Advertisement

Assessing LVMH’s Valuation as Digital Expansion Shapes Market Sentiment in 2025

Simply Wall St

Reviewed by Bailey Pemberton

- Curious whether LVMH Moët Hennessy Louis Vuitton Société Européenne is a bargain or just reflecting its luxury status? You're not alone, as plenty of investors are eyeing its potential for future growth and value.

- The stock has seen a modest rebound lately, climbing 2.6% over the past week and up 8.6% year-over-year, but remains slightly below its year-to-date starting point.

- Recent headlines have spotlighted LVMH's strategic expansions into new markets and its ongoing investment in digital experiences, both of which have shaped market sentiment and contributed to the latest price movements. Investors are watching closely as the company continues to set trends and consolidate its leadership in the luxury sector through bold moves like acquisitions and collaborations.

- As for valuation, LVMH currently scores just 2 out of 6 on our value checks. We’ll unpack this figure using classic and alternative valuation methods next, and there’s an even smarter way to look at value coming up at the end of this article.

LVMH Moët Hennessy - Louis Vuitton Société Européenne scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: LVMH Moët Hennessy Louis Vuitton Société Européenne Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) method is a widely used valuation model that estimates the present value of a company by projecting its future cash flows and discounting them back to today. This approach aims to determine what the company is fundamentally worth based on how much cash it is expected to generate for its shareholders.

Currently, LVMH Moët Hennessy Louis Vuitton Société Européenne reports a last twelve months Free Cash Flow (FCF) of approximately €13.3 billion. Analysts provide detailed cash flow estimates for the next five years, with projections showing a slight dip to €12.8 billion by 2029. Beyond this period, Simply Wall St extrapolates up to ten years, with estimated FCF ranging from about €12.0 billion in 2026 to over €13.1 billion by 2035.

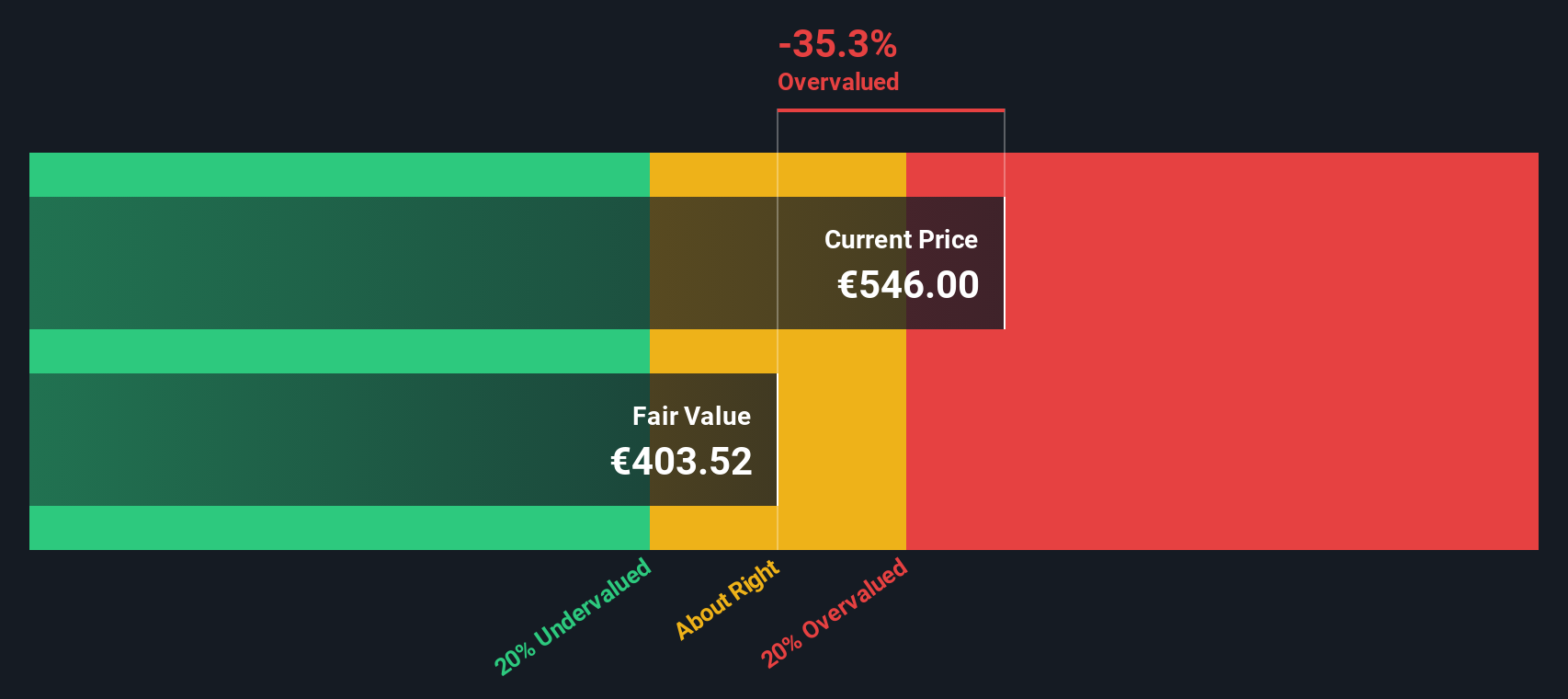

Based on these projections, the DCF model calculates the company's intrinsic value at €364.01 per share. Compared to the current market price, this valuation suggests that LVMH shares are trading at a 71.8% premium to their DCF-based intrinsic value.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests LVMH Moët Hennessy - Louis Vuitton Société Européenne may be overvalued by 71.8%. Discover 926 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: LVMH Moët Hennessy Louis Vuitton Société Européenne Price vs Earnings

The Price-to-Earnings (PE) ratio is often the preferred metric for valuing established, consistently profitable companies like LVMH Moët Hennessy Louis Vuitton Société Européenne. This ratio tells investors how much they are paying for each euro of earnings, and is particularly useful because it connects the company's bottom line performance directly to its share price.

When evaluating PE ratios, it is important to remember that factors like future earnings growth, risk, and company quality influence what counts as a normal or fair multiple. Generally, higher anticipated growth and lower risk justify higher PE ratios, while slower-growing or riskier companies tend to command lower multiples.

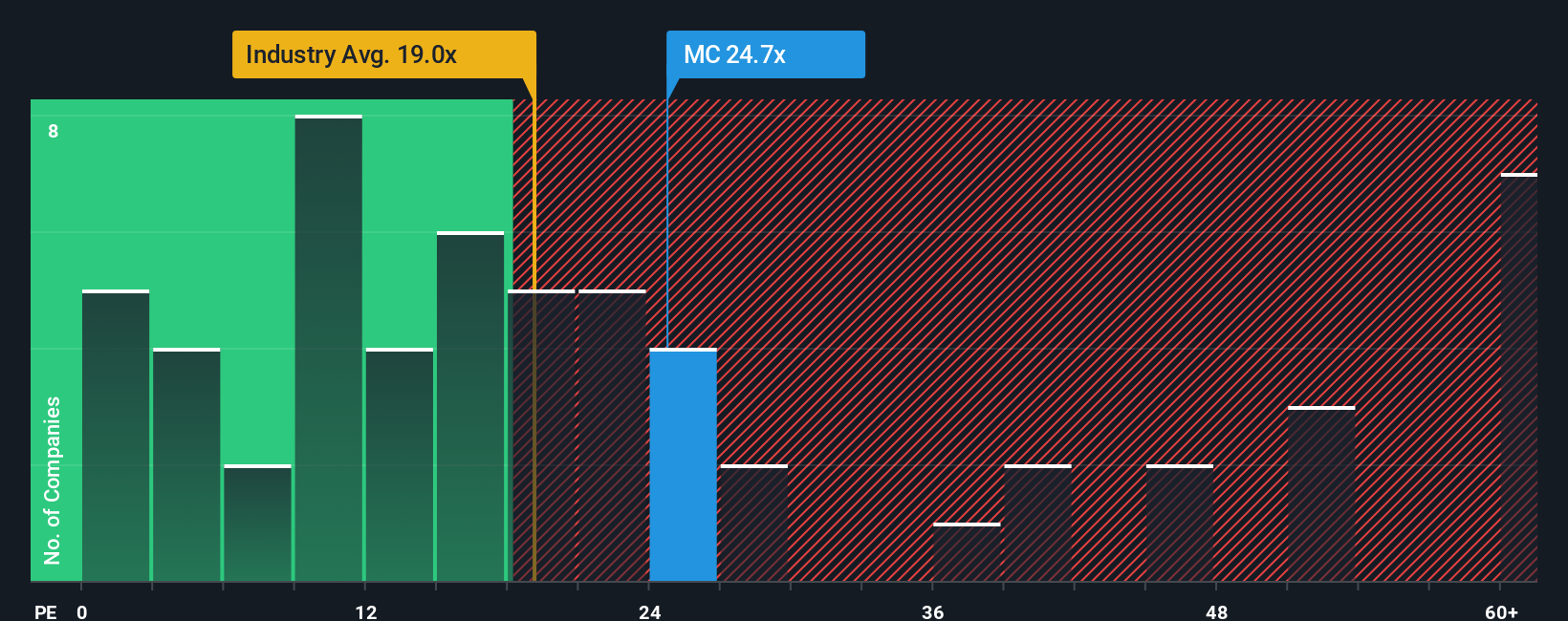

LVMH currently trades at a PE ratio of 28.3x. This is higher than the Luxury industry average of 17.5x, but notably below its peer average of 37.9x. Such context suggests LVMH’s valuation sits between other leading luxury firms and the broader sector standard, reflecting its unique place in the market.

Simply Wall St’s proprietary “Fair Ratio” for LVMH is 33.1x. This fair ratio is calculated with a more holistic lens than a simple industry or peer comparison, factoring in company-specific attributes like forecast growth, risk profile, profitability, company size, and the nuances of its market. That means Simply Wall St’s fair ratio arguably offers a more tailored and relevant benchmark for this stock.

Because LVMH’s actual PE (28.3x) is moderately below its fair PE (33.1x), the stock currently looks undervalued using this approach.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your LVMH Moët Hennessy - Louis Vuitton Société Européenne Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple but powerful tool that lets you define the story behind LVMH’s numbers by providing your perspective on how the company will perform in the future, including your own estimates for revenue, earnings, margins, and fair value.

Unlike traditional models that focus only on past data or analyst averages, Narratives connect your view of the company’s story directly to a financial forecast and a resulting fair value. Narratives are accessible right on Simply Wall St’s Community page, used by millions of investors. This makes it easy to see different viewpoints and share your own.

Narratives allow you to compare your Fair Value directly to the current Price, and are dynamically updated whenever important company information changes, such as new earnings releases or breaking news.

For example, recent Narratives on LVMH reflect a wide range of views. Some investors are optimistic, forecasting earnings per share above €30 and a fair value near €720 per share, while others are more cautious, estimating lower future earnings and a fair value closer to €435. The range demonstrates how Narratives let you see the logic and assumptions behind every price target and choose the one that fits your own outlook.

Do you think there's more to the story for LVMH Moët Hennessy - Louis Vuitton Société Européenne? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:MC

LVMH Moët Hennessy - Louis Vuitton Société Européenne

Operates as a luxury goods company worldwide.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative