Rémy Cointreau (ENXTPA:RCO) Revises Earnings Guidance for FY 2025-26

Reviewed by Simply Wall St

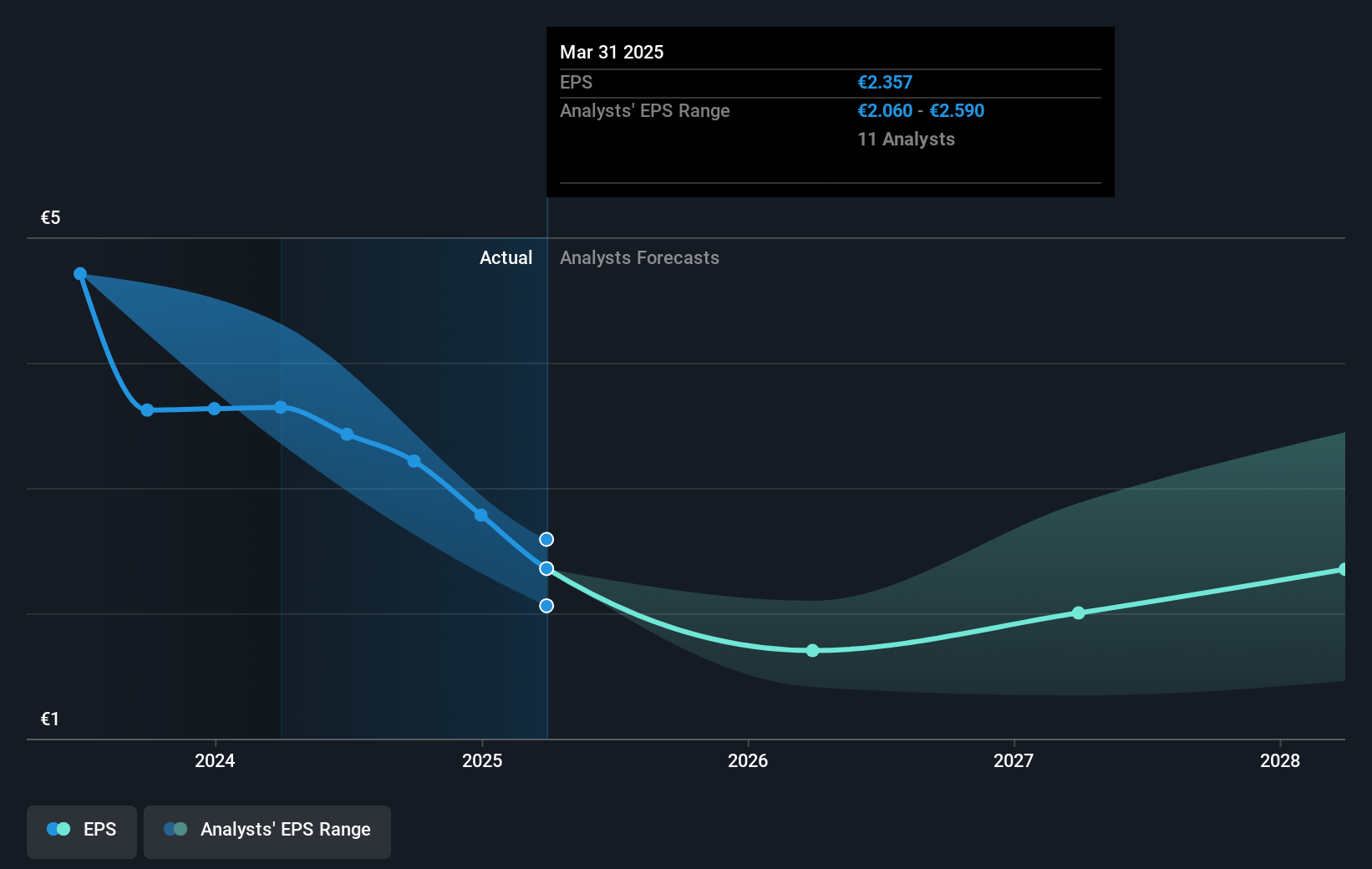

Rémy Cointreau (ENXTPA:RCO) recently revised its earnings guidance for fiscal year 2025-26, lowering its expectations while still targeting mid-single-digit organic sales growth, driven by a rebound in U.S. sales. Despite this, the company's share price declined 8% over the last quarter. The downward guidance and adjustments in expected tariff impacts likely weighed on investor sentiment. Additionally, a dividend decrease and changes in the board composition, although important for governance, did not seem to provide enough positive momentum to counter broader market trends, which have been broadly positive, reflecting investor optimism on interest rate cuts and other factors.

The recent downward revision in Rémy Cointreau's earnings guidance, combined with an 8% quarterly share price decline, may challenge the company's efforts to stabilize its financials. This news could further pressure revenue and earnings forecasts, which are already undergoing scrutiny from analysts due to macroeconomic challenges and rising production costs. The company's focus on U.S. and China markets for future growth may need reevaluation if current conditions persist.

Over the longer period of the past year, Rémy Cointreau experienced a total shareholder return of 24.32% decline, signaling a tougher environment when compared to the French market, which gained 3.9% over the same period. Furthermore, the company underperformed the French Beverage industry, which saw a decline of 23.9% in one year. These comparative performances highlight the challenges Rémy Cointreau faces amid broader market trends.

The current share price stands at €47.42, whereas the analyst consensus price target is €54.07, reflecting a discount of approximately 14% from the target. This gap indicates varied analyst expectations about the company's ability to improve its earnings to reach €146.2 million by 2028. If realized, the firm would need to trade at a PE ratio of 22.7x, contrasting with the current beverage industry average of 19.2x. It highlights the company's relative valuation complexities amid its ambitious growth targets.

Jump into the full analysis health report here for a deeper understanding of Rémy Cointreau.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:RCO

Rémy Cointreau

Engages in the production, sale, and distribution of liqueurs and spirits.

Excellent balance sheet and slightly overvalued.

Market Insights

Community Narratives