Advertisement

- United Kingdom

- /

- Biotech

- /

- LSE:GNS

Undervalued UK Small Caps With Insider Action In December 2024

Simply Wall St

Reviewed by Simply Wall St

As of late, the United Kingdom's market has been experiencing fluctuations, with the FTSE 100 index closing lower due to weak trade data from China and broader global economic concerns impacting investor sentiment. Despite these challenges, small-cap stocks often present unique opportunities for investors seeking potential growth in underexplored areas of the market. In this context, identifying companies with strong fundamentals and insider activity can be particularly appealing for those looking to navigate current market conditions effectively.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Pets at Home Group | 11.5x | 0.7x | 33.16% | ★★★★★★ |

| Headlam Group | NA | 0.2x | 25.46% | ★★★★★☆ |

| Sabre Insurance Group | 11.1x | 1.5x | 13.78% | ★★★★☆☆ |

| Marlowe | NA | 0.7x | 47.88% | ★★★★☆☆ |

| J D Wetherspoon | 15.6x | 0.4x | 17.68% | ★★★★☆☆ |

| Optima Health | NA | 1.2x | 39.04% | ★★★★☆☆ |

| iomart Group | 29.5x | 0.8x | 24.33% | ★★★☆☆☆ |

| Reach | 6.8x | 0.5x | -133.72% | ★★★☆☆☆ |

| Genus | 142.7x | 1.7x | 26.35% | ★★★☆☆☆ |

| THG | NA | 0.4x | -1056.48% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

Restore (AIM:RST)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Restore is a company that provides secure lifecycle services and digital information management solutions, with a market cap of £0.52 billion.

Operations: Secure Lifecycle Services and Digital & Information Management are the primary revenue segments, contributing £104.4 million and £172.5 million respectively. The company experienced fluctuations in its net income margin, with a notable decline into negative figures in recent periods, reaching -11.08% by December 2023 before recovering to 1.37% by June 2024. Operating expenses have remained substantial relative to revenue, impacting overall profitability trends over time.

PE: 95.8x

Restore, a UK-based company, is experiencing insider confidence with Charles Skinner acquiring 100,000 shares for £280K in November 2024. Despite facing slower activity and flat revenue projections due to market uncertainty before the Autumn Budget, the company anticipates earnings growth of 48% annually. However, its financial position is challenged by interest payments not well covered by earnings and reliance on higher-risk external borrowing. The recent addition of Patrick Butcher as a non-executive director may bring fresh strategic insights.

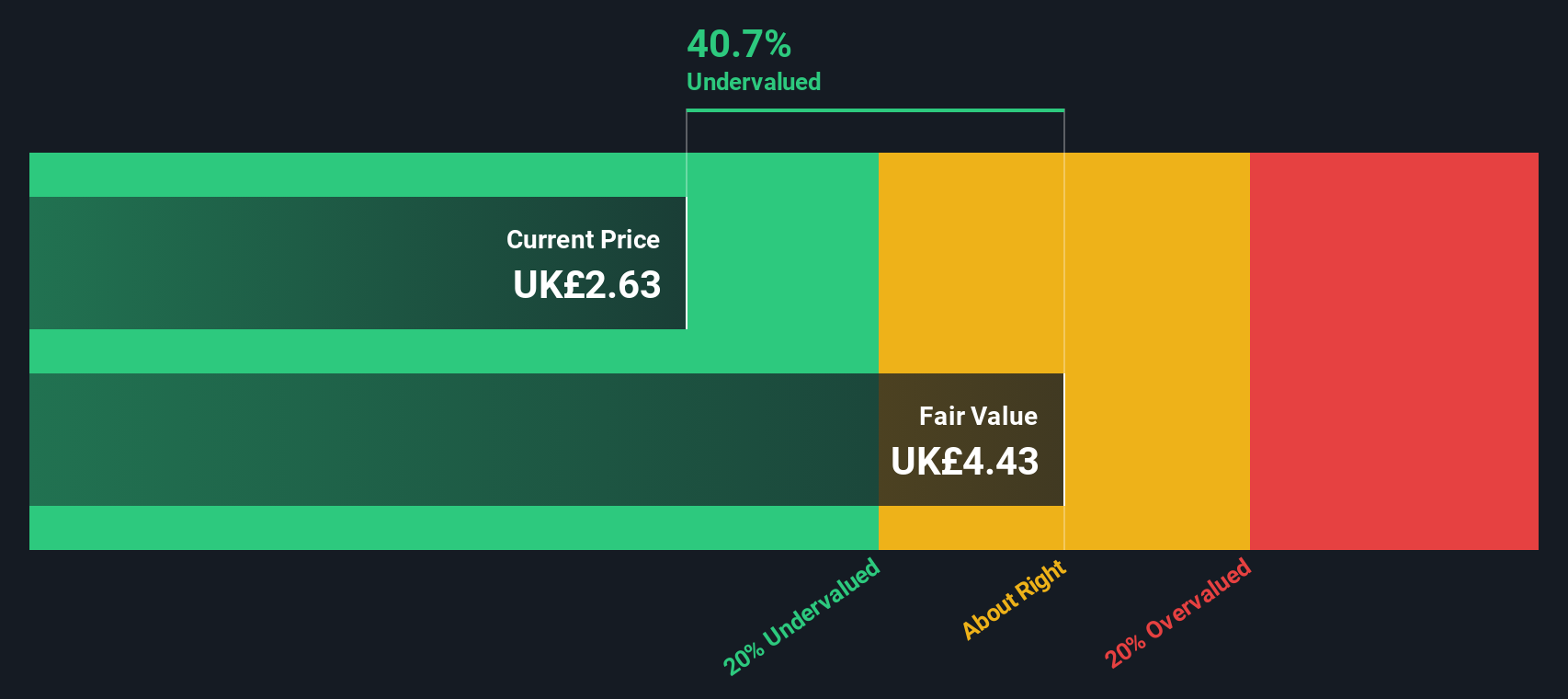

Genus (LSE:GNS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Genus is a leading global animal genetics company that focuses on developing and supplying high-quality breeding stock to farmers, with a market cap of approximately £1.92 billion.

Operations: Genus generates revenue primarily from its Genus ABS and Genus PIC segments, with the latter contributing £352.50 million. The company's cost of goods sold (COGS) has shown fluctuations, impacting its gross profit margin, which reached a peak of 53.78% in December 2014 before experiencing variations over subsequent periods. Operating expenses include significant allocations towards R&D and general & administrative costs, affecting net income margins that have varied across different time frames.

PE: 142.7x

Genus, a UK-based company, is navigating challenges with its recent financial performance showing a dip in net income to £7.9 million from £33.3 million the previous year. Despite this, insider confidence has been evident with share purchases in recent months, suggesting optimism about future prospects. The company also maintains strategic continuity with Alison Henriksen's planned CFO transition until July 2025 and continues rewarding shareholders through consistent dividends of 21.7 pence per share amidst auditor changes to PricewaterhouseCoopers LLP in November 2024.

- Unlock comprehensive insights into our analysis of Genus stock in this valuation report.

Review our historical performance report to gain insights into Genus''s past performance.

Mitchells & Butlers (LSE:MAB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Mitchells & Butlers operates a portfolio of pubs and restaurants in the UK, with a market cap of approximately £1.25 billion.

Operations: Revenue primarily comes from pubs and restaurants, with a notable gross profit margin trend showing fluctuations, reaching 16.93% most recently. Over time, the company has experienced variations in net income margins, indicating changes in profitability levels. Operating expenses have remained relatively stable compared to revenue shifts.

PE: 9.8x

Mitchells & Butlers, a smaller UK company, has shown significant financial improvement with sales reaching £2.61 billion for the year ending September 2024, up from £2.50 billion the previous year. Net income swung to a profit of £149 million from a loss of £4 million. This turnaround highlights potential value in their stock, despite reliance on external borrowing for funding. Insider confidence is evident with recent share purchases by insiders in November 2024, suggesting optimism about future growth prospects as earnings are projected to grow annually by 7.63%.

- Click to explore a detailed breakdown of our findings in Mitchells & Butlers' valuation report.

Assess Mitchells & Butlers' past performance with our detailed historical performance reports.

Next Steps

- Discover the full array of 26 Undervalued UK Small Caps With Insider Buying right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:GNS

Genus

Operates as an animal genetics company in North America, Latin America, the United Kingdom, rest of Europe, the Middle East, Russia, Africa, and Asia.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor