Advertisement

Alten SA is a financially healthy and robust stock with a proven track record of outperformance. We all know Alten, and having this large-cap to cushion your portfolio during a volatile period in the stock market isn't a bad idea. Today I will give a high-level overview of the stock, and why I believe it's still attractive.

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

View our latest analysis for Alten

Alten SA operates as an engineering and technology consultancy company primarily in France, North America, Germany, Scandinavia, Spain, the United Kingdom, Italy, Belgium, the Netherlands, and the Asia-Pacific. Formed in 1988, and headed by CEO Simon Azoulay, the company now has 33.70k employees and with the company's market cap sitting at €3.1b, it falls under the mid-cap group. Generally, large-cap stocks are well-resourced and well-established meaning that a bear market will cause it to rejig some short-term capital allocations, but stock market volatility is hardly detrimental to its financial health and business operations. Therefore large-cap stocks are a safe bet to buy more of when the wider market is going down and down.

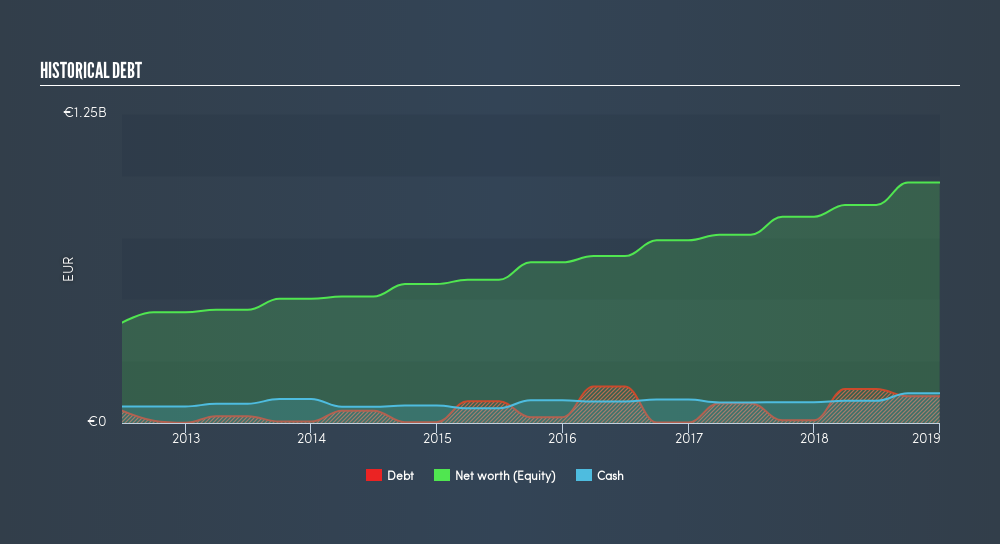

Alten currently has €108m debt on its books which requires regular servicing. This means it needs to have sufficient cash-on-hand to meet upcoming interest expenses. With an interest coverage ratio of 190x, Alten produces sufficient earnings (EBIT) to cover its interest payments. Anything above 3x is considered safe practice. Moreover, its cash flows from operations copiously covers it debt by 92%, which is higher than the bare minimum requirement of 20%. Not to mention, it meets the basic liquidity requirement with current assets exceeding liabilities, which further builds on its financial strength in the face of a volatile market.

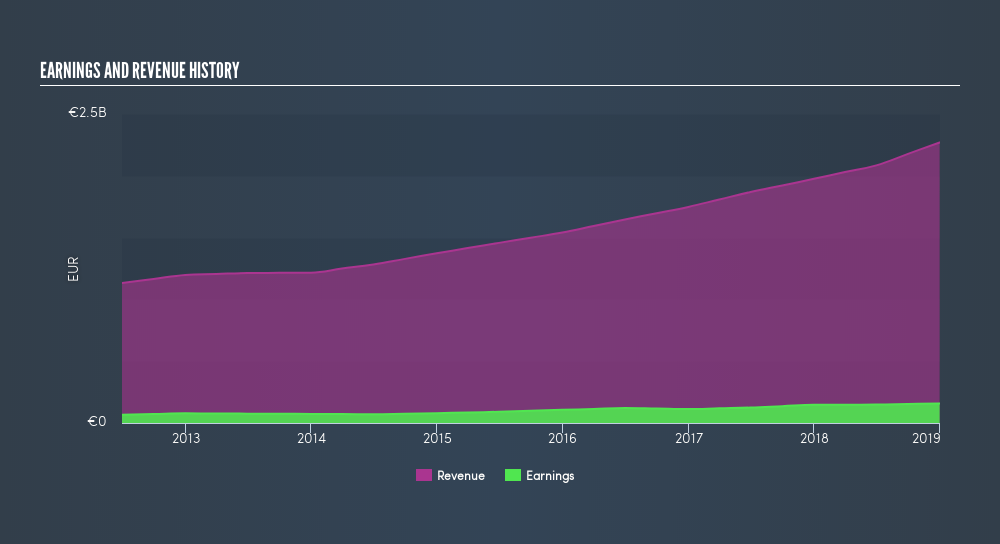

ATE’s year-on-year earnings growth has been positive over the past five years, with an average annual growth rate of 17%, outperfoming the market growth rate of 12%. It has also returned an ROE of 17% recently, above the industry return of 11%. Alten's strong performance over time is a demonstration of its ability to grow through cycles, raising my confidence in the company as a long-term investment.

Next Steps:

Alten makes for a robust long-term investment based on its scale, financial health and track record. Remember, in bear markets, sell-offs can be unjustified. Ask yourself, has anything really changed with Alten? If not, then why not scoop it up at a discount? Lining your portfolio with a few well-established companies can reduce your risk and help you scale your wealth in the long run. One thing you should remember though, is to do your homework. Do your own research, come up with your point of view. Below is a list I've put together of other things you should consider before you buy:- Future Outlook: What are well-informed industry analysts predicting for ATE’s future growth? Take a look at our free research report of analyst consensus for ATE’s outlook.

- Valuation: What is ATE worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether ATE is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:ATE

Alten

Operates as an engineering and technology consultancy company in France, North America, Germany, Scandinavia, Benelux, Iberian, Spain, Italy, the United Kingdom, the Asia-Pacific, Switzerland, Eastern Europe, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor