Advertisement

- France

- /

- Aerospace & Defense

- /

- ENXTPA:SAF

Safran (ENXTPA:SAF) Valuation Spotlight as 100% Sustainable Aviation Fuel Milestone Nears

Simply Wall St

Reviewed by Simply Wall St

Safran (ENXTPA:SAF) is making headlines as it partners with Bell to complete over 700 hours of flight tests using Sustainable Aviation Fuel in the Bell 505. The company’s helicopter engines will soon be able to operate on 100% SAF, which signals a clear move toward greater sustainability in the industry.

See our latest analysis for Safran.

As Safran pushes deeper into sustainable aviation tech, investors have taken notice, with its share price climbing more than 34% year-to-date, backed by a robust 34% total shareholder return over the past year. The long-term momentum is just as impressive, with a three-year total return topping 150%, suggesting that optimism is building around Safran’s ability to navigate new industry challenges and opportunities.

If you’re interested in other companies shaping the future of aerospace and defense, there’s never been a better time to explore See the full list for free.

With the stock up strongly this year and trading just below analyst targets, is Safran undervalued given its innovation in sustainable aviation, or is the market already factoring in its future growth potential?

Most Popular Narrative: 12% Undervalued

Safran’s widely followed narrative points to a fair value above its last close price, reflecting strategic optimism about future growth and margin resilience. With analysts factoring in upcoming catalysts and robust sector tailwinds, the current share price appears to lag their broader outlook.

The recent acquisition of Collins' actuation and flight control assets, along with other targeted acquisitions and strategic partnerships, will broaden Safran's mission-critical offering, drive cost synergies through 2028, and further diversify revenue streams. This is expected to result in higher EBIT margins and more stable earnings.

Want to know which bold strategy shifts are behind this valuation? The forecast depends on major boosts to free cash flow, new tech bets, and a game-changing margin play. Discover how all the pieces fit together in the full breakdown and see which financial projections hold the key.

Result: Fair Value of €328.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing supply chain pressures and significant integration challenges from recent acquisitions could still threaten Safran’s projected earnings momentum and valuation upside.

Find out about the key risks to this Safran narrative.

Another View: Multiple Approach Challenges the Outlook

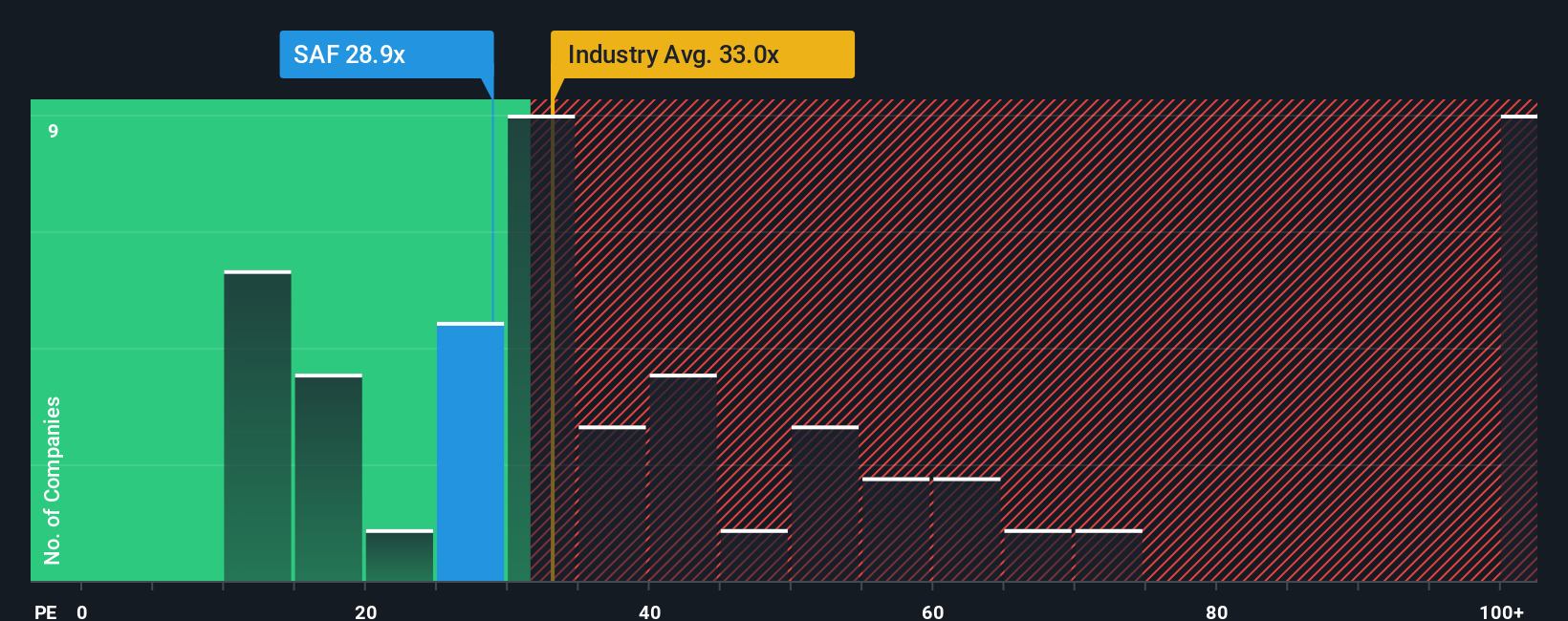

Taking a look through the lens of the price-to-earnings ratio, Safran appears well-priced compared to both its direct peers and the industry average. However, it trades above its fair ratio (27.9x vs 27x). This small premium suggests there could be less upside left than the growth narrative implies. Is the current optimism already priced in, or is there still room for a surprise?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Safran Narrative

If you’d rather dig into the numbers yourself or believe there’s a different story waiting to be told, you can craft your own in just minutes: Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Safran.

Ready for More Winning Investment Ideas?

Do not stop at one opportunity. The Simply Wall Street Screener gives you the edge to act fast and catch high-potential stocks before everyone else does.

- Catch high-yielding options with strong income potential by assessing these 15 dividend stocks with yields > 3% offering yields above 3% for reliable cash flow.

- Uncover exciting companies tackling the future of medicine by tapping into these 30 healthcare AI stocks blending artificial intelligence with innovative healthcare solutions.

- Capitalize on hidden value by targeting these 928 undervalued stocks based on cash flows that the market has yet to fully appreciate, based on robust cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:SAF

Safran

Engages in the aerospace and defense businesses in France, rest of Europe, the Americas, the Asia-Pacific, Africa, and the Middle East.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

77 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative