Advertisement

Wedia SA (EPA:ALWED), is not the largest company out there, but it led the ENXTPA gainers with a relatively large price hike in the past couple of weeks. Less-covered, small caps tend to present more of an opportunity for mispricing due to the lack of information available to the public, which can be a good thing. So, could the stock still be trading at a low price relative to its actual value? Let’s examine Wedia’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

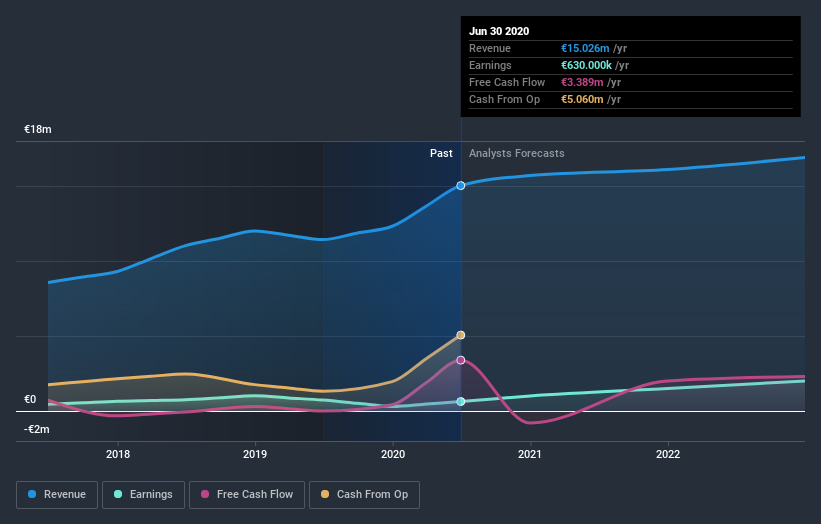

See our latest analysis for Wedia

What's the opportunity in Wedia?

The stock seems fairly valued at the moment according to my valuation model. It’s trading around 0.30% above my intrinsic value, which means if you buy Wedia today, you’d be paying a relatively fair price for it. And if you believe that the stock is really worth €35.89, there’s only an insignificant downside when the price falls to its real value. Furthermore, Wedia’s low beta implies that the stock is less volatile than the wider market.

What does the future of Wedia look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to more than double over the next couple of years, the future seems bright for Wedia. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? It seems like the market has already priced in ALWED’s positive outlook, with shares trading around its fair value. However, there are also other important factors which we haven’t considered today, such as the financial strength of the company. Have these factors changed since the last time you looked at the stock? Will you have enough confidence to invest in the company should the price drop below its fair value?

Are you a potential investor? If you’ve been keeping tabs on ALWED, now may not be the most advantageous time to buy, given it is trading around its fair value. However, the optimistic prospect is encouraging for the company, which means it’s worth further examining other factors such as the strength of its balance sheet, in order to take advantage of the next price drop.

In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example - Wedia has 3 warning signs we think you should be aware of.

If you are no longer interested in Wedia, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

When trading Wedia or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wedia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:ALWED

Wedia

Engages in publishing of digital asset management software in France and internationally.

Adequate balance sheet low.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor