- France

- /

- Capital Markets

- /

- ENXTPA:ANTIN

Antin Infrastructure Partners SAS (EPA:ANTIN) Will Pay A €0.37 Dividend In Four Days

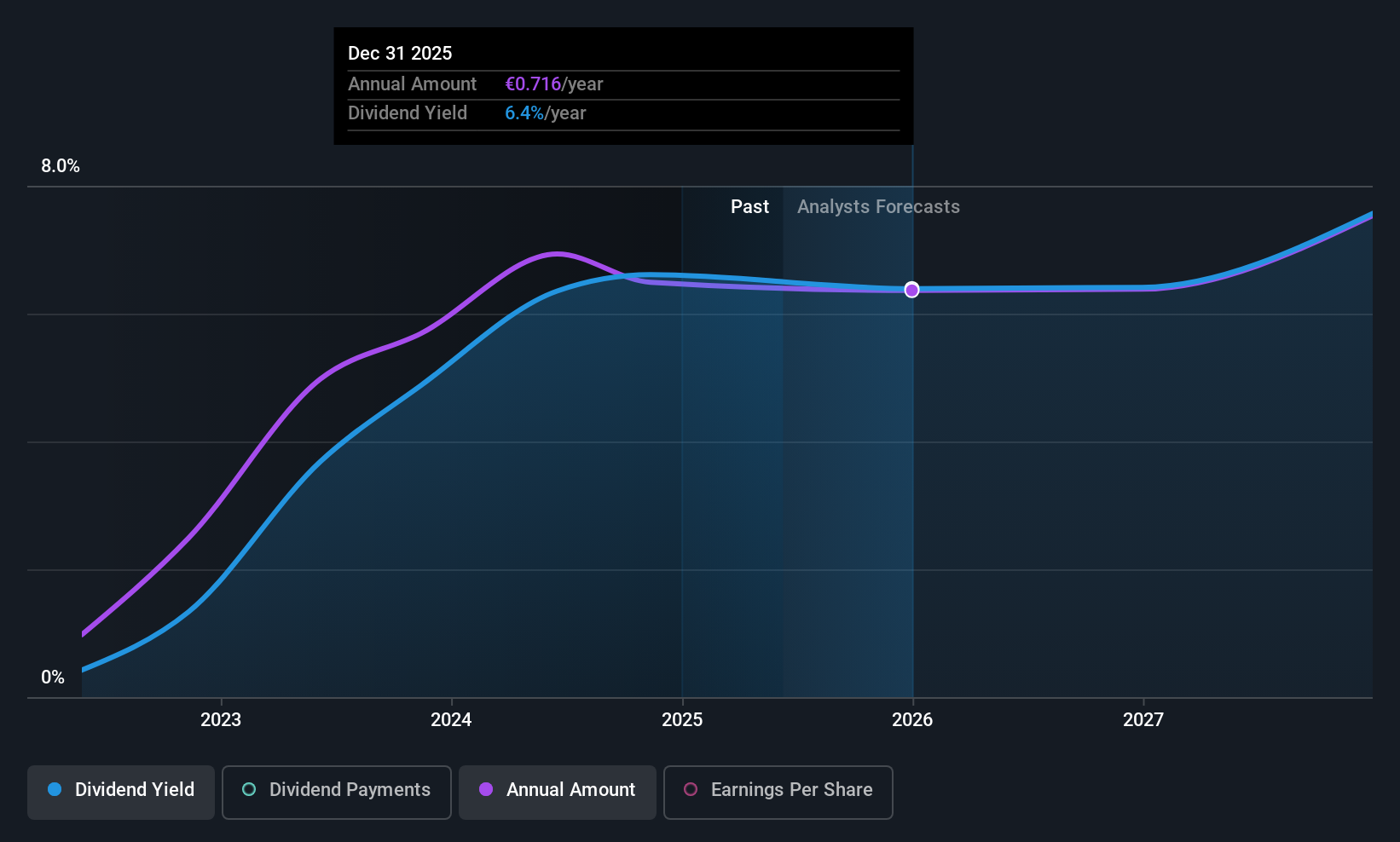

Antin Infrastructure Partners SAS (EPA:ANTIN) stock is about to trade ex-dividend in four days. The ex-dividend date is commonly two business days before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Accordingly, Antin Infrastructure Partners SAS investors that purchase the stock on or after the 16th of June will not receive the dividend, which will be paid on the 18th of June.

The company's upcoming dividend is €0.37 a share, following on from the last 12 months, when the company distributed a total of €0.71 per share to shareholders. Based on the last year's worth of payments, Antin Infrastructure Partners SAS has a trailing yield of 6.3% on the current stock price of €11.20. If you buy this business for its dividend, you should have an idea of whether Antin Infrastructure Partners SAS's dividend is reliable and sustainable. So we need to investigate whether Antin Infrastructure Partners SAS can afford its dividend, and if the dividend could grow.

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Last year, Antin Infrastructure Partners SAS paid out 96% of its income as dividends, which is above a level that we're comfortable with, especially if the company needs to reinvest in its business.

When a company pays out a dividend that is not well covered by profits, the dividend is generally seen as more vulnerable to being cut.

View our latest analysis for Antin Infrastructure Partners SAS

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings fall far enough, the company could be forced to cut its dividend. That's why it's comforting to see Antin Infrastructure Partners SAS's earnings have been skyrocketing, up 55% per annum for the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the past three years, Antin Infrastructure Partners SAS has increased its dividend at approximately 86% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

The Bottom Line

Has Antin Infrastructure Partners SAS got what it takes to maintain its dividend payments? It's been growing earnings per share at a pleasant rate, although its dividend payout was not well covered by earnings. At best we would put it on a watch-list to see if business conditions improve, as it doesn't look like a clear opportunity right now.

If you want to look further into Antin Infrastructure Partners SAS, it's worth knowing the risks this business faces. For example, we've found 1 warning sign for Antin Infrastructure Partners SAS that we recommend you consider before investing in the business.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:ANTIN

Antin Infrastructure Partners SAS

A private equity firm specializing in infrastructure investments.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion