Advertisement

- Finland

- /

- Retail Distributors

- /

- HLSE:WUF1V

Wulff-Yhtiöt Oyj (HEL:WUF1V) Surges 27% Yet Its Low P/E Is No Reason For Excitement

Wulff-Yhtiöt Oyj (HEL:WUF1V) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 34% in the last twelve months.

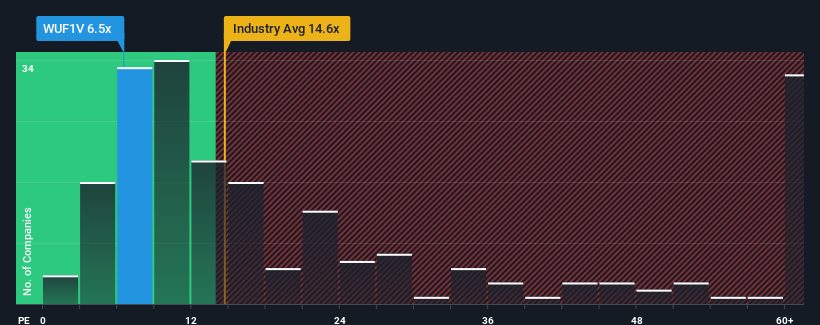

Although its price has surged higher, Wulff-Yhtiöt Oyj may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 6.5x, since almost half of all companies in Finland have P/E ratios greater than 19x and even P/E's higher than 32x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

There hasn't been much to differentiate Wulff-Yhtiöt Oyj's and the market's retreating earnings lately. One possibility is that the P/E is low because investors think the company's earnings may begin to slide even faster. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. At the very least, you'd be hoping that earnings don't fall off a cliff if your plan is to pick up some stock while it's out of favour.

View our latest analysis for Wulff-Yhtiöt Oyj

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as depressed as Wulff-Yhtiöt Oyj's is when the company's growth is on track to lag the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 7.5%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 27% overall rise in EPS. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been mostly respectable for the company.

Turning to the outlook, the next three years should generate growth of 10% per annum as estimated by the lone analyst watching the company. With the market predicted to deliver 16% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that Wulff-Yhtiöt Oyj's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Wulff-Yhtiöt Oyj's P/E?

Shares in Wulff-Yhtiöt Oyj are going to need a lot more upward momentum to get the company's P/E out of its slump. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Wulff-Yhtiöt Oyj's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Wulff-Yhtiöt Oyj (at least 1 which is a bit concerning), and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on Wulff-Yhtiöt Oyj, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Wulff-Yhtiöt Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:WUF1V

Wulff-Yhtiöt Oyj

Provides workplace products, IT supplies, ergonomics, printing, international exhibition, and event services in Finland, Sweden, Norway, Denmark, other European countries, and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor