Advertisement

BBS-Bioactive Bone Substitutes Oyj (HEL:BONEH) Is Making Moderate Use Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, BBS-Bioactive Bone Substitutes Oyj (HEL:BONEH) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for BBS-Bioactive Bone Substitutes Oyj

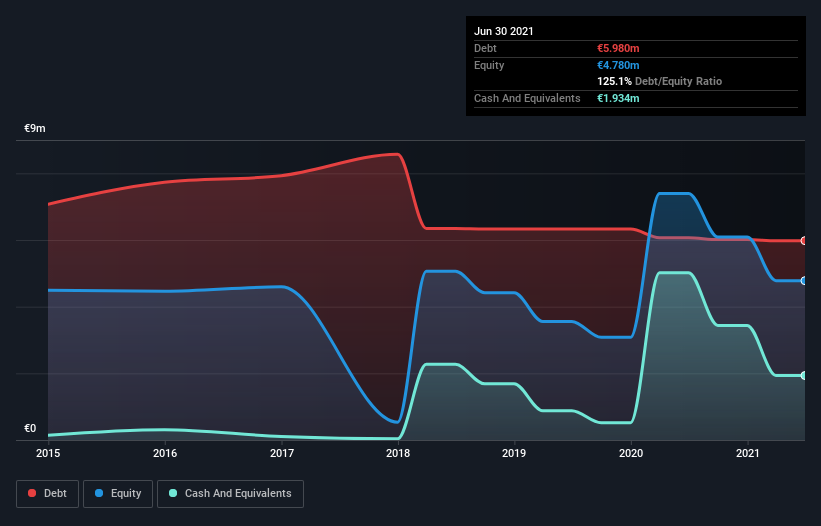

What Is BBS-Bioactive Bone Substitutes Oyj's Net Debt?

As you can see below, BBS-Bioactive Bone Substitutes Oyj had €5.98m of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. However, it also had €1.93m in cash, and so its net debt is €4.05m.

A Look At BBS-Bioactive Bone Substitutes Oyj's Liabilities

The latest balance sheet data shows that BBS-Bioactive Bone Substitutes Oyj had liabilities of €1.43m due within a year, and liabilities of €5.09m falling due after that. On the other hand, it had cash of €1.93m and €330.3k worth of receivables due within a year. So it has liabilities totalling €4.26m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since BBS-Bioactive Bone Substitutes Oyj has a market capitalization of €14.9m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since BBS-Bioactive Bone Substitutes Oyj will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Given its lack of meaningful operating revenue, BBS-Bioactive Bone Substitutes Oyj shareholders no doubt hope it can fund itself until it has a profitable product.

Caveat Emptor

Over the last twelve months BBS-Bioactive Bone Substitutes Oyj produced an earnings before interest and tax (EBIT) loss. Its EBIT loss was a whopping €2.5m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled €3.0m in negative free cash flow over the last twelve months. So in short it's a really risky stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 6 warning signs for BBS-Bioactive Bone Substitutes Oyj (3 are concerning!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if BBS-Bioactive Bone Substitutes Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:BONEH

BBS-Bioactive Bone Substitutes Oyj

A biomedical technology company, develops, manufactures, and commercializes bioactive medical devices and implants for orthopedic surgery in Finland.

Medium-low with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor