Advertisement

- United Kingdom

- /

- Diversified Financial

- /

- AIM:TIME

Here's Why Time Finance (LON:TIME) Has Caught The Eye Of Investors

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

In contrast to all that, many investors prefer to focus on companies like Time Finance (LON:TIME), which has not only revenues, but also profits. Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Time Finance with the means to add long-term value to shareholders.

How Fast Is Time Finance Growing Its Earnings Per Share?

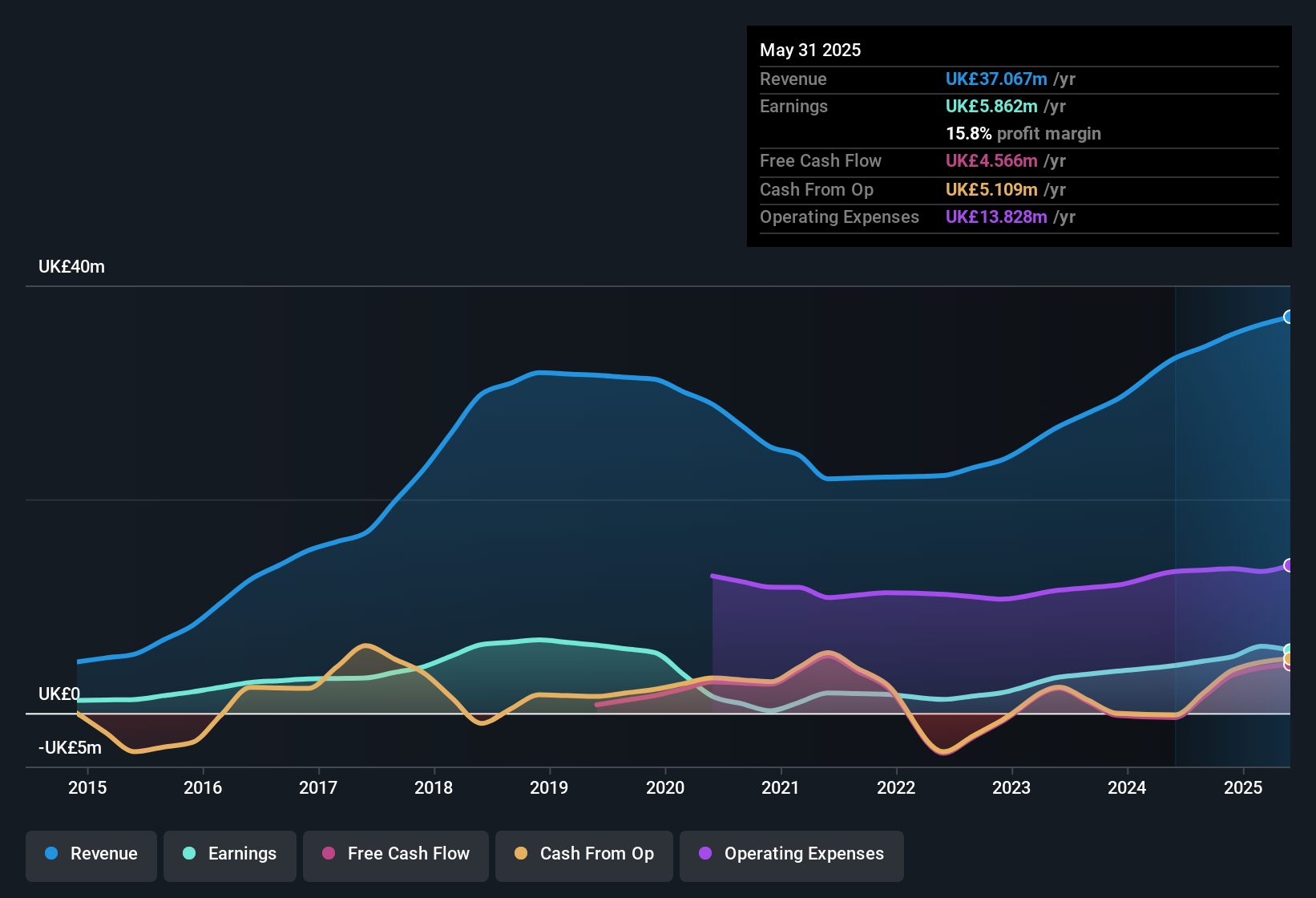

Time Finance has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. So it would be better to isolate the growth rate over the last year for our analysis. To the delight of shareholders, Time Finance's EPS soared from UK£0.048 to UK£0.064, over the last year. That's a impressive gain of 33%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. It's noted that Time Finance's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. While we note Time Finance achieved similar EBIT margins to last year, revenue grew by a solid 12% to UK£37m. That's encouraging news for the company!

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

See our latest analysis for Time Finance

Time Finance isn't a huge company, given its market capitalisation of UK£50m. That makes it extra important to check on its balance sheet strength.

Are Time Finance Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

One positive for Time Finance, is that company insiders spent UK£28k acquiring shares in the last year. While this investment may be modest, it is great considering the lack of insider selling. It is also worth noting that it was Independent Non-Executive Director Tracy Watkinson who made the biggest single purchase, worth UK£10.0k, paying UK£0.55 per share.

Should You Add Time Finance To Your Watchlist?

If you believe that share price follows earnings per share you should definitely be delving further into Time Finance's strong EPS growth. Growth in EPS isn't the only striking feature with company insiders adding to their holdings being another noteworthy vote of confidence for the company. To put it succinctly; Time Finance is a strong candidate for your watchlist. What about risks? Every company has them, and we've spotted 1 warning sign for Time Finance you should know about.

The good news is that Time Finance is not the only stock with insider buying. Here's a list of small cap, undervalued companies in GB with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Time Finance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:TIME

Time Finance

Provides financial products and services to consumers and businesses in the United Kingdom.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor