Advertisement

- United Kingdom

- /

- Building

- /

- LSE:ECEL

Most Shareholders Will Probably Find That The CEO Compensation For Eurocell plc (LON:ECEL) Is Reasonable

The share price of Eurocell plc (LON:ECEL) has been growing in the past few years, however, the per-share earnings growth has been lacking, suggesting something is amiss. Some of these issues will occupy shareholders' minds as the AGM rolls around on 13 May 2021. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From what we gathered, we think shareholders should be wary of raising CEO compensation until the company shows some marked improvement.

Check out our latest analysis for Eurocell

How Does Total Compensation For Mark Kelly Compare With Other Companies In The Industry?

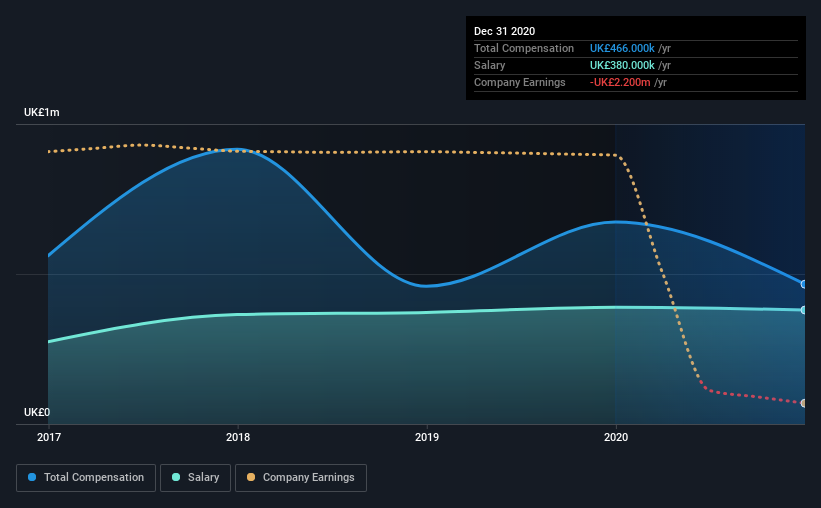

Our data indicates that Eurocell plc has a market capitalization of UK£288m, and total annual CEO compensation was reported as UK£466k for the year to December 2020. Notably, that's a decrease of 31% over the year before. Notably, the salary which is UK£380.0k, represents most of the total compensation being paid.

On comparing similar companies from the same industry with market caps ranging from UK£144m to UK£576m, we found that the median CEO total compensation was UK£537k. So it looks like Eurocell compensates Mark Kelly in line with the median for the industry. What's more, Mark Kelly holds UK£417k worth of shares in the company in their own name.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | UK£380k | UK£389k | 82% |

| Other | UK£86k | UK£284k | 18% |

| Total Compensation | UK£466k | UK£673k | 100% |

On an industry level, roughly 65% of total compensation represents salary and 35% is other remuneration. Eurocell is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Eurocell plc's Growth Numbers

Eurocell plc has reduced its earnings per share by 53% a year over the last three years. It saw its revenue drop 7.5% over the last year.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Eurocell plc Been A Good Investment?

Eurocell plc has served shareholders reasonably well, with a total return of 17% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Despite the positive returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about whether these returns will continue. In the upcoming AGM, shareholders will get the opportunity to discuss any concerns with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

So you may want to check if insiders are buying Eurocell shares with their own money (free access).

Switching gears from Eurocell, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Eurocell, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eurocell might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:ECEL

Eurocell

Engages in manufacture, distribution, and recycling of windows, doors, and roofline polyvinyl chloride (PVC) building products in the United Kingdom and the Republic of Ireland.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets