Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- AIM:PMP

Our Take On The Returns On Capital At Portmeirion Group (LON:PMP)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. In light of that, when we looked at Portmeirion Group (LON:PMP) and its ROCE trend, we weren't exactly thrilled.

Return On Capital Employed (ROCE): What is it?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Portmeirion Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

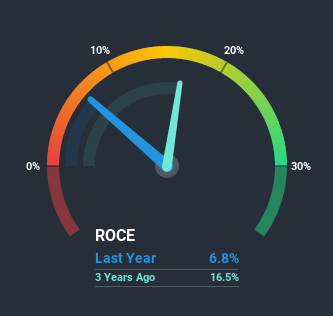

0.068 = UK£5.0m ÷ (UK£90m - UK£17m) (Based on the trailing twelve months to June 2020).

So, Portmeirion Group has an ROCE of 6.8%. On its own that's a low return on capital but it's in line with the industry's average returns of 6.7%.

See our latest analysis for Portmeirion Group

Above you can see how the current ROCE for Portmeirion Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Portmeirion Group here for free.

What The Trend Of ROCE Can Tell Us

The trend of ROCE doesn't look fantastic because it's fallen from 23% five years ago, while the business's capital employed increased by 109%. Usually this isn't ideal, but given Portmeirion Group conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. It's unlikely that all of the funds raised have been put to work yet, so as a consequence Portmeirion Group might not have received a full period of earnings contribution from it.

The Bottom Line On Portmeirion Group's ROCE

Bringing it all together, while we're somewhat encouraged by Portmeirion Group's reinvestment in its own business, we're aware that returns are shrinking. And investors appear hesitant that the trends will pick up because the stock has fallen 43% in the last five years. Therefore based on the analysis done in this article, we don't think Portmeirion Group has the makings of a multi-bagger.

On a separate note, we've found 3 warning signs for Portmeirion Group you'll probably want to know about.

While Portmeirion Group isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade Portmeirion Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:PMP

Portmeirion Group

Manufactures, markets, and distributes ceramics, home fragrances, and associated homeware products in the United Kingdom, South Korea, North America, and internationally.

Mediocre balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor