Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Enertime SA (EPA:ALENE) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Enertime

What Is Enertime's Debt?

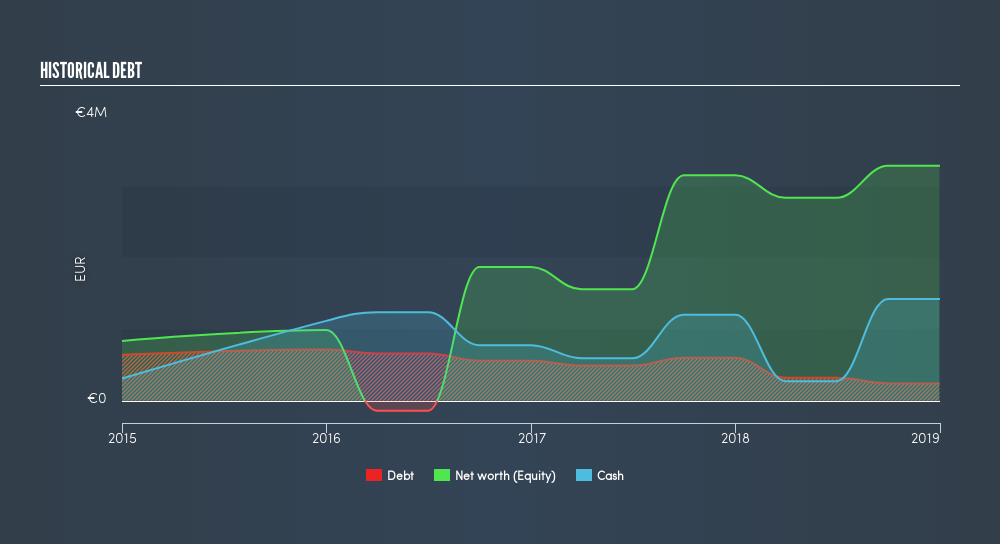

You can click the graphic below for the historical numbers, but it shows that Enertime had €241.5k of debt in December 2018, down from €598.1k, one year before However, it does have €1.42m in cash offsetting this, leading to net cash of €1.18m.

How Strong Is Enertime's Balance Sheet?

We can see from the most recent balance sheet that Enertime had liabilities of €1.95m falling due within a year, and liabilities of €352.5k due beyond that. On the other hand, it had cash of €1.42m and €1.91m worth of receivables due within a year. So it actually has €1.03m more liquid assets than total liabilities.

This excess liquidity suggests that Enertime is taking a careful approach to debt. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Enertime boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Enertime can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Enertime actually shrunk its revenue by 36%, to €3.1m. That makes us nervous, to say the least.

So How Risky Is Enertime?

By their very nature companies that are losing money are more risky than those with a long history of profitability. Anf the fact is that over the last twelve months Enertime lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through €451k of cash and made a loss of €1.3m. While this does make the company a bit risky, it's important to remember it has net cash of €1.4m. That means it could keep spending at its current rate for more than two years. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Enertime's profit, revenue, and operating cashflow have changed over the last few years.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:ALENE

Enertime

Engages in the design, development, and implementation of Organic Rankine Cycle (ORC) modules to produce renewable or CO2-free electricity from heat.

Moderate and overvalued.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor