Advertisement

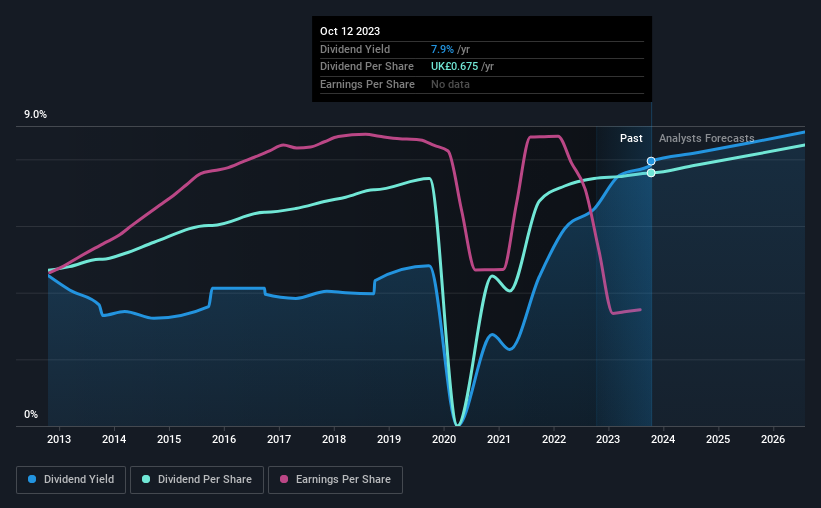

The board of Close Brothers Group plc (LON:CBG) has announced that it will be paying its dividend of £0.45 on the 24th of November, an increased payment from last year's comparable dividend. This takes the dividend yield to 7.9%, which shareholders will be pleased with.

Check out our latest analysis for Close Brothers Group

Close Brothers Group's Payment Expected To Have Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable.

Having distributed dividends for at least 10 years, Close Brothers Group has a long history of paying out a part of its earnings to shareholders. Past distributions unfortunately do not guarantee future ones, and Close Brothers Group's last earnings report actually showed that the company went over its net earnings in its total dividend distribution. This is an alarming sign for the sustainability of its dividends, as it may mean that Close Brothers Groupis pulling cash from elsewhere to keep its shareholders happy.

Over the next 3 years, EPS is forecast to expand by 145.3%. For the same time horizon, analysts estimate that the future payout ratio could be 55% which would be quite comfortable going to take the dividend forward.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The annual payment during the last 10 years was £0.415 in 2013, and the most recent fiscal year payment was £0.675. This works out to be a compound annual growth rate (CAGR) of approximately 5.0% a year over that time. We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments the total shareholder return may be limited.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Close Brothers Group's EPS has fallen by approximately 17% per year during the past five years. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

Close Brothers Group's Dividend Doesn't Look Sustainable

Overall, we always like to see the dividend being raised, but we don't think Close Brothers Group will make a great income stock. The payments are bit high to be considered sustainable, and the track record isn't the best. We don't think Close Brothers Group is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for Close Brothers Group that investors need to be conscious of moving forward. Is Close Brothers Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:CBG

Close Brothers Group

A merchant banking company, engages in the provision of financial services to small businesses and individuals in the United Kingdom.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor