Stock Analysis

- United Kingdom

- /

- Capital Markets

- /

- LSE:HL.

Hargreaves Lansdown plc (LON:HL.) Stock Catapults 30% Though Its Price And Business Still Lag The Market

Hargreaves Lansdown plc (LON:HL.) shareholders would be excited to see that the share price has had a great month, posting a 30% gain and recovering from prior weakness. Taking a wider view, although not as strong as the last month, the full year gain of 13% is also fairly reasonable.

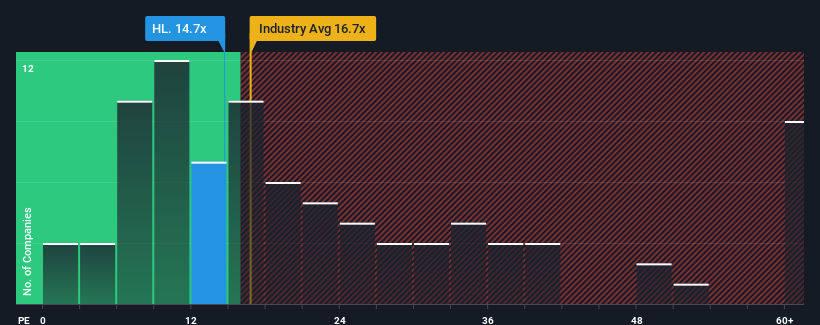

In spite of the firm bounce in price, Hargreaves Lansdown's price-to-earnings (or "P/E") ratio of 14.7x might still make it look like a buy right now compared to the market in the United Kingdom, where around half of the companies have P/E ratios above 18x and even P/E's above 30x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Hargreaves Lansdown as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Hargreaves Lansdown

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Hargreaves Lansdown's is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a terrific increase of 20%. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 7.6% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 1.8% each year over the next three years. With the market predicted to deliver 15% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that Hargreaves Lansdown's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Hargreaves Lansdown's P/E?

Despite Hargreaves Lansdown's shares building up a head of steam, its P/E still lags most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Hargreaves Lansdown maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Hargreaves Lansdown that you need to be mindful of.

If these risks are making you reconsider your opinion on Hargreaves Lansdown, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether Hargreaves Lansdown is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:HL.

Hargreaves Lansdown

Provides investment services for individuals and corporates in the United Kingdom and Poland.

Outstanding track record with flawless balance sheet and pays a dividend.