- United Kingdom

- /

- Consumer Durables

- /

- AIM:VCP

Victoria (LON:VCP) adds UK£22m to market cap in the past 7 days, though investors from three years ago are still down 84%

This week we saw the Victoria PLC (LON:VCP) share price climb by 12%. But the last three years have seen a terrible decline. Indeed, the share price is down a whopping 84% in the last three years. So it's about time shareholders saw some gains. The thing to think about is whether the business has really turned around. While a drop like that is definitely a body blow, money isn't as important as health and happiness.

The recent uptick of 12% could be a positive sign of things to come, so let's take a look at historical fundamentals.

See our latest analysis for Victoria

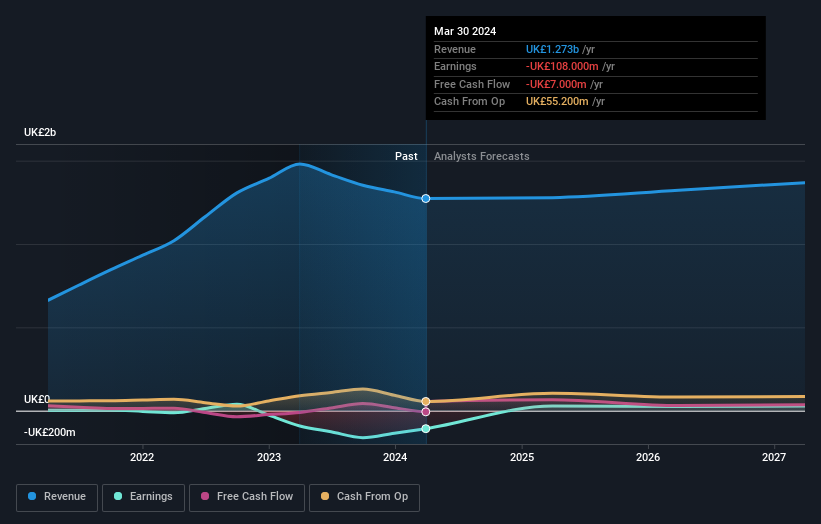

Because Victoria made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually desire strong revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

In the last three years, Victoria saw its revenue grow by 21% per year, compound. That's well above most other pre-profit companies. So why has the share priced crashed 23% per year, in the same time? The share price makes us wonder if there is an issue with profitability. Sometimes fast revenue growth doesn't lead to profits. If the company is low on cash, it may have to raise capital soon.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

This free interactive report on Victoria's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Investors in Victoria had a tough year, with a total loss of 73%, against a market gain of about 11%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 11% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Victoria better, we need to consider many other factors. For example, we've discovered 2 warning signs for Victoria (1 is a bit concerning!) that you should be aware of before investing here.

But note: Victoria may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on British exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:VCP

Victoria

Designs, manufactures, and distributes flooring products primarily in the United Kingdom, Italy, Belgium, Spain, Australia, the Netherlands, Turkey, France, Ireland, Portugal, and the United States.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Community Narratives