Advertisement

- United Kingdom

- /

- Machinery

- /

- LSE:GDWN

Exploring April 2025 Undiscovered Gems in the UK Market

Simply Wall St

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 index faces headwinds from weak trade data out of China, impacting companies heavily reliant on commodity exports and global demand, investors are increasingly looking towards small-cap opportunities that may offer resilience amidst broader market volatility. In this environment, identifying stocks with strong fundamentals and growth potential becomes crucial for those seeking to uncover hidden gems in the UK market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| BioPharma Credit | NA | 7.22% | 7.91% | ★★★★★★ |

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| Livermore Investments Group | NA | 9.92% | 13.65% | ★★★★★★ |

| MS INTERNATIONAL | NA | 13.42% | 56.55% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -7.87% | -8.41% | ★★★★★★ |

| Goodwin | 37.02% | 9.75% | 15.68% | ★★★★★☆ |

| FW Thorpe | 2.95% | 11.79% | 13.49% | ★★★★★☆ |

| AltynGold | 77.07% | 28.64% | 38.10% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Griffin Mining (AIM:GFM)

Simply Wall St Value Rating: ★★★★★★

Overview: Griffin Mining Limited is a mining and investment company focused on the exploration and development of mineral properties, with a market capitalization of £313.29 million.

Operations: Griffin Mining Limited generates revenue primarily from the Caijiaying Zinc Gold Mine, contributing $162.25 million.

Griffin Mining, a nimble player in the UK mining sector, showcases impressive earnings growth of 116.5% over the past year, outpacing the industry’s 5.2%. Despite no debt on its books for five years, Griffin's recent production figures reveal some challenges with ore mined dropping to 1.15 million tonnes from 1.51 million tonnes last year and zinc output at 39,444 tonnes compared to last year's 56,933 tonnes. Trading at roughly 41.8% below estimated fair value suggests potential upside as it navigates these hurdles while maintaining high-quality earnings and forecasting an annual growth of about 18.52%.

- Unlock comprehensive insights into our analysis of Griffin Mining stock in this health report.

Gain insights into Griffin Mining's past trends and performance with our Past report.

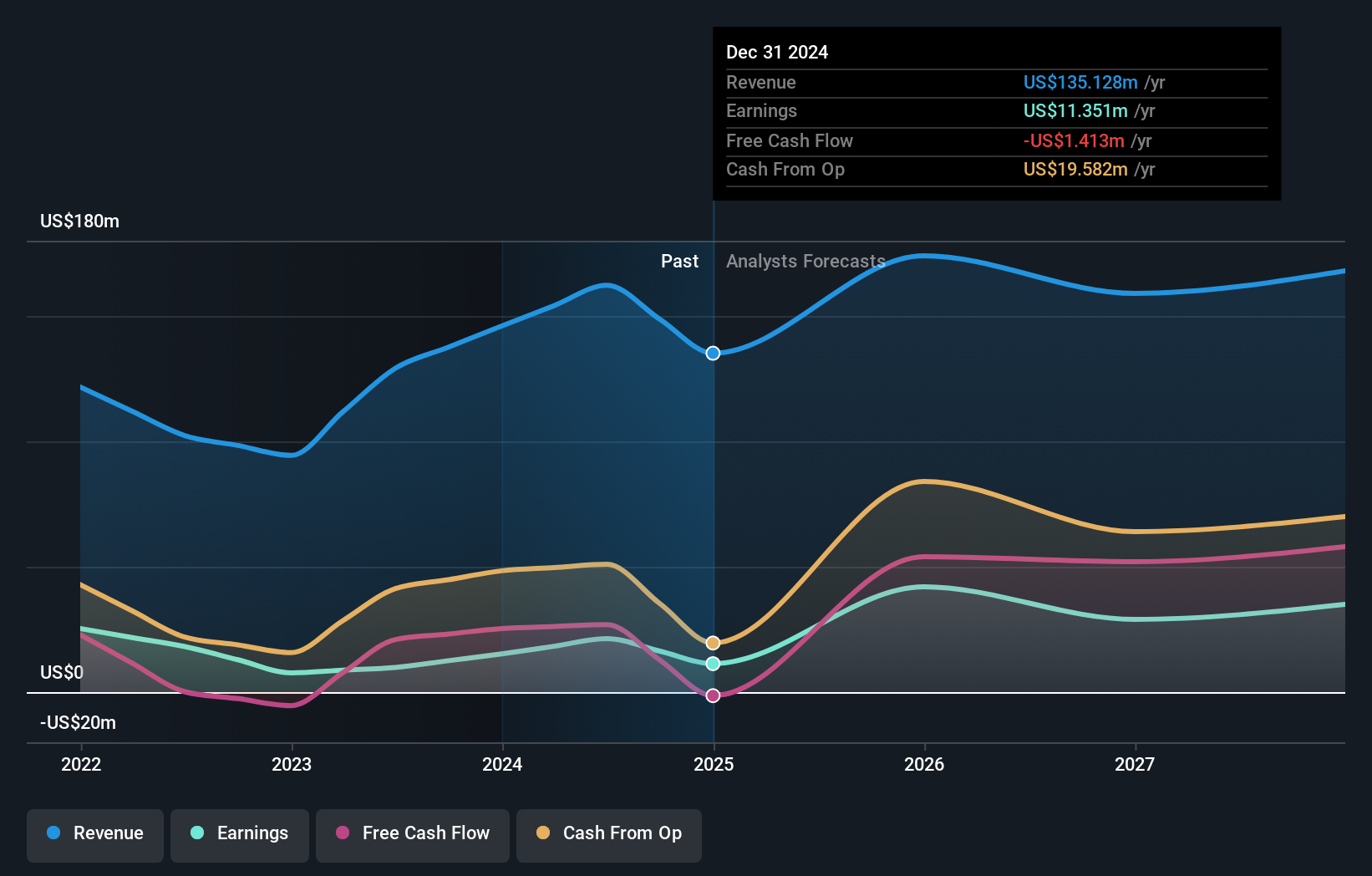

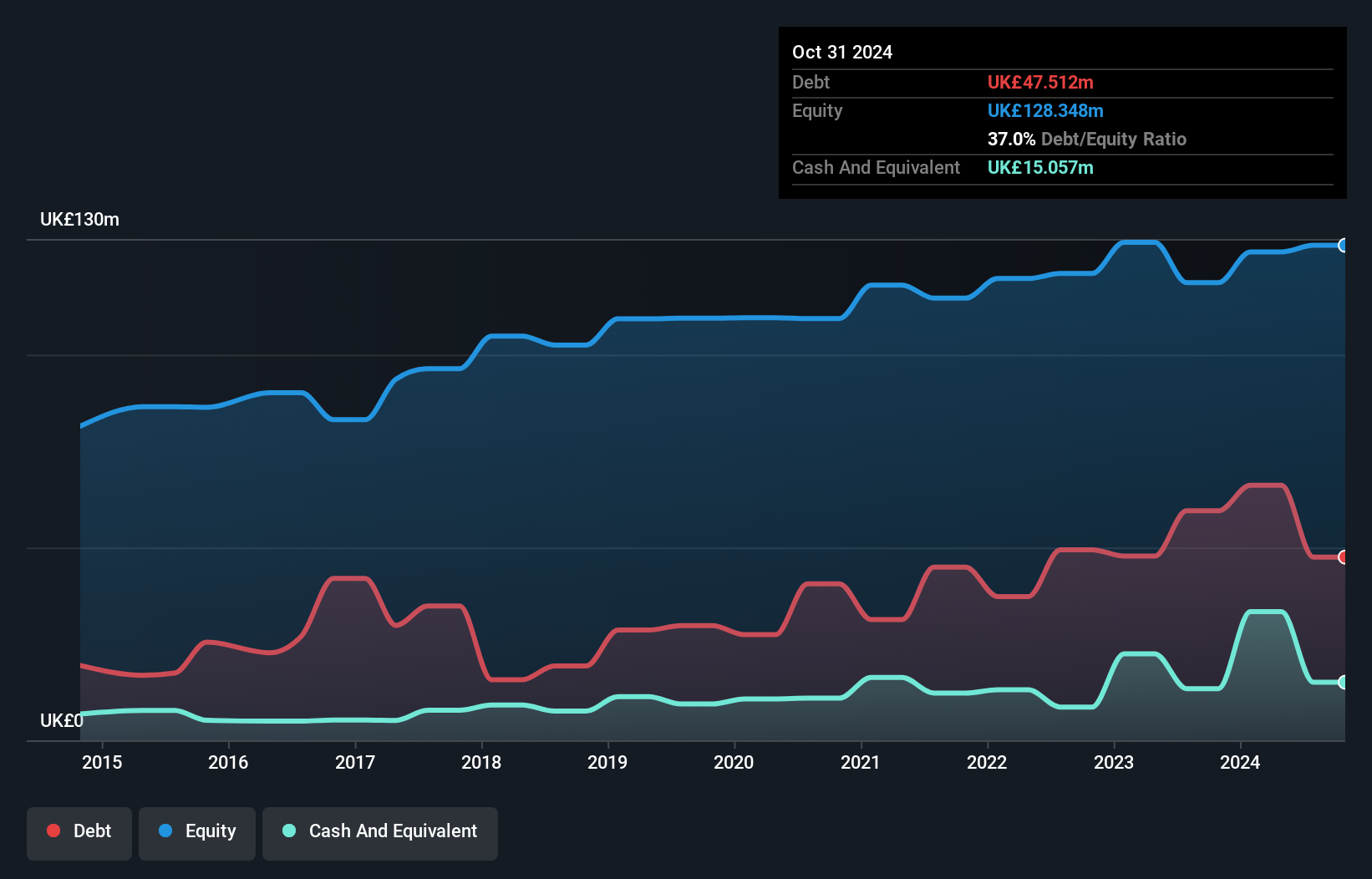

Goodwin (LSE:GDWN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Goodwin PLC, along with its subsidiaries, offers mechanical and refractory engineering solutions across various regions including the United Kingdom, Europe, the United States, and the Pacific Basin, with a market cap of £498.64 million.

Operations: Goodwin PLC generates revenue primarily from its mechanical segment (£168.02 million) and refractory segment (£75.58 million). The company has a market cap of £498.64 million.

With a knack for delivering high-quality earnings, Goodwin seems to be carving out its niche in the machinery space. The company boasts an impressive 22.9% earnings growth over the past year, outpacing the industry average of 3.2%. Its net debt to equity ratio stands at a satisfactory 25.3%, and interest payments are well-covered with EBIT at 8.4 times coverage. Trading at 61% below estimated fair value, it offers potential upside for investors seeking undervalued opportunities. Recent announcements include a dividend increase, reinforcing its commitment to shareholder returns amidst solid financial health and positive cash flow trends.

- Navigate through the intricacies of Goodwin with our comprehensive health report here.

Assess Goodwin's past performance with our detailed historical performance reports.

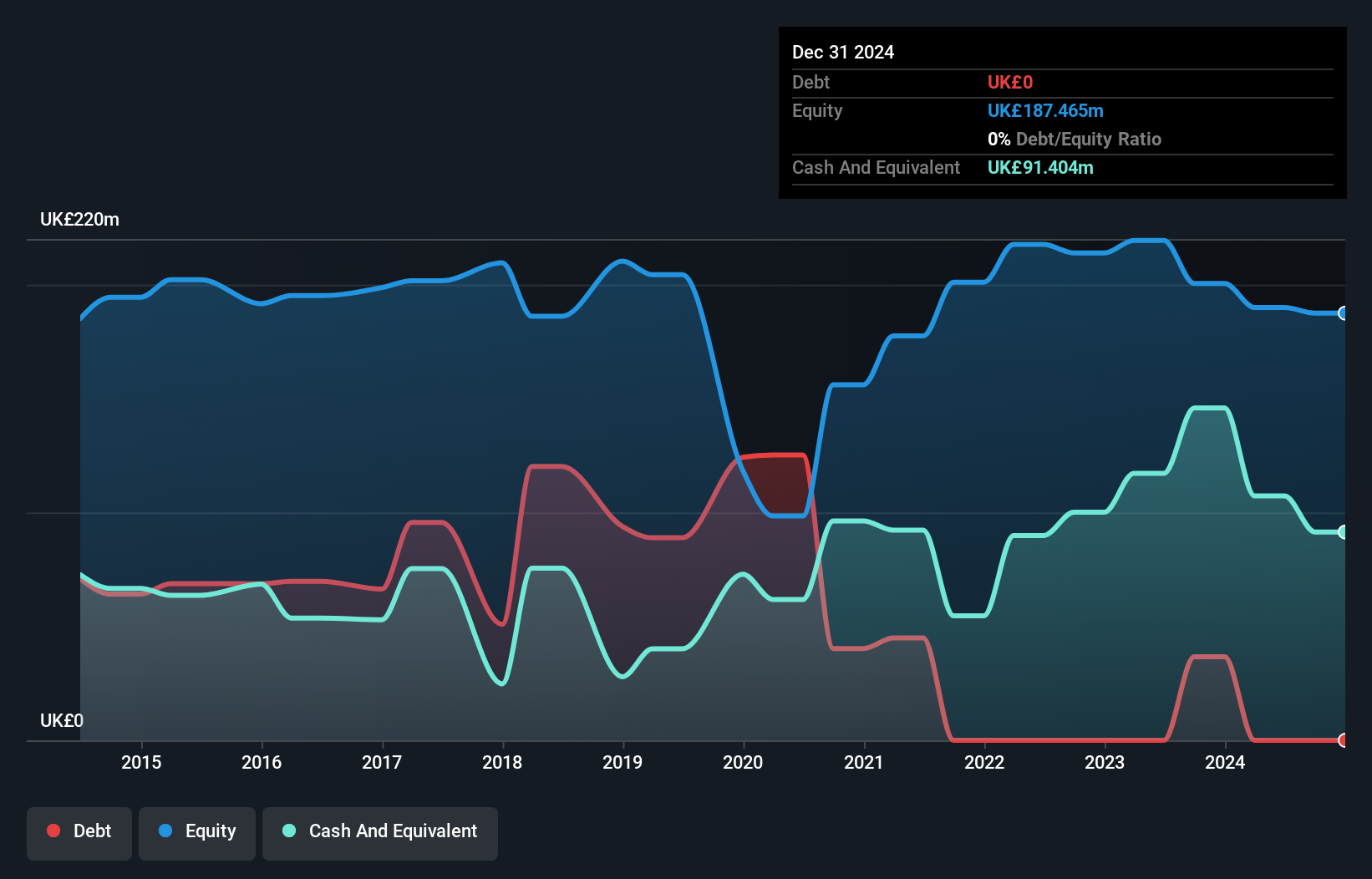

Mears Group (LSE:MER)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mears Group plc, along with its subsidiaries, offers a range of outsourced services to both public and private sectors in the UK, with a market capitalization of £315.52 million.

Operations: Mears Group generates revenue primarily from its Management and Maintenance segments, with Management contributing £591.63 million and Maintenance adding £551.73 million. The company has a market capitalization of £315.52 million.

Mears Group, a small player in the UK market, is debt-free with a price-to-earnings ratio of 7.5x, well below the UK market average of 14.1x, suggesting it trades at an attractive valuation relative to peers. The company has impressively reduced its debt from a 43.5% debt-to-equity ratio five years ago to zero now, highlighting strong financial management. Earnings surged by 42.6% last year, outpacing the Commercial Services industry growth of 20.7%. However, future prospects appear challenging with earnings expected to decline by an average of 13.8% annually over the next three years despite high-quality past earnings performance.

- Take a closer look at Mears Group's potential here in our health report.

Examine Mears Group's past performance report to understand how it has performed in the past.

Where To Now?

- Embark on your investment journey to our 58 UK Undiscovered Gems With Strong Fundamentals selection here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:GDWN

Goodwin

Provides mechanical and refractory engineering solutions primarily in the United Kingdom, rest of Europe, the United States, the Pacific Basin, and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor