Advertisement

Here's What We Like About Capgemini SE (EPA:CAP)'s Upcoming Dividend

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Capgemini SE (EPA:CAP) stock is about to trade ex-dividend in the near future. Investors can purchase shares before the 5th of June in order to be eligible for this dividend, which will be paid on the 7th of June.

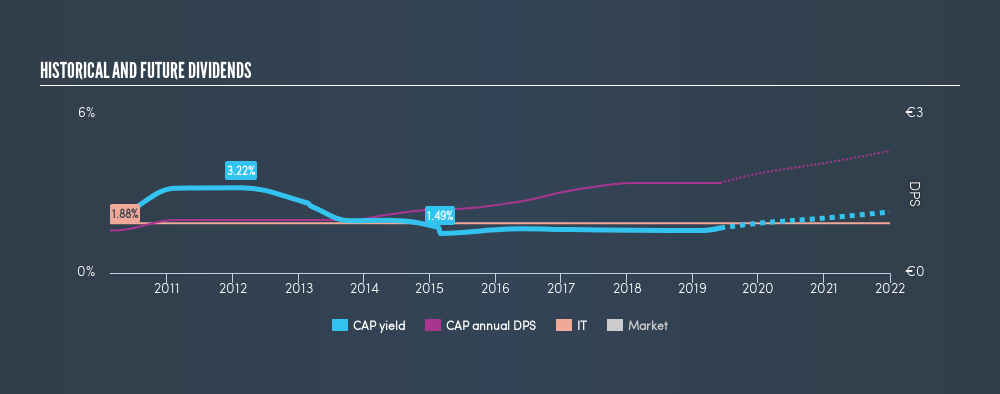

Capgemini's next dividend payment will be €1.70 per share, and in the last 12 months, the company paid a total of €1.70 per share. Calculating the last year's worth of payments shows that Capgemini has a trailing yield of 1.7% on the current share price of €100.1. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! As a result, readers should always check whether Capgemini has been able to grow its dividends, or if the dividend might be cut.

View our latest analysis for Capgemini

Dividends are typically paid out of profits, so if a company pays out more than it earned then its dividend is usually at a higher risk of being cut. Fortunately Capgemini's payout ratio is modest, at just 39% of profit. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. The good news is it paid out just 24% of its free cash flow in the last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. This is why it's a relief to see Capgemini earnings per share are up 9.3% per annum over the last five years.

The company is retaining more than half of its earnings within the business, and it has been growing earnings at a decent rate. We think this is generally an attractive combination, as dividends can grow through a combination of earnings growth and or a higher payout ratio over time.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the last 9 years, Capgemini has lifted its dividend by approximately 8.7% a year on average. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

The Bottom Line

Should investors buy Capgemini for the upcoming dividend? Earnings per share growth has been growing somewhat, and Capgemini is paying out less than half its earnings and cash flow as dividends. This is interesting for a few reasons, as it suggests management may be reinvesting heavily in the business, but it also provides room to increase the dividend in time. It might be nice to see earnings growing faster, but Capgemini is being conservative with its dividend payouts and could still perform reasonably over the long run. Capgemini looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

Ever wonder what professionals think the future holds for Capgemini? See what the 16 analysts we track are forecasting , with this visualisation of its historical and future estimated earnings and cash flow

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:CAP

Capgemini

Provides consulting, digital transformation, technology, and engineering services primarily in North America, France, the United Kingdom, Ireland, the rest of Europe, the Asia-Pacific, and Latin America.

Very undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor