Advertisement

MEMSCAP, S.A. (EPA:MEMS) shareholders might be concerned after seeing the share price drop 16% in the last quarter. On the other hand the share price is higher than it was three years ago. In that time, it is up 15%, which isn't bad, but not amazing either.

See our latest analysis for MEMSCAP

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

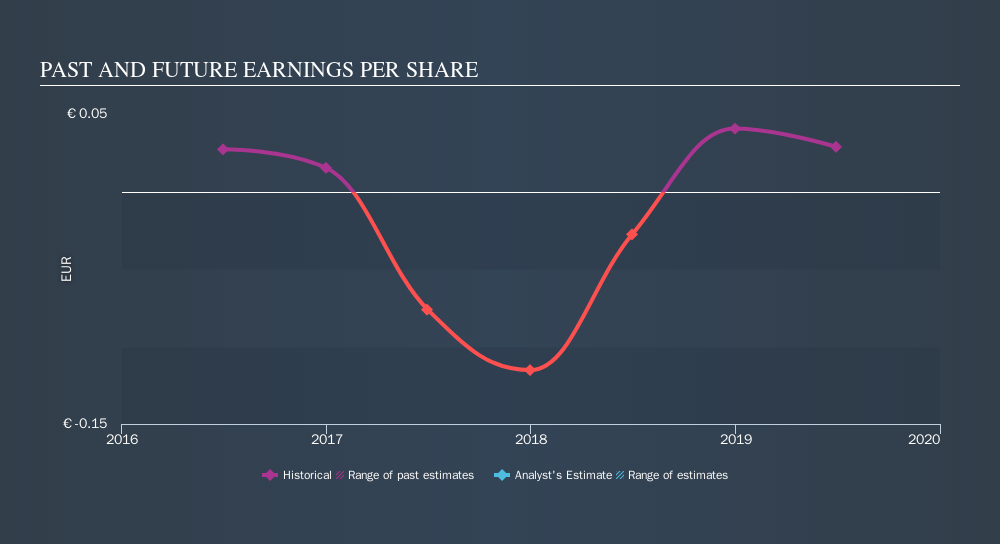

MEMSCAP became profitable within the last three years. So we would expect a higher share price over the period.

You can see below how EPS has changed over time.

It might be well worthwhile taking a look at our free report on MEMSCAP's earnings, revenue and cash flow.

A Different Perspective

Investors in MEMSCAP had a tough year, with a total loss of 11%, against a market gain of about 16%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 0.6% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. Before deciding if you like the current share price, check how MEMSCAP scores on these 3 valuation metrics.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on FR exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:MEMS

MEMSCAP

Provides micro-electro-mechanical systems (MEMS) based solutions for aerospace and defense, optical communications, medical, and biomedical markets worldwide.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor