Advertisement

- United Kingdom

- /

- Capital Markets

- /

- LSE:GROW

One Draper Esprit plc (LON:GROW) Broker Just Cut Their Revenue Forecasts By 43%

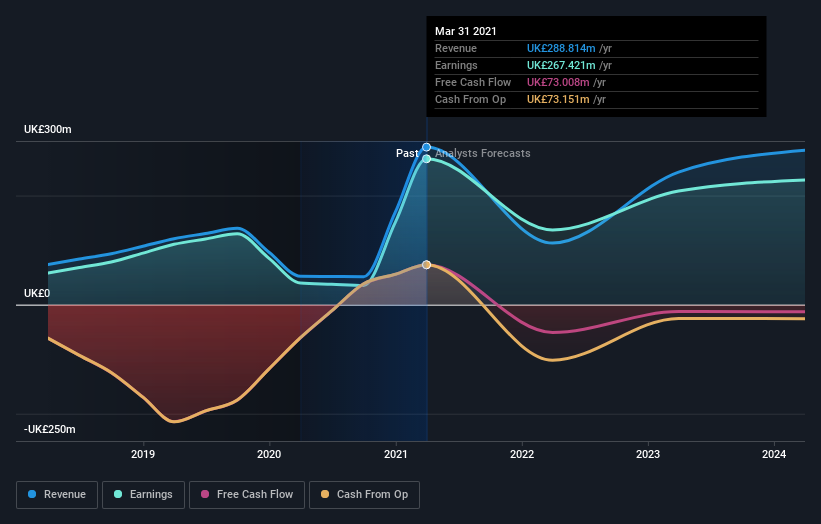

The analyst covering Draper Esprit plc (LON:GROW) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

Following the latest downgrade, the single analyst covering Draper Esprit provided consensus estimates of UK£113m revenue in 2022, which would reflect a stressful 61% decline on its sales over the past 12 months. Statutory earnings per share are supposed to dive 67% to UK£0.69 in the same period. Previously, the analyst had been modelling revenues of UK£198m and earnings per share (EPS) of UK£0.76 in 2022. Indeed, we can see that analyst sentiment has declined measurably after the new consensus came out, with a sizeable cut to revenue estimates and a minor downgrade to EPS estimates to boot.

View our latest analysis for Draper Esprit

The analyst made no major changes to their price target of UK£9.90, suggesting the downgrades are not expected to have a long-term impact on Draper Esprit's valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Draper Esprit, with the most bullish analyst valuing it at UK£10.14 and the most bearish at UK£9.67 per share. With such a narrow range of valuations, analysts apparently share similar views on what they think the business is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Draper Esprit's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 61% by the end of 2022. This indicates a significant reduction from annual growth of 36% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 2.0% per year. It's pretty clear that Draper Esprit's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that the analyst has reduced their earnings per share estimates, suggesting business headwinds lay ahead for Draper Esprit. Unfortunately the analyst also downgraded their revenue estimates, and industry data suggests that Draper Esprit's revenues are expected to grow slower than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of Draper Esprit going forwards.

As you can see, this analyst clearly isn't bullish, and there might be good reason for that. We've identified some potential issues with Draper Esprit's financials, such as concerns around earnings quality. For more information, you can click here to discover this and the 1 other flag we've identified.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading Draper Esprit or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:GROW

Molten Ventures

Molten Ventures Plc, formerly known as Draper Esprit plc, is a private equity and venture capital firm specializing in directly investing as well as investing in other funds.

High growth potential and fair value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor