Advertisement

- United Kingdom

- /

- Beverage

- /

- AIM:NICL

UK Stocks Priced Below Estimated Value In April 2025

Simply Wall St

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 index grapples with global economic challenges, notably the sluggish recovery of China's economy, investors are keenly observing how these developments impact market dynamics. In this environment, identifying undervalued stocks becomes crucial as they may offer potential opportunities for growth despite broader market uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Gooch & Housego (AIM:GHH) | £3.77 | £7.14 | 47.2% |

| Aptitude Software Group (LSE:APTD) | £2.84 | £5.15 | 44.9% |

| NIOX Group (AIM:NIOX) | £0.614 | £1.10 | 44% |

| On the Beach Group (LSE:OTB) | £2.61 | £4.78 | 45.4% |

| Trainline (LSE:TRN) | £2.88 | £5.17 | 44.3% |

| ECO Animal Health Group (AIM:EAH) | £0.65 | £1.28 | 49.1% |

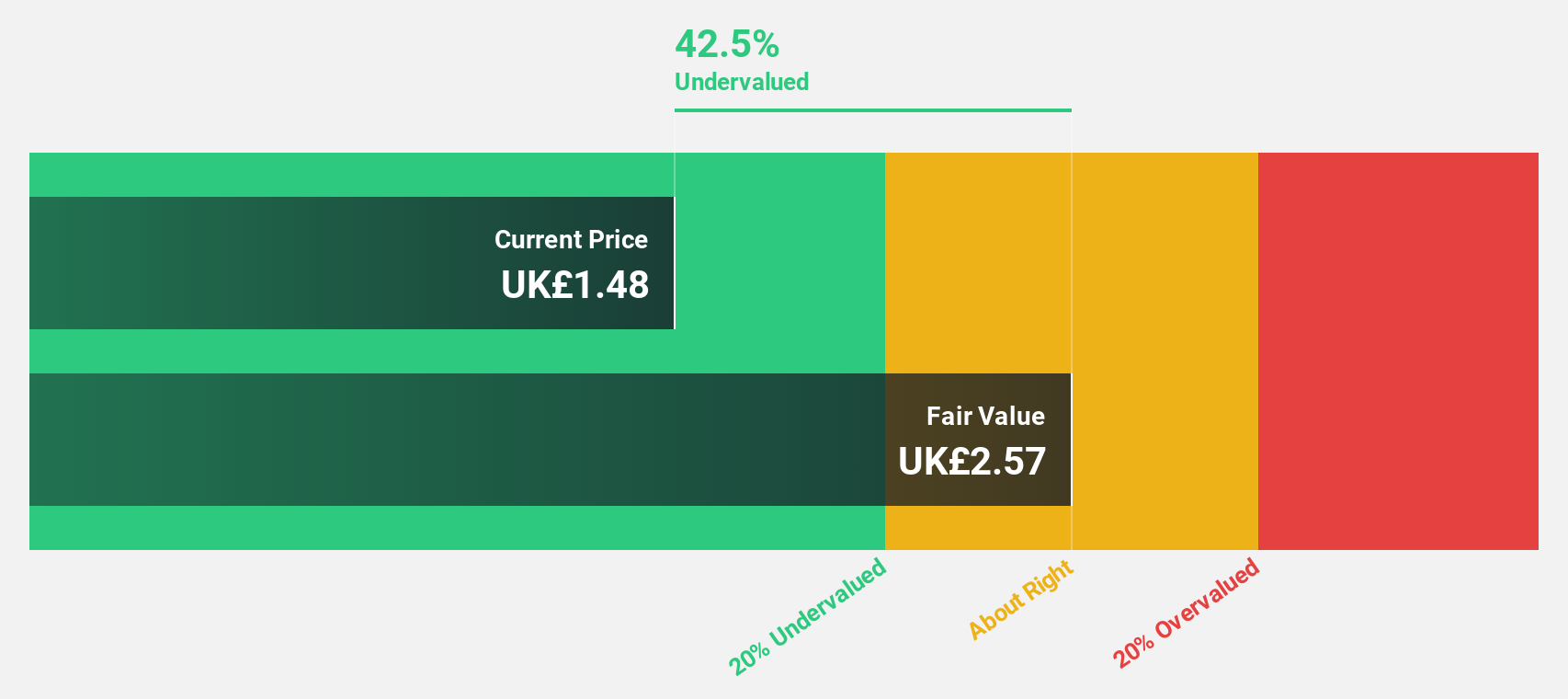

| Deliveroo (LSE:ROO) | £1.466 | £2.67 | 45.1% |

| Kromek Group (AIM:KMK) | £0.051 | £0.10 | 49.6% |

| Ibstock (LSE:IBST) | £1.76 | £3.25 | 45.9% |

| CVS Group (AIM:CVSG) | £10.14 | £18.50 | 45.2% |

Here's a peek at a few of the choices from the screener.

Franchise Brands (AIM:FRAN)

Overview: Franchise Brands plc operates in franchising and related activities across the United Kingdom, Ireland, North America, and Continental Europe with a market cap of £268.59 million.

Operations: The company's revenue is primarily derived from its segments: Pirtek (£63.91 million), Water & Waste Services (£46.05 million), Filta International (£25.60 million), B2C Division (£5.75 million), and Azura (£0.81 million).

Estimated Discount To Fair Value: 43.5%

Franchise Brands plc appears undervalued, trading at 43.5% below its estimated fair value of £2.47 per share. The company reported significant earnings growth of 143.9% over the past year, with net income rising to £7.28 million from £2.99 million a year ago, and is forecasted to continue growing earnings at 29.4% annually, outpacing the UK market average of 13.7%. Recent strategic initiatives aim to enhance operational efficiency and reduce debt further supporting its valuation prospects.

- Upon reviewing our latest growth report, Franchise Brands' projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Franchise Brands stock in this financial health report.

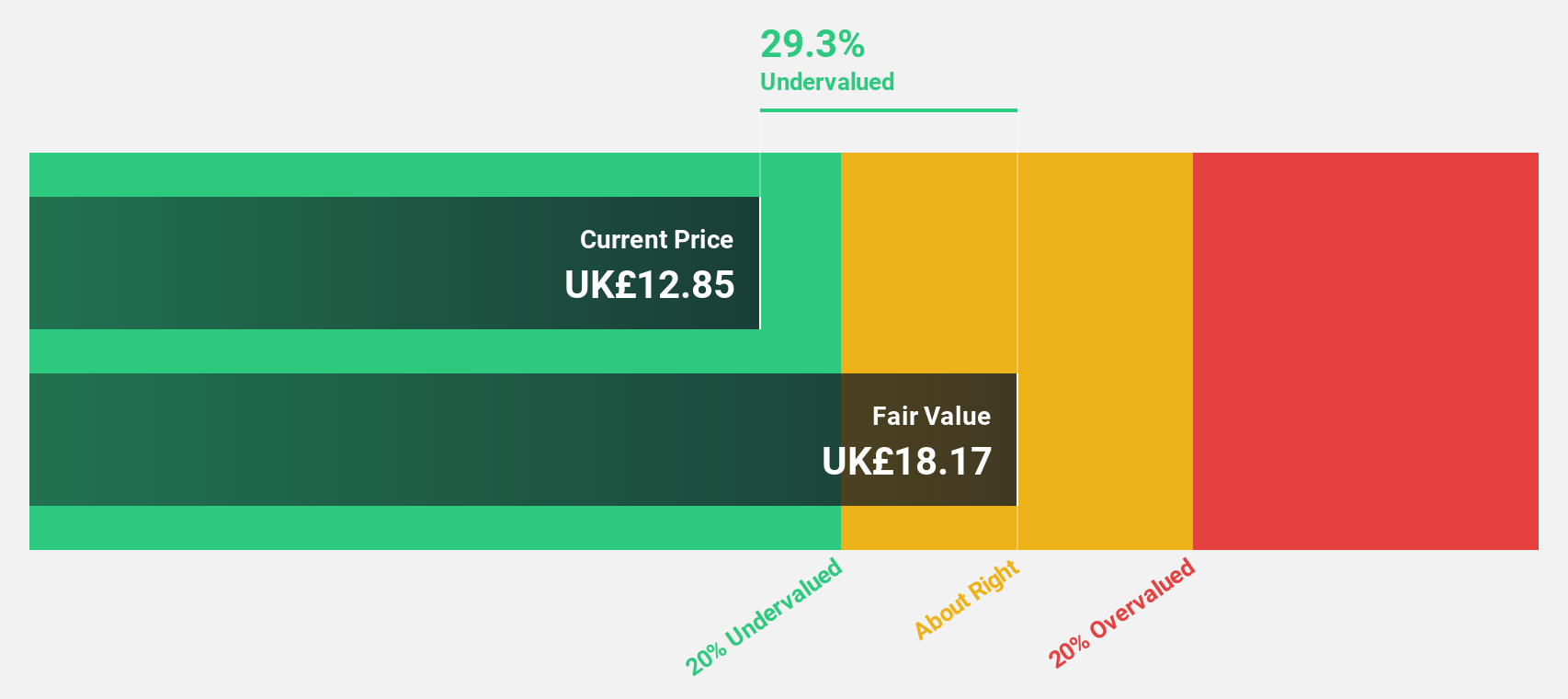

Nichols (AIM:NICL)

Overview: Nichols plc, with a market cap of £447.50 million, is involved in supplying soft drinks to various sectors including retail, wholesale, catering, licensed, and leisure industries across the United Kingdom and international markets such as the Middle East and Africa.

Operations: The company's revenue is primarily derived from its Packaged segment, which accounts for £132.82 million, and the Out of Home segment, contributing £39.99 million.

Estimated Discount To Fair Value: 33.2%

Nichols plc is trading at £12.25, significantly below its estimated fair value of £18.33, indicating a potential undervaluation based on cash flows. Despite a slight dip in net income to £17.84 million from the previous year, Nichols maintains strong cash generation, supporting an increased dividend of 32p per share for 2024. Forecasted earnings growth of 14.8% annually surpasses the UK market average and highlights Nichols' potential for future profitability amidst recent executive changes impacting leadership stability.

- According our earnings growth report, there's an indication that Nichols might be ready to expand.

- Take a closer look at Nichols' balance sheet health here in our report.

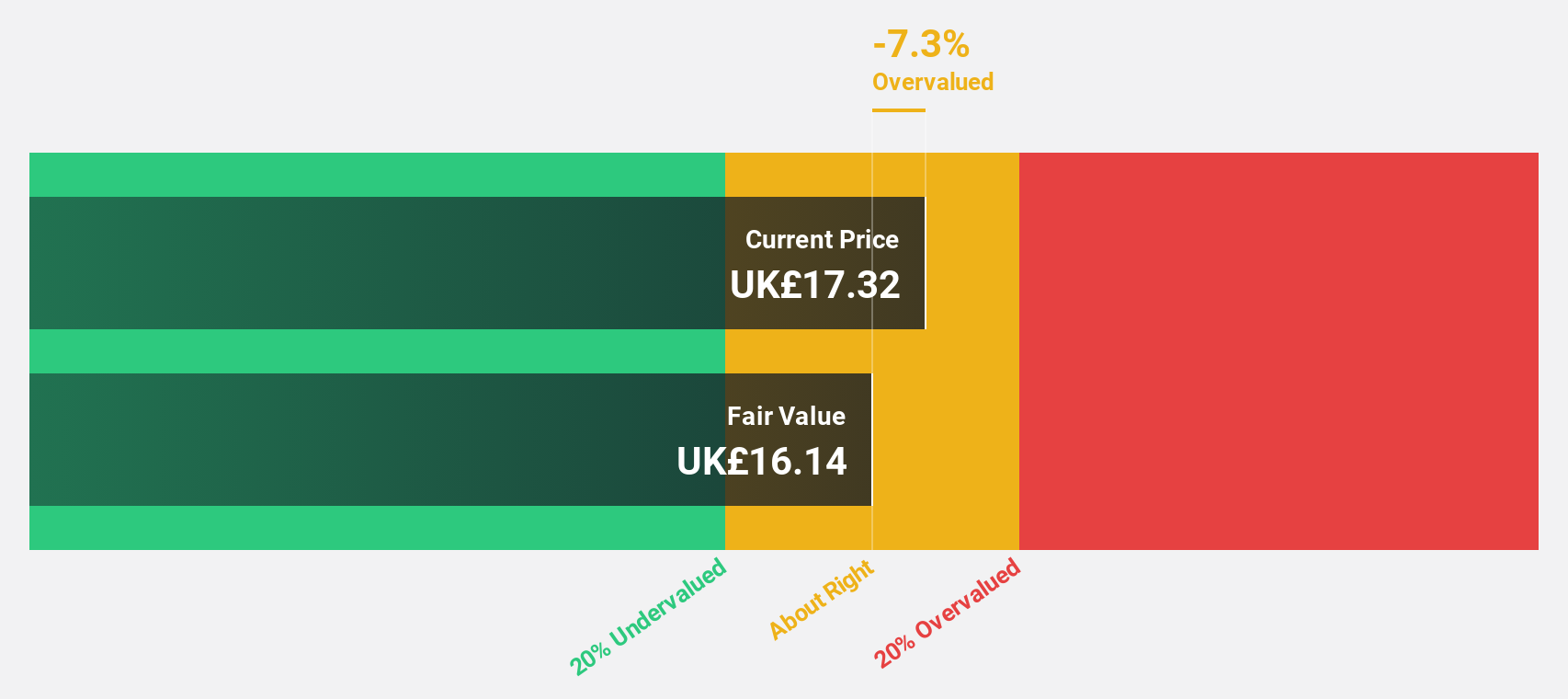

Avon Technologies (LSE:AVON)

Overview: Avon Technologies Plc, with a market cap of £406.93 million, specializes in providing respiratory and head protection products for military and first responder markets in Europe and the United States.

Operations: The company's revenue is derived from its Team Wendy segment, contributing $129.40 million, and the Avon Protection segment, which accounts for $145.60 million.

Estimated Discount To Fair Value: 20.2%

Avon Technologies, trading at £13.70, is significantly below its estimated fair value of £17.17, highlighting a potential undervaluation based on cash flows. Recent corporate guidance suggests stronger-than-expected revenue and operating profit margins for 2025 due to increased demand and efficiency improvements in Avon Protection. Although earnings are forecasted to grow significantly at 53.82% annually over the next three years, low return on equity and large one-off items may impact financial results.

- Insights from our recent growth report point to a promising forecast for Avon Technologies' business outlook.

- Get an in-depth perspective on Avon Technologies' balance sheet by reading our health report here.

Key Takeaways

- Click this link to deep-dive into the 53 companies within our Undervalued UK Stocks Based On Cash Flows screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nichols might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:NICL

Nichols

Engages in supply of soft drinks to the retail, wholesale, catering, licensed, and leisure industries in the United Kingdom, the Middle East, Africa, and internationally.

Excellent balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor