Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Aston Martin Lagonda Global Holdings plc (LON:AML) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Aston Martin Lagonda Global Holdings

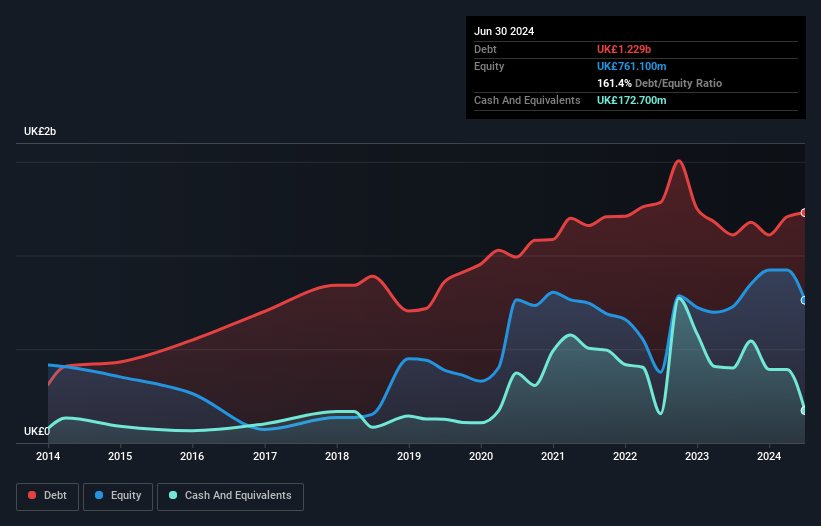

What Is Aston Martin Lagonda Global Holdings's Debt?

As you can see below, at the end of June 2024, Aston Martin Lagonda Global Holdings had UK£1.23b of debt, up from UK£1.11b a year ago. Click the image for more detail. However, it does have UK£172.7m in cash offsetting this, leading to net debt of about UK£1.06b.

A Look At Aston Martin Lagonda Global Holdings' Liabilities

Zooming in on the latest balance sheet data, we can see that Aston Martin Lagonda Global Holdings had liabilities of UK£887.9m due within 12 months and liabilities of UK£1.39b due beyond that. On the other hand, it had cash of UK£172.7m and UK£264.3m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£1.84b.

This deficit casts a shadow over the UK£1.18b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Aston Martin Lagonda Global Holdings would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Aston Martin Lagonda Global Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Aston Martin Lagonda Global Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 2.7%, to UK£1.6b. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Aston Martin Lagonda Global Holdings had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at UK£95m. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through UK£360m in negative free cash flow over the last year. That means it's on the risky side of things. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Aston Martin Lagonda Global Holdings you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:AML

Aston Martin Lagonda Global Holdings

Engages in the design, development, manufacture, and marketing of luxury sports cars in the United Kingdom, the Americas, the Middle East, Africa, rest of Europe, and the Asia Pacific.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor