- United Kingdom

- /

- Professional Services

- /

- LSE:HAS

Top 3 Undervalued Small Caps In The United Kingdom With Insider Action October 2024

Reviewed by Simply Wall St

The United Kingdom's market has been experiencing turbulence, with the FTSE 100 closing lower amid weak trade data from China and broader global economic concerns. Despite these challenges, small-cap stocks often present unique opportunities for investors, particularly those that show signs of being undervalued and have insider action indicating confidence in their potential.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Dr. Martens | 7.8x | 0.6x | 40.04% | ★★★★★★ |

| Domino's Pizza Group | 15.2x | 1.7x | 39.05% | ★★★★★☆ |

| C&C Group | NA | 0.5x | 44.71% | ★★★★★☆ |

| Bytes Technology Group | 26.5x | 6.0x | 5.49% | ★★★★☆☆ |

| CVS Group | 31.0x | 1.3x | 41.39% | ★★★★☆☆ |

| Essentra | 732.1x | 1.4x | 37.04% | ★★★★☆☆ |

| Genus | 166.4x | 2.0x | -0.52% | ★★★★☆☆ |

| NWF Group | 8.8x | 0.1x | 34.98% | ★★★☆☆☆ |

| Alpha Group International | 9.9x | 4.6x | -24.24% | ★★★☆☆☆ |

| Harworth Group | 12.5x | 6.5x | -620.87% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

Dr. Martens (LSE:DOCS)

Simply Wall St Value Rating: ★★★★★★

Overview: Dr. Martens is a renowned footwear company primarily engaged in the design, manufacturing, and sale of iconic boots and shoes, with a market capitalization of approximately £2.50 billion.

Operations: Dr. Martens generates revenue primarily from its footwear segment, with a gross profit margin of 65.58% as of September 30, 2024. The company's operating expenses include significant costs in general and administrative areas, which have reached £377.70 million for the same period.

PE: 7.8x

Dr. Martens, a notable player in the UK market, has seen insider confidence with share purchases in Q2 2024. Despite its high debt levels and reliance on external borrowing, earnings are forecast to grow at 5.88% annually. The company’s profit margins have dipped from 12.9% last year to 7.9%. Additionally, recent investor activism by Sparta Capital Management Ltd concluded without further discussions post-July AGM results announcement on July 11, 2024.

Genus (LSE:GNS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Genus is a company specializing in animal genetics, with operations in bovine and porcine breeding, and a market cap of approximately £2.50 billion.

Operations: Genus generates revenue through its Genus ABS and Genus PIC segments, with the latter contributing £352.5 million. The company's gross profit margin has shown significant fluctuations, peaking at 68.02% in March 2024, while net income margins have varied widely, reaching up to 14.05% in December 2017 but dropping to lower levels in recent periods.

PE: 166.4x

Genus, a small cap stock in the UK, has seen insider confidence with recent share purchases over the past six months. Despite a drop in net income from £33.3 million to £7.9 million for the year ending June 30, 2024, and sales decreasing to £668.8 million from £689.7 million, earnings are forecasted to grow by 39.4% annually. The company also affirmed a final dividend of 21.7 pence per share payable on December 6, indicating stable shareholder returns amidst financial challenges.

- Take a closer look at Genus' potential here in our valuation report.

Assess Genus' past performance with our detailed historical performance reports.

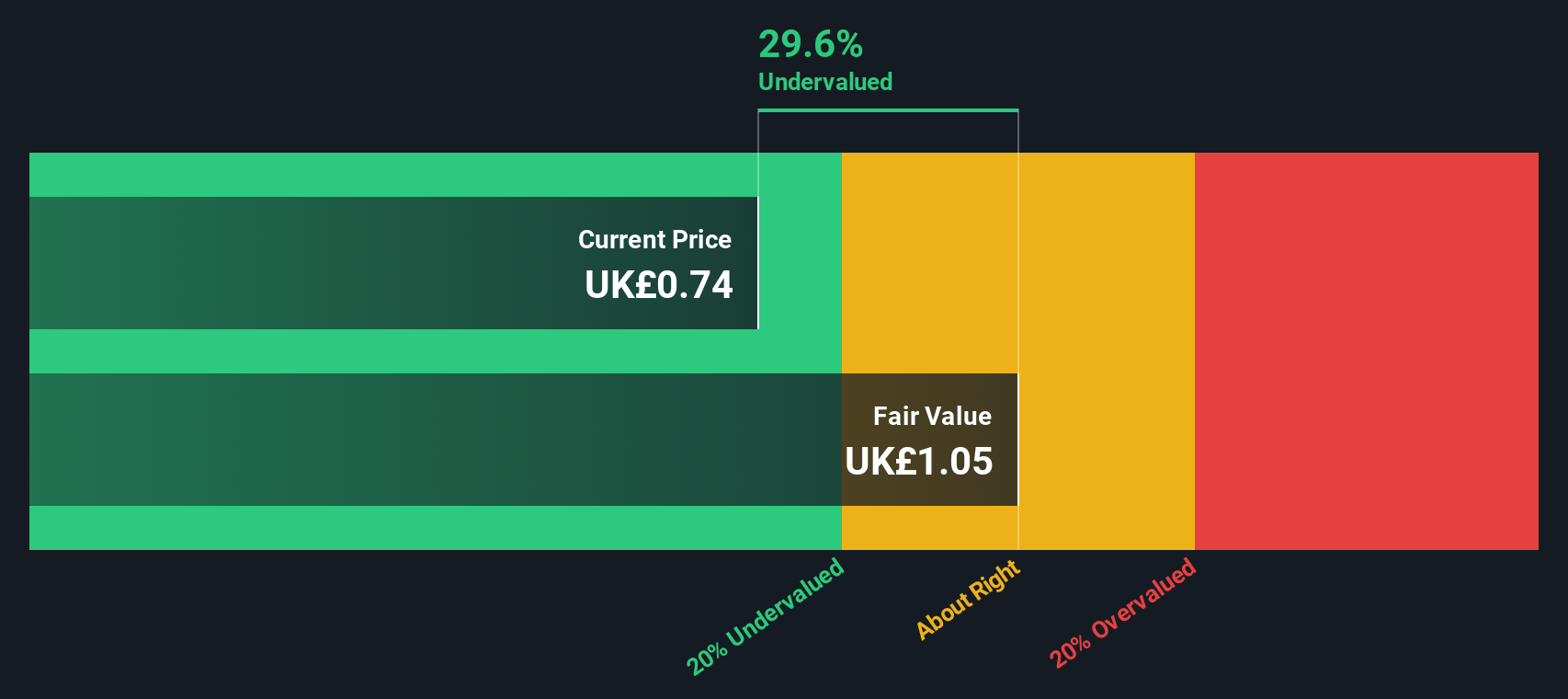

Hays (LSE:HAS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hays is a global recruitment company specializing in qualified, professional, and skilled recruitment services with a market cap of approximately £1.60 billion.

Operations: Hays generates revenue primarily from qualified, professional, and skilled recruitment services. The company's cost of goods sold (COGS) consistently represents a significant portion of its expenses, with gross profit margins ranging from 4.21% to 14.34% over the observed periods.

PE: -300.3x

Hays plc, a notable player among undervalued UK small caps, reported full-year sales of £6.95 billion for the year ending June 30, 2024, down from £7.58 billion the previous year. The company faced a net loss of £4.9 million compared to a net income of £138.3 million last year. Insider confidence is evident with recent share purchases by executives in August 2024. Earnings are forecasted to grow by 62% annually, highlighting potential future growth despite current challenges in revenue and profitability metrics.

- Click here and access our complete valuation analysis report to understand the dynamics of Hays.

Review our historical performance report to gain insights into Hays''s past performance.

Turning Ideas Into Actions

- Explore the 19 names from our Undervalued UK Small Caps With Insider Buying screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hays might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HAS

Hays

Engages in the provision of recruitment services in Australia, New Zealand, Germany, the United Kingdom, Ireland, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives