Advertisement

- United Kingdom

- /

- Banks

- /

- LSE:HSBA

HSBC (LSE:HSBA): Exploring Valuation After Recent Share Price Upswing

Simply Wall St

Reviewed by Simply Wall St

HSBC Holdings (LSE:HSBA) shares have traded with some swings recently, catching the attention of investors curious about what might be driving momentum. Over the past month, the stock is up almost 5%.

See our latest analysis for HSBC Holdings.

HSBC’s run higher this past month, with a 1-month share price return of 4.9%, extends a powerful longer-term rally. The bank’s total shareholder return has surged over 50% in the past year and more than doubled over three years. Recent volatility has not dented overall momentum, as robust profit growth and improving sentiment continue to keep HSBC in the spotlight.

If you’re looking to expand beyond the banking sector, now’s a great opportunity to discover fast growing stocks with high insider ownership.

With rapid gains and positive sentiment at its back, the question facing investors now is whether HSBC’s current share price leaves room for further upside or if the market has already priced in all of its expected growth.

Most Popular Narrative: 3.3% Undervalued

HSBC’s latest fair value assessment puts its worth slightly above the last close, hinting that analyst enthusiasm persists despite muted price moves. Here is a look into the story driving these expectations.

The bank is intensifying investment in Asian wealth management and private banking, leveraging a strong brand and local presence in fast-growing wealth markets like Hong Kong, mainland China, and Southeast Asia. This positions HSBC to capture rising affluence and middle class expansion, fueling future growth in fee income and supporting more resilient earnings and higher margins.

Craving the real numbers pushing this narrative? The valuation rests on a bold bet about soaring margins and a multi-year surge for both revenue and profits. What are the surprising growth levers that set this price target? Only the full projection tells all.

Result: Fair Value of $10.77 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent uncertainty in Asian markets or a prolonged downturn in Hong Kong commercial real estate could undermine HSBC’s strong profit momentum and growth outlook.

Find out about the key risks to this HSBC Holdings narrative.

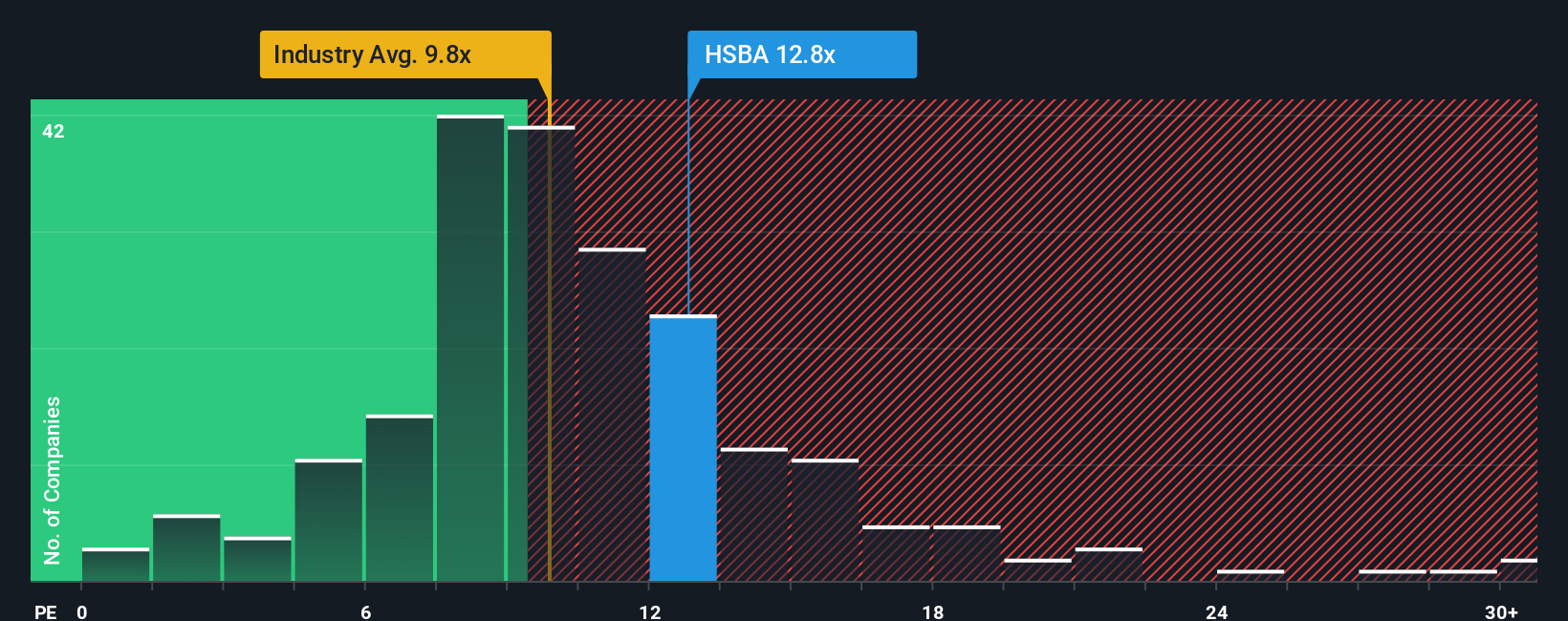

Another View: Valuation by Peer Comparison

While the narrative suggests HSBC is undervalued, a closer look at its price-to-earnings ratio tells a different story. HSBC trades at 14.1x earnings, noticeably above both its peer average of 10.7x and the industry average of 9.8x. The fair ratio points even lower at 9.9x. This premium signals that investors have high expectations. Are they justified, or are they taking on extra valuation risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own HSBC Holdings Narrative

If you see things differently or want to take a deeper dive into the numbers, you can put together your own story in just minutes: Do it your way.

A great starting point for your HSBC Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don't sit on the sidelines while tomorrow's winners get away. Stand out from the crowd by exploring alternative opportunities ready to reshape your portfolio and build lasting wealth.

- Maximize your income potential by targeting top performers offering attractive yields. Use these 17 dividend stocks with yields > 3% to spot the strongest dividend payers on the market.

- Seize growth as artificial intelligence transforms entire industries. Assess prospects among these 25 AI penny stocks set for technological disruption.

- Ride the momentum of digital innovation and market volatility by checking out these 81 cryptocurrency and blockchain stocks powering the blockchain and cryptocurrency ecosystem.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HSBC Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HSBA

HSBC Holdings

Engages in the provision of banking and financial products and services worldwide.

Adequate balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor