Why It Might Not Make Sense To Buy Wärtsilä Oyj Abp (HEL:WRT1V) For Its Upcoming Dividend

Wärtsilä Oyj Abp (HEL:WRT1V) stock is about to trade ex-dividend in 3 days time. Investors can purchase shares before the 19th of September in order to be eligible for this dividend, which will be paid on the 27th of September.

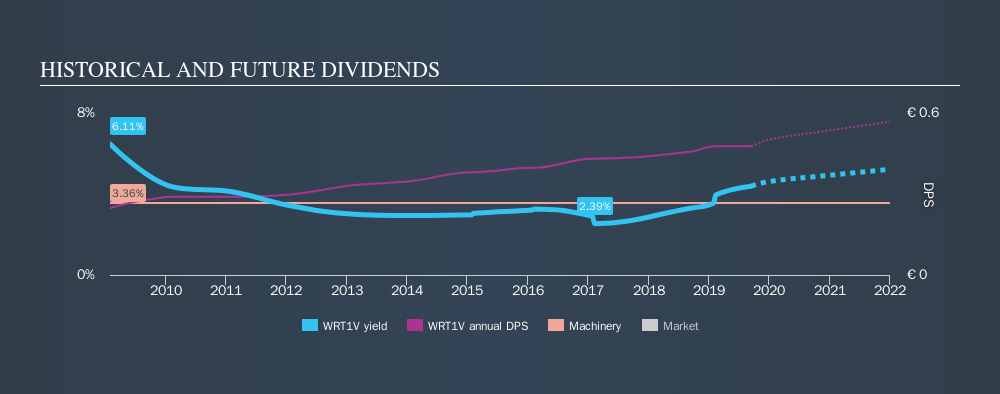

Wärtsilä Oyj Abp's upcoming dividend is €0.24 a share, following on from the last 12 months, when the company distributed a total of €0.48 per share to shareholders. Calculating the last year's worth of payments shows that Wärtsilä Oyj Abp has a trailing yield of 4.1% on the current share price of €11.595. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. As a result, readers should always check whether Wärtsilä Oyj Abp has been able to grow its dividends, or if the dividend might be cut.

View our latest analysis for Wärtsilä Oyj Abp

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Its dividend payout ratio is 76% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth We'd be worried about the risk of a drop in earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out 78% of its free cash flow as dividends, which is within usual limits but will limit the company's ability to lift the dividend if there's no growth.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. So we're not too excited that Wärtsilä Oyj Abp's earnings are down 2.3% a year over the past five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, ten years ago, Wärtsilä Oyj Abp has lifted its dividend by approximately 6.7% a year on average. Growing the dividend payout ratio while earnings are declining can deliver nice returns for a while, but it's always worth checking for when the company can't increase the payout ratio any more - because then the music stops.

The Bottom Line

Should investors buy Wärtsilä Oyj Abp for the upcoming dividend? It's never good to see earnings per share shrinking, but at least the dividend payout ratios appear reasonable. We're aware though that if earnings continue to decline, the dividend could be at risk. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Curious what other investors think of Wärtsilä Oyj Abp? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About HLSE:WRT1V

Wärtsilä Oyj Abp

Offers technologies and lifecycle solutions for the marine and energy markets worldwide.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion