- Spain

- /

- Electric Utilities

- /

- BME:IBE

Is It Too Late to Consider Iberdrola After Its Strong Multi Year Share Price Rally?

Reviewed by Bailey Pemberton

- Wondering if Iberdrola is still good value after its strong run, or if you might be late to the party? You are not alone. This is exactly what we are going to unpack.

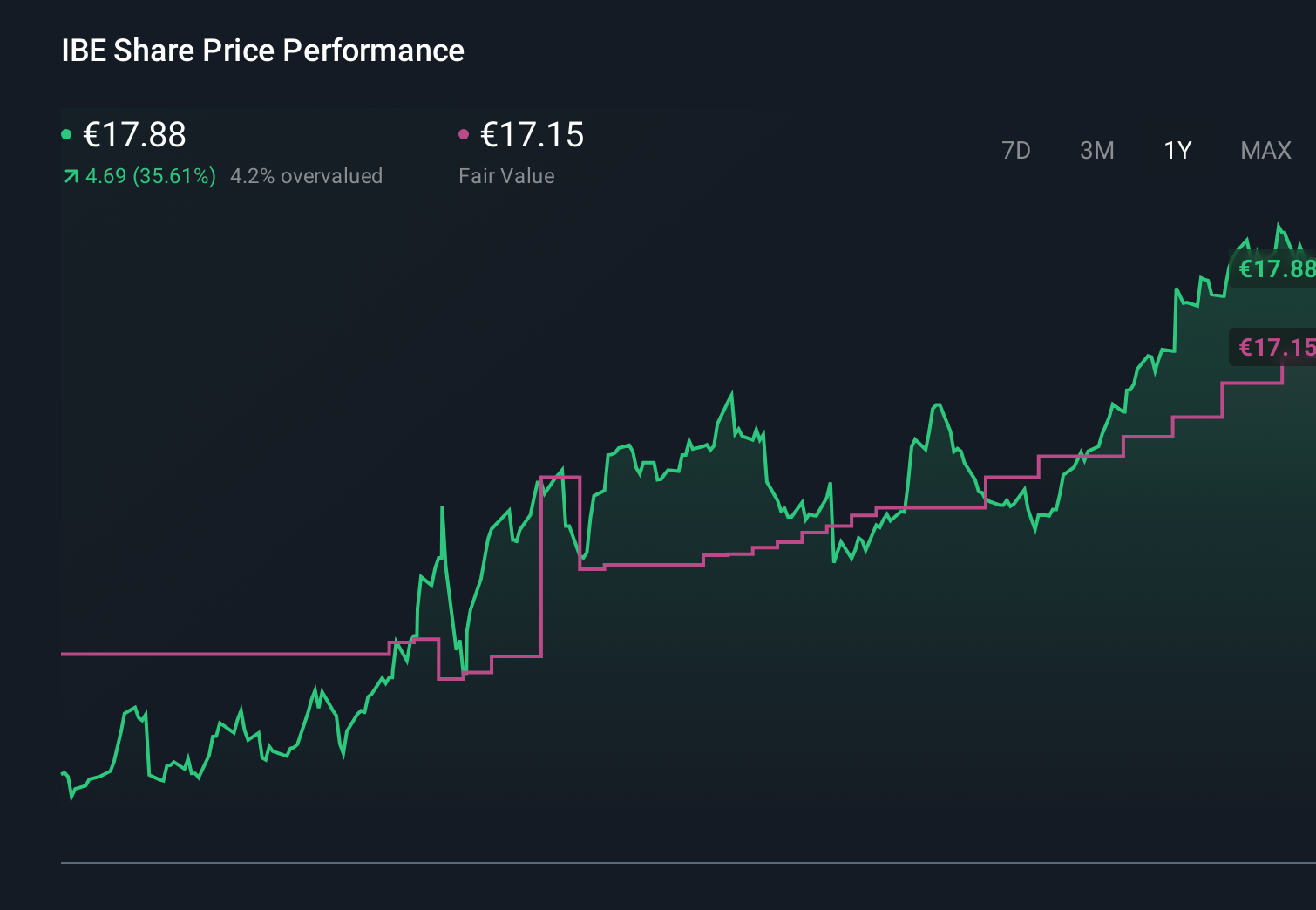

- The stock has barely moved over the last week, dipping about 0.2%, but zoom out and it is up 0.8% over 30 days, 33.1% year to date, 43.0% over 1 year, and an impressive 85.1% over 3 years and 84.0% over 5 years.

- Those gains have been underpinned by Iberdrola leaning into the global push for renewables, with ongoing investment in grid upgrades and clean energy projects across Europe and the United States. At the same time, supportive regulatory frameworks for green infrastructure and the company’s role in major offshore wind and transmission initiatives have helped investors reassess its growth and risk profile.

- Yet, on our numbers Iberdrola only scores 0 out of 6 on valuation checks for being undervalued. Next we will walk through what different valuation methods say about the stock, and why there may be an even better way to think about what Iberdrola is really worth by the end of this article.

Iberdrola scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Iberdrola Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today.

For Iberdrola, the latest twelve month Free Cash Flow is about €5.0 billion. Analysts expect cash flows to remain positive but to trend lower, with Simply Wall St extending those forecasts beyond the formal analyst horizon using its 2 Stage Free Cash Flow to Equity framework. By 2027, Free Cash Flow is projected to be roughly €0.32 billion, and the model then tapers growth further over the following years as the business matures.

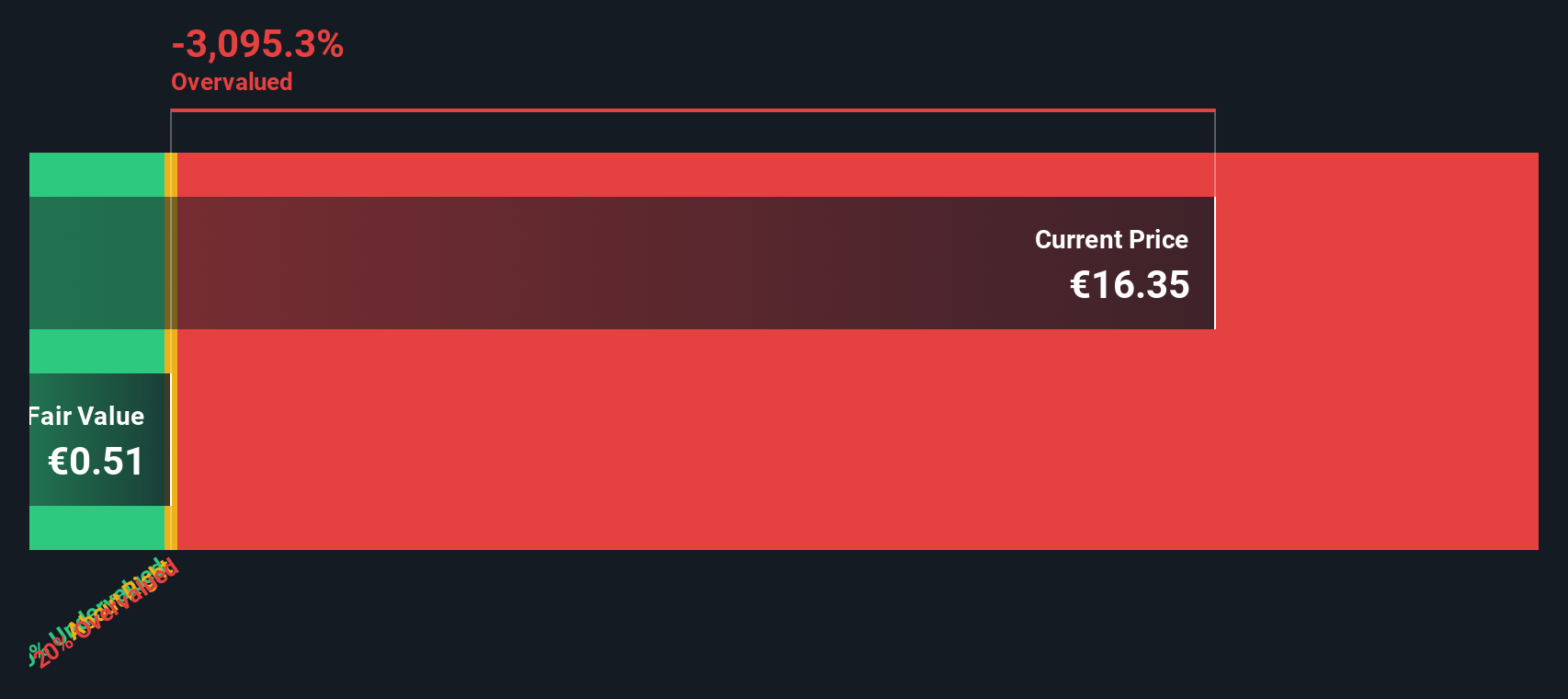

When all those projected cash flows are discounted back to today, the DCF model arrives at an intrinsic value of about €0.36 per share. Compared with the current share price, this implies Iberdrola is roughly 4853.1% overvalued on a cash flow basis, a large gap that suggests the market is pricing in far stronger or more durable cash generation than this model assumes.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Iberdrola may be overvalued by 4853.1%. Discover 899 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Iberdrola Price vs Earnings

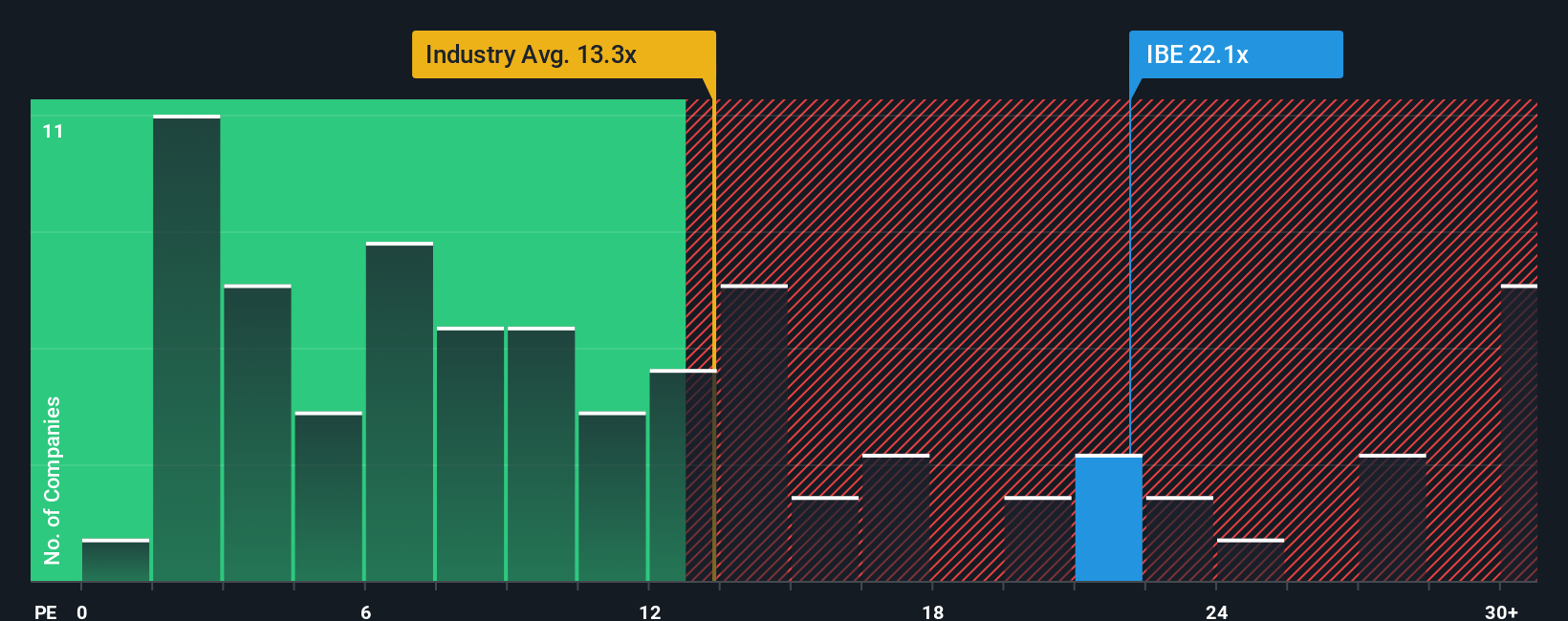

For profitable, established companies like Iberdrola, the price to earnings, or PE, ratio is a straightforward way to gauge whether investors are paying a reasonable price for each euro of profit. What counts as a normal PE depends on how fast earnings are expected to grow and how risky those earnings are, with faster growth and lower risk typically justifying a higher multiple.

Iberdrola currently trades on a PE of 22.70x, which is notably higher than both the Electric Utilities industry average of about 14.35x and the peer average of 13.73x. To go a step further, Simply Wall St’s Fair Ratio framework estimates what PE you might expect for Iberdrola given its earnings growth outlook, margins, risk profile, industry and market cap. This produces a Fair Ratio of 19.95x, which is more tailored to Iberdrola’s fundamentals than a simple comparison with peers or the sector.

With the actual PE sitting above the Fair Ratio, the shares look somewhat expensive relative to what its fundamentals justify on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1458 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Iberdrola Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Iberdrola’s story with a concrete forecast for its future revenue, earnings and margins, and then a Fair Value that you can compare with today’s share price to inform your decision. On Simply Wall St’s Community page, used by millions of investors, a Narrative is essentially your investment story written into the numbers. You spell out why you think, for example, Iberdrola’s expanding regulated networks and green projects will support stronger growth and justify a Fair Value near €18.5. Alternatively, if you are more cautious about regulation and execution risks, you can set out why your assumptions lead to a much lower Fair Value closer to €9.7. Because Narratives are updated dynamically as fresh news, earnings and analyst revisions come in, they stay current and make it easier to monitor how far your Fair Value sits above or below the live market price and to consider acting when the gap becomes large enough for you.

Do you think there's more to the story for Iberdrola? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BME:IBE

Iberdrola

Engages in the generation, production, transmission, distribution, and supply of electricity in Spain, the United Kingdom, the United States, Mexico, Brazil, Germany, France, and Australia.

Average dividend payer with mediocre balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion