise's (LSE:WISE) Impressive 211% Earnings Surge and 36% ROE: Balancing Strengths with Forecasted Challenges and Opportunities

Simply Wall St

Reviewed by Simply Wall St

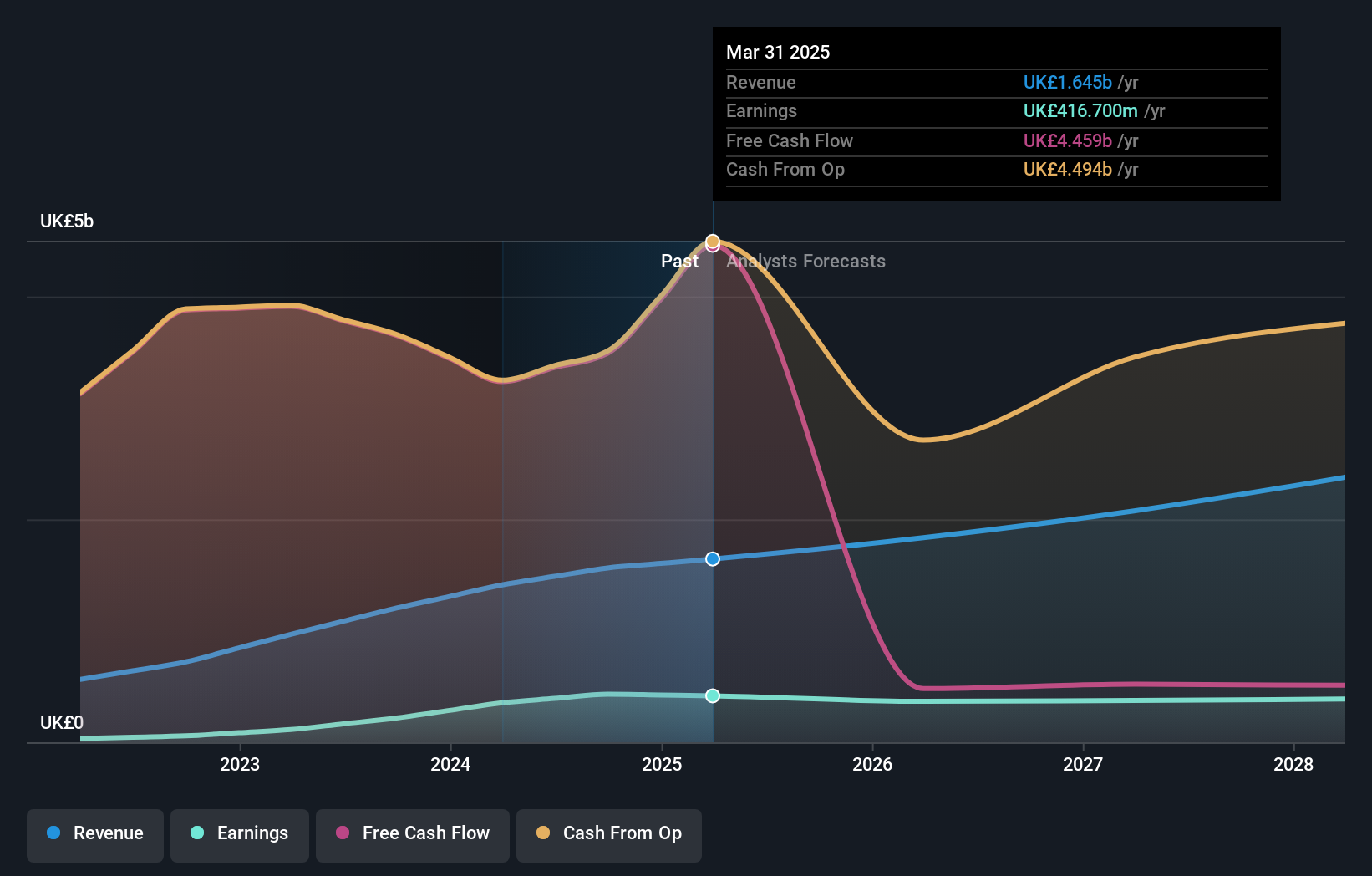

With a staggering 211.1% earnings growth in the past year and a return on equity of 36.2%, Wise (LSE:WISE) has outperformed its industry peers, though it faces challenges such as forecasted earnings declines and rising operational costs.

Click here and access our complete analysis report to understand the dynamics of Wise.

Innovative Factors Supporting Wise

Wise has demonstrated impressive earnings growth, averaging 60.7% annually over the past five years, with a remarkable 211.1% increase in the last year alone. This growth far surpasses the Diversified Financial industry average of 2.8%, highlighting Wise's strong market positioning. The company's return on equity stands at 36.2%, reflecting its efficient use of capital. With net profit margins rising to 25.1% from 11.8% last year, Wise is clearly on a profitable trajectory. The management's experience, with an average tenure of 3.3 years, underscores their strategic acumen in steering the company towards sustained growth. Moreover, Wise is trading below its estimated fair value, suggesting potential for future appreciation despite a lack of consensus among analysts on price targets.

Challenges Constraining Wise's Potential

However, Wise faces forecasted earnings declines over the next three years, with an anticipated reduction in return on equity to 18.4%. The projected revenue growth of 11.4% annually, while faster than the UK market's 3.6%, remains below the 20% threshold that might indicate more aggressive expansion. Rising operational costs have slightly impacted margins, pointing to the necessity for cost management strategies. Additionally, some regions, particularly in the Southeast, have not met growth expectations, suggesting a need for targeted market strategies.

Growth Avenues Awaiting Wise

Despite these challenges, Wise has opportunities to enhance its market position through strategic alliances and product-related announcements. With revenue forecasted to grow faster than the UK market, Wise is well-positioned to capitalize on emerging opportunities. The company's commitment to product innovation and maintaining strong customer relationships can further bolster its competitive edge.

Regulatory Challenges Facing Wise

External threats such as potential economic downturns and intensifying market competition pose significant risks. Wise must remain agile to navigate these challenges, particularly as regulatory changes could impact operations and compliance costs. Proactive monitoring and strategic planning will be crucial in mitigating these threats and ensuring sustained growth.

To dive deeper into how Wise's valuation metrics are shaping its market position, check out our detailed analysis of Wise's Valuation. Explore the current health of Wise and how it reflects on its financial stability and growth potential.

Conclusion

Wise's impressive earnings growth and substantial return on equity highlight its strong market positioning and efficient use of capital, suggesting a solid foundation for future profitability. However, anticipated earnings declines and rising operational costs indicate the need for strategic cost management and targeted market strategies to sustain growth. Despite these challenges, Wise's commitment to innovation and strategic alliances positions it to capitalize on emerging opportunities, potentially enhancing its market position. The fact that Wise is trading below its estimated fair value, coupled with a lack of consensus on price targets among analysts, suggests that there is room for future appreciation, provided the company effectively navigates regulatory challenges and market competition.

Summing It All Up

- Have a stake in Wise? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management .

- Find companies with promising cash flow potential yet trading below their fair value .

Valuation is complex, but we're here to simplify it.

Discover if Wise might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About LSE:WISE

Wise

Provides cross-border and domestic financial services for personal and business customers in the United Kingdom, rest of Europe, the Asia-Pacific, North America, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor