Advertisement

We Think Keskisuomalainen Oyj (HEL:KSLAV) Has A Fair Chunk Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Keskisuomalainen Oyj (HEL:KSLAV) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Keskisuomalainen Oyj

What Is Keskisuomalainen Oyj's Debt?

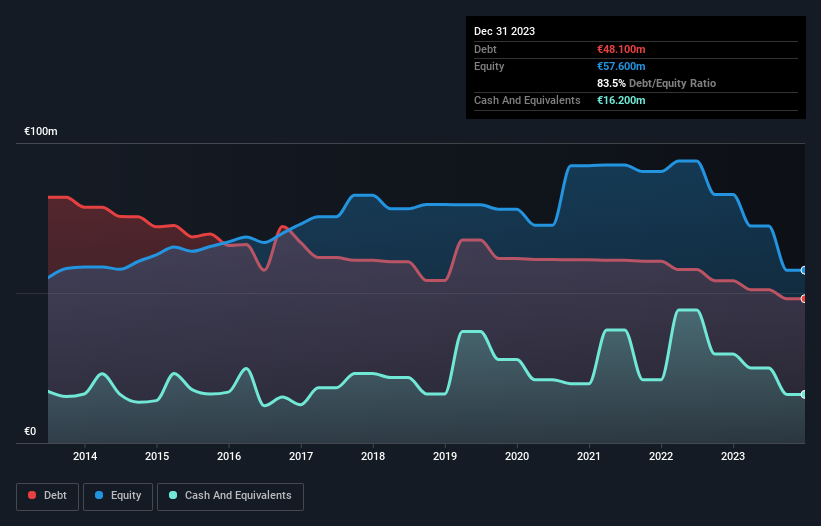

The image below, which you can click on for greater detail, shows that Keskisuomalainen Oyj had debt of €48.1m at the end of December 2023, a reduction from €54.1m over a year. However, it does have €16.2m in cash offsetting this, leading to net debt of about €31.9m.

How Healthy Is Keskisuomalainen Oyj's Balance Sheet?

According to the last reported balance sheet, Keskisuomalainen Oyj had liabilities of €54.1m due within 12 months, and liabilities of €48.4m due beyond 12 months. On the other hand, it had cash of €16.2m and €16.6m worth of receivables due within a year. So its liabilities total €69.7m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of €95.8m, so it does suggest shareholders should keep an eye on Keskisuomalainen Oyj's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Keskisuomalainen Oyj will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Keskisuomalainen Oyj had a loss before interest and tax, and actually shrunk its revenue by 5.6%, to €209m. That's not what we would hope to see.

Caveat Emptor

Importantly, Keskisuomalainen Oyj had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable €14m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. We would feel better if it turned its trailing twelve month loss of €13m into a profit. In the meantime, we consider the stock very risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 3 warning signs for Keskisuomalainen Oyj (2 don't sit too well with us) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Keskisuomalainen Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:KSL

Keskisuomalainen Oyj

Engages in publishing, printing, and distributing newspapers and magazines in Finland.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|48.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.4% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|19.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|53.6% overvalued

RO

Community Contributor