Advertisement

- United Kingdom

- /

- Professional Services

- /

- LSE:WIL

It's Unlikely That Wilmington plc's (LON:WIL) CEO Will See A Huge Pay Rise This Year

Key Insights

- Wilmington's Annual General Meeting to take place on 28th of November

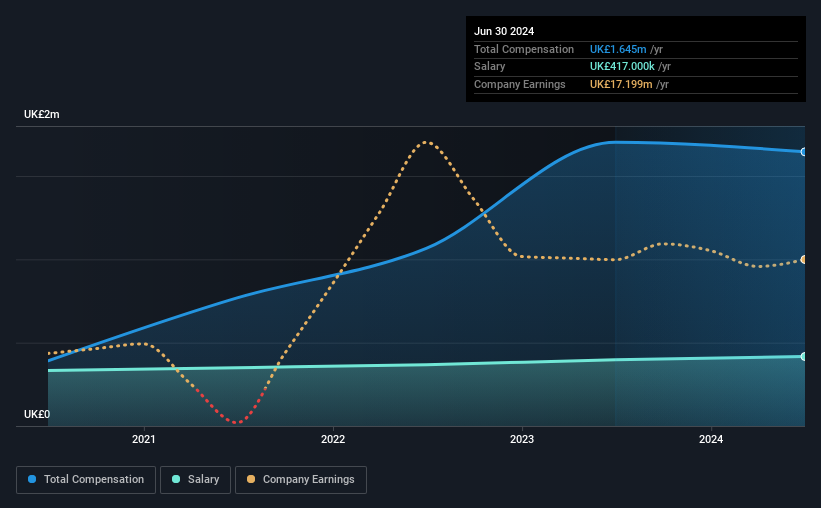

- Salary of UK£417.0k is part of CEO Mark Milner's total remuneration

- Total compensation is 171% above industry average

- Wilmington's total shareholder return over the past three years was 84% while its EPS grew by 19% over the past three years

Under the guidance of CEO Mark Milner, Wilmington plc (LON:WIL) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 28th of November. However, some shareholders will still be cautious of paying the CEO excessively.

View our latest analysis for Wilmington

Comparing Wilmington plc's CEO Compensation With The Industry

Our data indicates that Wilmington plc has a market capitalization of UK£351m, and total annual CEO compensation was reported as UK£1.6m for the year to June 2024. We note that's a small decrease of 3.3% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at UK£417k.

In comparison with other companies in the British Professional Services industry with market capitalizations ranging from UK£159m to UK£635m, the reported median CEO total compensation was UK£608k. Accordingly, our analysis reveals that Wilmington plc pays Mark Milner north of the industry median. What's more, Mark Milner holds UK£1.4m worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£417k | UK£397k | 25% |

| Other | UK£1.2m | UK£1.3m | 75% |

| Total Compensation | UK£1.6m | UK£1.7m | 100% |

On an industry level, roughly 64% of total compensation represents salary and 36% is other remuneration. In Wilmington's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Wilmington plc's Growth Numbers

Over the past three years, Wilmington plc has seen its earnings per share (EPS) grow by 19% per year. In the last year, its revenue is up 5.7%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Wilmington plc Been A Good Investment?

We think that the total shareholder return of 84%, over three years, would leave most Wilmington plc shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 2 warning signs for Wilmington that investors should look into moving forward.

Important note: Wilmington is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Wilmington might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:WIL

Wilmington

Provides data, information, training, and education solutions to professional markets in the United Kingdom, the United States, rest of Europe, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

106 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative