Advertisement

- France

- /

- Energy Services

- /

- ENXTPA:VK

Should You Reconsider Vallourec After Its 13% Monthly Rally in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

If you are weighing your next move on Vallourec stock, you are in good company. The stock has been drawing renewed attention thanks to some sharp price moves in recent months. With a closing price of €16.89, Vallourec has delivered a steady 3.2% gain over just the past week, and over the past month, it is up an impressive 13.8%. Stepping back, the growth looks even stronger. Vallourec is up 29.2% over the last year and an eye-opening 222.9% across five years. These numbers show that the market’s perception of Vallourec’s prospects is shifting, as global energy and metals demand fluctuates and investors appear to be recognizing its long-term potential.

Of course, the big question is whether there is still value left in the stock, or if the best gains have already happened. This is where things get interesting. By most recognized valuation criteria, Vallourec currently earns a score of 5 out of 6 on the value scale, suggesting the stock is undervalued across a broad set of professional checks. That is not something you see every day, especially from a company that has already delivered such strong returns.

So how do these valuation approaches compare when it comes to Vallourec? And is there an even more insightful way to view value that investors often overlook? Let us break down the numbers and see where the real opportunities might lie.

Why Vallourec is lagging behind its peers

Approach 1: Vallourec Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a forward-looking valuation method that estimates a company's intrinsic value by projecting its anticipated future cash flows and then discounting them back to today's value. This helps investors determine what the business is fundamentally worth, regardless of its current share price.

For Vallourec, the DCF approach begins with its latest reported Free Cash Flow, totaling €375.3 million. Analyst consensus suggests this figure will continue to climb, with estimates projecting €475.5 million by 2028. Beyond the next five years, longer-term projections extrapolated from these estimates forecast Free Cash Flow to taper gradually, though remaining above €400 million annually across most of the following decade.

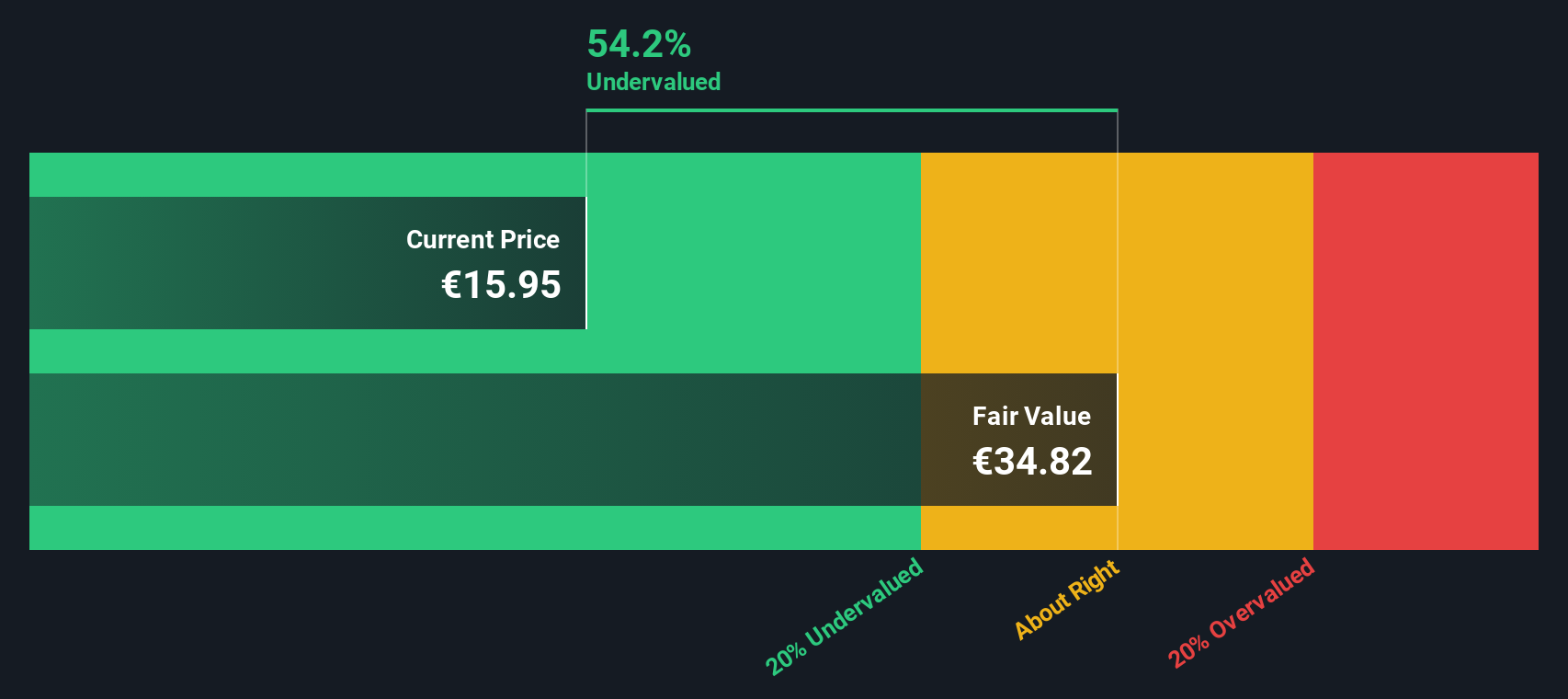

After discounting all those expected future cash flows to reflect their present value, the DCF model calculates Vallourec's intrinsic value per share at €29.60. With the current market price at €16.89, this implies the stock is trading at a substantial 43.0% discount to its estimated fair value. According to this model, Vallourec appears significantly undervalued by the market.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Vallourec is undervalued by 43.0%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

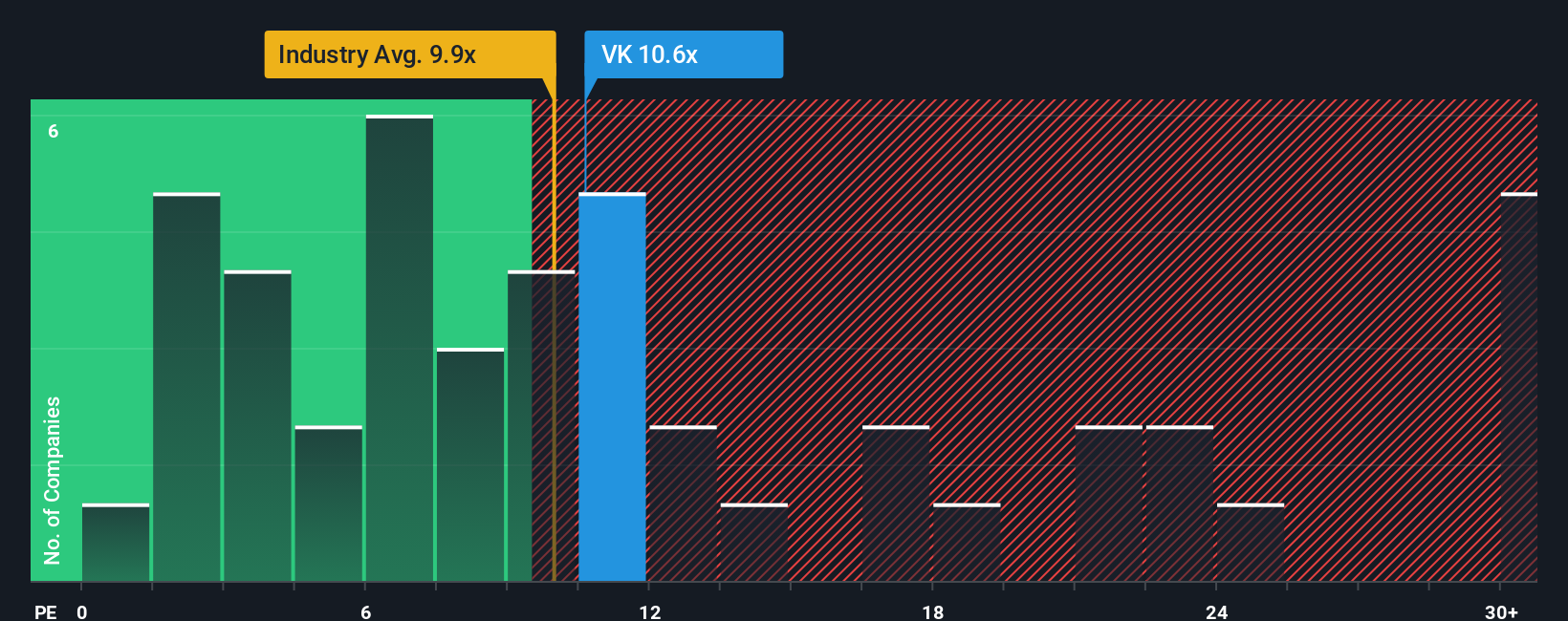

Approach 2: Vallourec Price vs Earnings

The Price-to-Earnings (PE) ratio is a favored metric for valuing profitable companies like Vallourec because it connects the stock price directly to its ability to generate profits. Investors generally prefer this ratio when assessing established firms with steady earnings, as it offers a straightforward comparison between valuation and actual company performance.

The "normal" or "fair" PE ratio for a company is not set in stone, as it depends on factors like future earnings growth, perceived business risk, and general market sentiment. Fast-growing companies or those with lower perceived risk often command higher PE ratios, while slower growth or riskier companies will generally trade at lower PE multiples.

Vallourec currently trades at a PE ratio of 11.1x. To put this into context, the average for its Energy Services industry peers is 14.1x. Similar companies in the peer set average 13.5x. This suggests Vallourec is valued more conservatively by the market relative to these benchmarks, reflecting tempered expectations or distinct company-specific risks.

Simply Wall St’s proprietary “Fair Ratio” tailors the PE multiple specifically to Vallourec’s situation, blending in forward-looking growth, profit margins, the company’s market capitalization, and sector-specific trends. Unlike a straightforward industry or peer average, the Fair Ratio (13.9x) is much more nuanced and offers a personalized view of what a reasonable market valuation should look like for Vallourec.

Comparing Vallourec’s actual PE of 11.1x to its Fair Ratio of 13.9x, the shares appear notably undervalued, with the market pricing them well below what would be expected given company trends and sector norms.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Vallourec Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your personal way of telling the story behind a company like Vallourec, connecting your perspective about its future revenue, earnings, and margins to a financial forecast and a fair value. This approach brings real meaning to all the numbers you see.

Think of Narratives as easy-to-use tools available on Simply Wall St’s Community page. These tools are designed so you can combine your view of Vallourec’s strategy, industry shifts, or risks with actual financial assumptions in just a few clicks. When you draft a Narrative, you get a tailored Fair Value for Vallourec, which you can then compare directly with the current share price to help you decide if it is time to buy, hold, or sell.

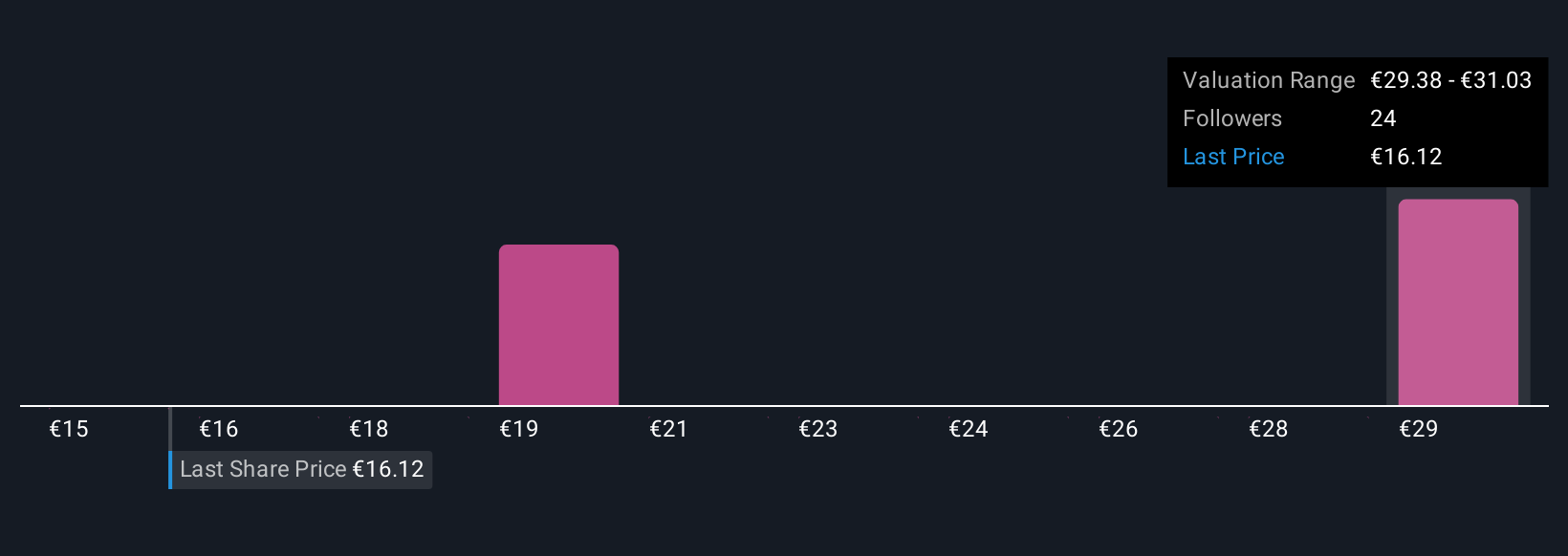

Narratives are kept up to date automatically whenever new information emerges, such as company results or breaking industry news, so you never lose track of how your investment thesis stacks up. For example, one investor might see Vallourec as a beneficiary of Brazil’s cost reductions and U.S. tariffs on steel, justifying a higher fair value above €22.6. Another may focus on oil dependence and FX risk, leading to a more cautious estimate below €18.8.

Do you think there's more to the story for Vallourec? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:VK

Vallourec

Through its subsidiaries, provides tubular solutions for the oil and gas, industry, and new energies markets in Europe, North America, South America, Asia, the Middle East, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor