Atos (ENXTPA:ATO) recently achieved a 94% price increase during the last quarter, bolstered by strategic client announcements and restructuring efforts. The integration of AI in its Selartag® solution and a significant contract with the UK's DEFRA reflect effective innovation and client engagement. Additions like Pierre-Yves Jolivet as EVP and a recovery to a net income of €248 million also likely influenced investor confidence, despite a previous year's revenue decline. These factors may have amplified Atos's market performance compared to the overall 8% rise observed in the broader market over the past 12 months.

We've identified 5 warning signs for Atos (4 can't be ignored) that you should be aware of.

The recent developments at Atos, including strategic client engagements and leadership changes, might invigorate the company's financial health despite the challenges. Over the past year, the total return, encompassing share price and dividends, witnessed a significant reduction of 72.49%. While the recent quarterly 94% recovery shows positive momentum, it contrasts starkly with this longer-term trend. This indicates a volatile investor sentiment in the face of systemic restructuring and market conditions.

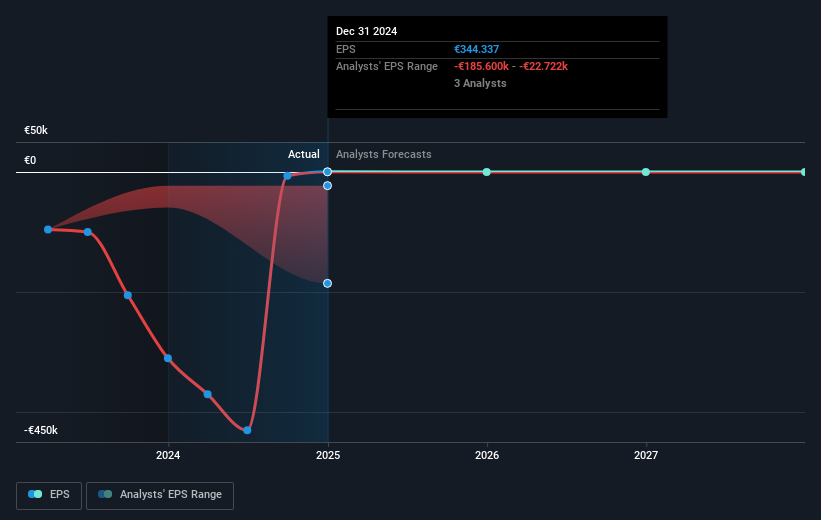

Relative to the broader French IT industry, which returned -24.9% over the past year, Atos underperformed, signaling persistent challenges in capitalizing on industry-wide growth. This also shows a pronounced divergence from the broader market's overall returns, highlighting the company's unique hurdles. Despite restructuring and operational adjustments aimed at efficiency, the firm's revenue forecasts still suggest declines, averaging -3.2% annually over the next three years, with earnings expected to contract by 42.7% per year.

In light of these dynamics, current share valuations appear heavily discounted compared to the consensus price target of €393.5. Although share price gains provide a brief optimistic outlook, achieving this target would require a dramatic enhancement in financial performance beyond analysts' current projections. Therefore, while the news underscores efforts toward turnaround, sustaining growth and closing the valuation gap remains a formidable task for Atos.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:ATO

Atos

Provides digital transformation solutions and services in France and internationally.

Moderate and fair value.

Similar Companies

Market Insights

Community Narratives