Advertisement

Despite Its High P/E Ratio, Is Alten SA (EPA:ATE) Still Undervalued?

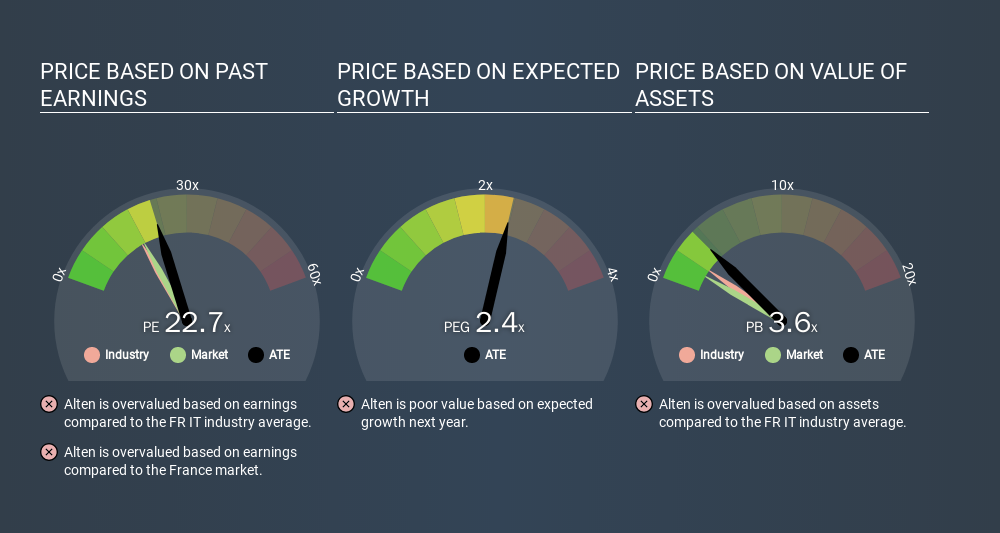

This article is written for those who want to get better at using price to earnings ratios (P/E ratios). To keep it practical, we'll show how Alten SA's (EPA:ATE) P/E ratio could help you assess the value on offer. Alten has a P/E ratio of 22.68, based on the last twelve months. That means that at current prices, buyers pay €22.68 for every €1 in trailing yearly profits.

See our latest analysis for Alten

How Do I Calculate A Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Alten:

P/E of 22.68 = €108.20 ÷ €4.77 (Based on the year to June 2019.)

Is A High P/E Ratio Good?

A higher P/E ratio means that buyers have to pay a higher price for each €1 the company has earned over the last year. That isn't a good or a bad thing on its own, but a high P/E means that buyers have a higher opinion of the business's prospects, relative to stocks with a lower P/E.

Does Alten Have A Relatively High Or Low P/E For Its Industry?

We can get an indication of market expectations by looking at the P/E ratio. The image below shows that Alten has a higher P/E than the average (17.0) P/E for companies in the it industry.

That means that the market expects Alten will outperform other companies in its industry. Shareholders are clearly optimistic, but the future is always uncertain. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. A lower P/E should indicate the stock is cheap relative to others -- and that may attract buyers.

Alten's earnings per share grew by -6.9% in the last twelve months. And earnings per share have improved by 17% annually, over the last five years.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. So it won't reflect the advantage of cash, or disadvantage of debt. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

Alten's Balance Sheet

Net debt totals just 0.5% of Alten's market cap. It would probably trade on a higher P/E ratio if it had a lot of cash, but I doubt it is having a big impact.

The Verdict On Alten's P/E Ratio

Alten has a P/E of 22.7. That's higher than the average in its market, which is 17.7. Given the debt is only modest, and earnings are already moving in the right direction, it's not surprising that the market expects continued improvement.

Investors have an opportunity when market expectations about a stock are wrong. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ENXTPA:ATE

Alten

Operates as an engineering and technology consultancy company in France, North America, Germany, Scandinavia, Benelux, Iberian, Spain, Italy, the United Kingdom, the Asia-Pacific, Switzerland, Eastern Europe, and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor