- United Kingdom

- /

- Electrical

- /

- AIM:TFW

FW Thorpe And 2 Promising Small Caps To Consider For Your Portfolio

Reviewed by Simply Wall St

The United Kingdom's market has recently faced challenges, with the FTSE 100 and FTSE 250 indices both closing lower amid weak trade data from China. As global economic uncertainties persist, investors are increasingly looking for resilient small-cap stocks that can offer potential growth despite broader market volatility. In this article, we explore FW Thorpe and two other promising small-cap companies that could be valuable additions to your portfolio.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| Georgia Capital | NA | -27.80% | 18.94% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Fix Price Group | 43.59% | 12.53% | 23.49% | ★★★★★☆ |

| Ros Agro | 49.06% | 17.05% | 17.70% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

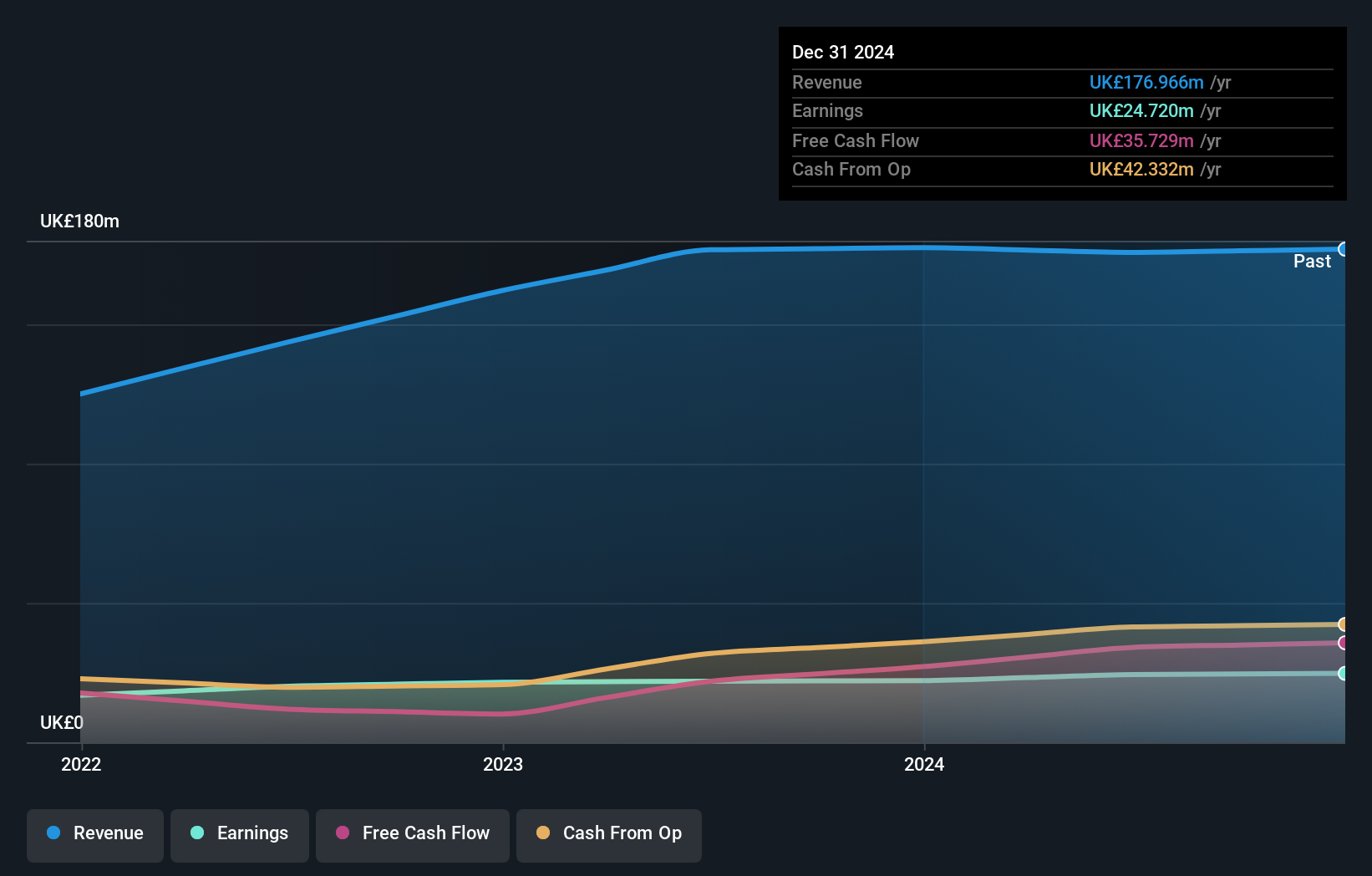

FW Thorpe (AIM:TFW)

Simply Wall St Value Rating: ★★★★★☆

Overview: FW Thorpe Plc, with a market cap of £422.43 million, designs, manufactures, and supplies professional lighting equipment across the United Kingdom, the Netherlands, Germany, rest of Europe, and internationally.

Operations: Thorlux is the primary revenue driver for FW Thorpe, generating £104.65 million, followed by Netherlands Companies and Zemper Group contributing £37.80 million and £19.62 million respectively.

FW Thorpe, a small cap in the UK, has seen its debt to equity ratio rise from 0% to 3.3% over five years. Despite this, it boasts high-quality earnings and trades at 51.2% below estimated fair value. Its earnings growth of 2.6% last year outpaced the Electrical industry’s -3.9%. The company is free cash flow positive and has more cash than total debt, with EBIT covering interest payments by an impressive 2805x margin.

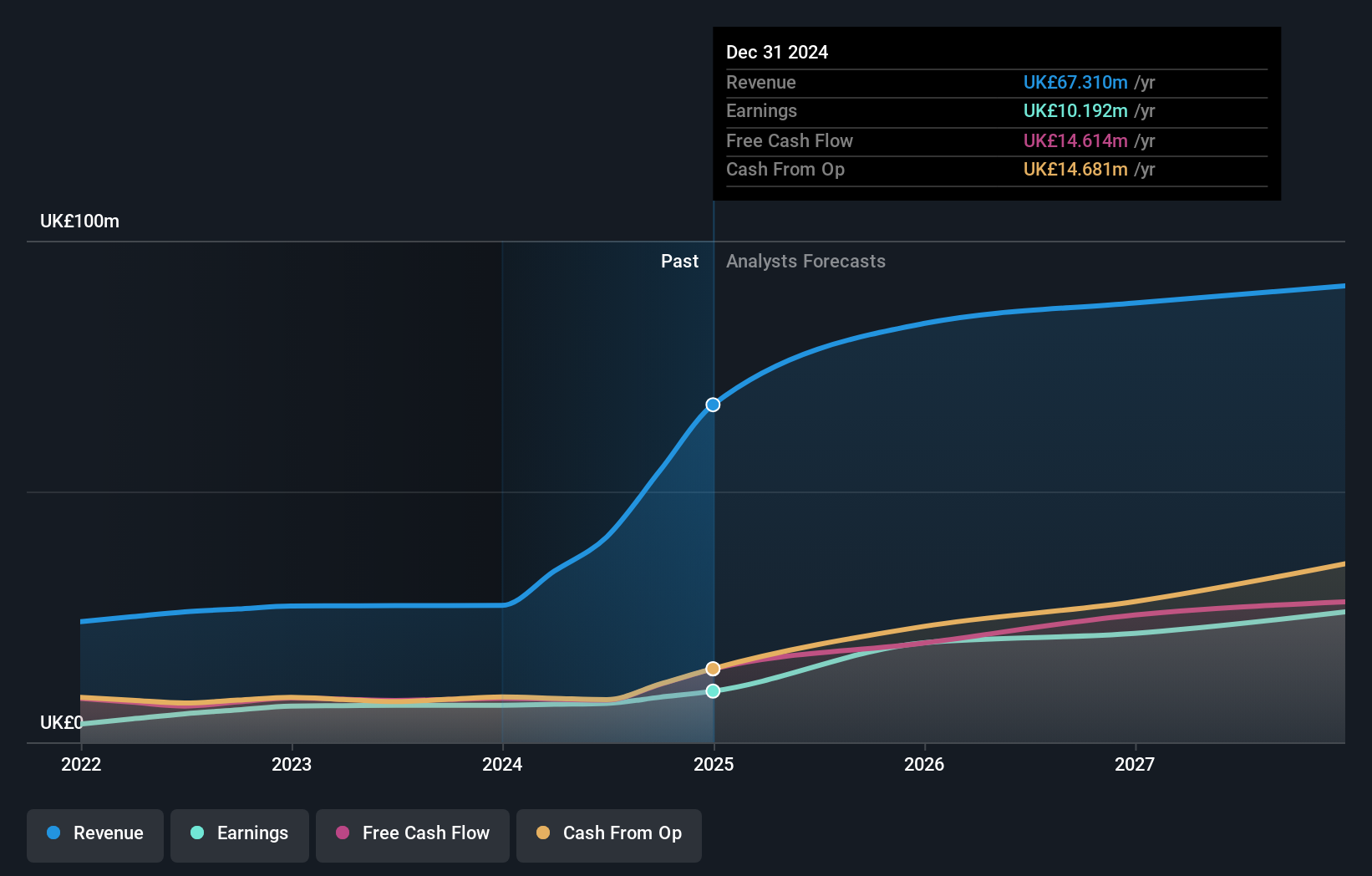

Property Franchise Group (AIM:TPFG)

Simply Wall St Value Rating: ★★★★★★

Overview: The Property Franchise Group PLC manages and leases residential real estate properties in the United Kingdom with a market cap of £288.58 million.

Operations: The company's revenue streams include £1.50 million from Financial Services and £25.78 million from Property Franchising, totaling approximately £27.28 million.

TPFG's earnings have grown 20.6% annually over the past five years, with a debt to equity ratio decreasing from 10.2% to 6.1%. Currently trading at 60.3% below its estimated fair value, the company has high-quality earnings, although shareholders faced substantial dilution last year. With EBIT covering interest payments by 26.6 times and profitability ensuring no cash runway issues, TPFG's forecasted annual earnings growth is projected at an impressive 36.71%.

- Click here and access our complete health analysis report to understand the dynamics of Property Franchise Group.

Gain insights into Property Franchise Group's past trends and performance with our Past report.

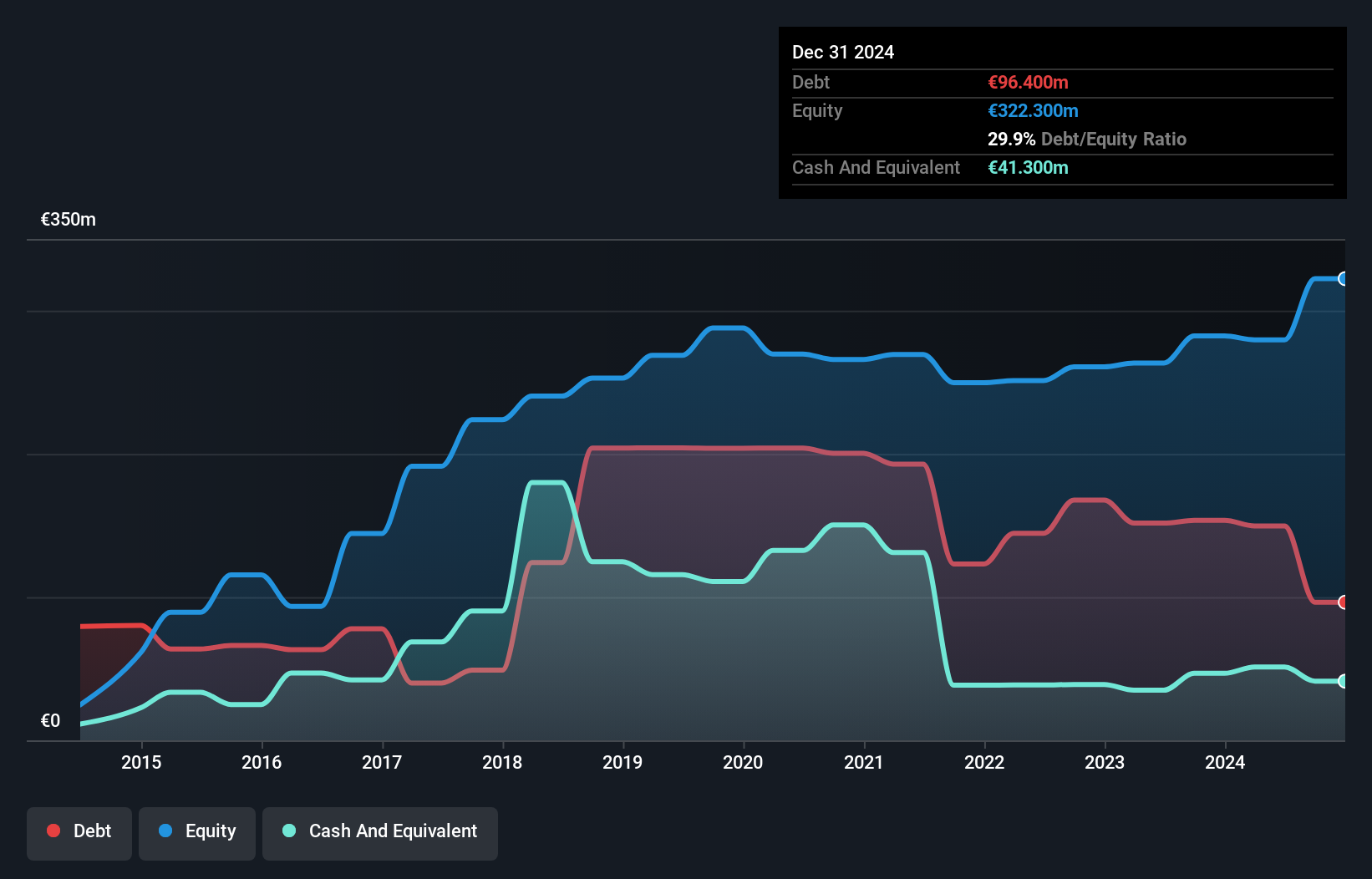

Irish Continental Group (LSE:ICGC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Irish Continental Group plc operates as a maritime transport company with a market cap of £753.55 million.

Operations: The company generates revenue primarily from its Ferries segment (€412.30 million) and Container and Terminal segment (€194.10 million).

Irish Continental Group (ICG) has shown promising performance with a 3% earnings growth over the past year, outpacing the shipping industry's -6.5%. The company's net debt to equity ratio stands at 37.8%, which is satisfactory, and its interest payments are well covered by EBIT at 10.9x coverage. Recent figures highlight an 8.3% revenue increase to €177 million for the first four months of 2024, alongside higher car volumes and RoRo Freight volumes compared to last year.

- Dive into the specifics of Irish Continental Group here with our thorough health report.

Evaluate Irish Continental Group's historical performance by accessing our past performance report.

Taking Advantage

- Unlock more gems! Our UK Undiscovered Gems With Strong Fundamentals screener has unearthed 76 more companies for you to explore.Click here to unveil our expertly curated list of 79 UK Undiscovered Gems With Strong Fundamentals.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:TFW

FW Thorpe

Designs, manufactures, and supplies professional lighting equipment in the United Kingdom, the Netherlands, Germany, rest of Europe, and internationally.

Excellent balance sheet and fair value.