Advertisement

- United Kingdom

- /

- Commercial Services

- /

- AIM:FRAN

Don't Sell Franchise Brands plc (LON:FRAN) Before You Read This

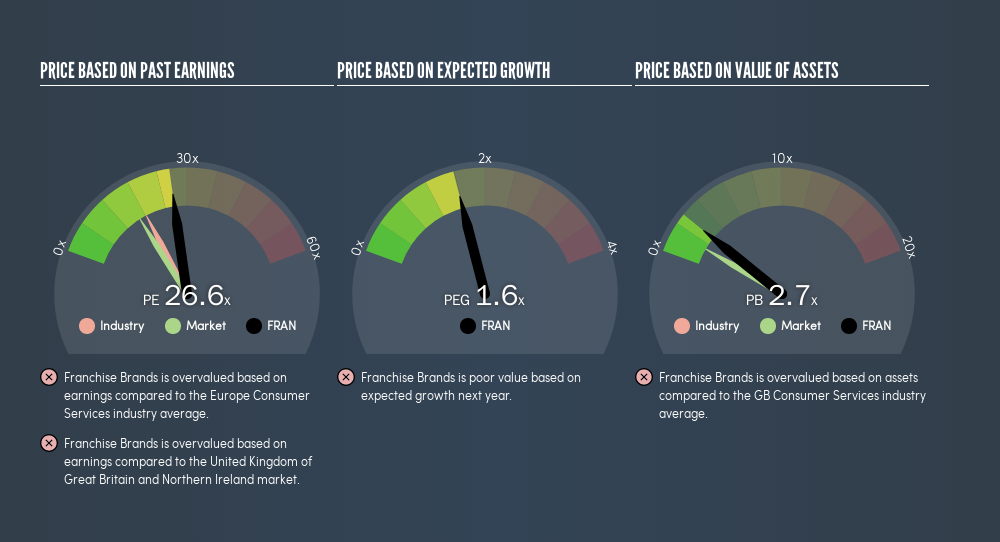

This article is for investors who would like to improve their understanding of price to earnings ratios (P/E ratios). We'll look at Franchise Brands plc's (LON:FRAN) P/E ratio and reflect on what it tells us about the company's share price. Looking at earnings over the last twelve months, Franchise Brands has a P/E ratio of 26.55. That corresponds to an earnings yield of approximately 3.8%.

See our latest analysis for Franchise Brands

How Do I Calculate A Price To Earnings Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Franchise Brands:

P/E of 26.55 = £0.89 ÷ £0.034 (Based on the year to June 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each £1 of company earnings. That isn't necessarily good or bad, but a high P/E implies relatively high expectations of what a company can achieve in the future.

How Does Franchise Brands's P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. You can see in the image below that the average P/E (17.9) for companies in the consumer services industry is lower than Franchise Brands's P/E.

That means that the market expects Franchise Brands will outperform other companies in its industry.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. Earnings growth means that in the future the 'E' will be higher. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

Franchise Brands's earnings made like a rocket, taking off 102% last year. And earnings per share have improved by 18% annually, over the last three years. So we'd absolutely expect it to have a relatively high P/E ratio. Unfortunately, earnings per share are down 5.8% a year, over 5 years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

Don't forget that the P/E ratio considers market capitalization. That means it doesn't take debt or cash into account. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

So What Does Franchise Brands's Balance Sheet Tell Us?

Net debt totals just 6.7% of Franchise Brands's market cap. It would probably trade on a higher P/E ratio if it had a lot of cash, but I doubt it is having a big impact.

The Verdict On Franchise Brands's P/E Ratio

Franchise Brands trades on a P/E ratio of 26.6, which is above its market average of 16.3. Its debt levels do not imperil its balance sheet and its EPS growth is very healthy indeed. So on this analysis a high P/E ratio seems reasonable.

Investors have an opportunity when market expectations about a stock are wrong. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course you might be able to find a better stock than Franchise Brands. So you may wish to see this free collection of other companies that have grown earnings strongly.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About AIM:FRAN

Franchise Brands

Through its subsidiaries, engages in franchising and related activities in the United Kingdom, Ireland, North America, and Continental Europe.

Solid track record with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor