Advertisement

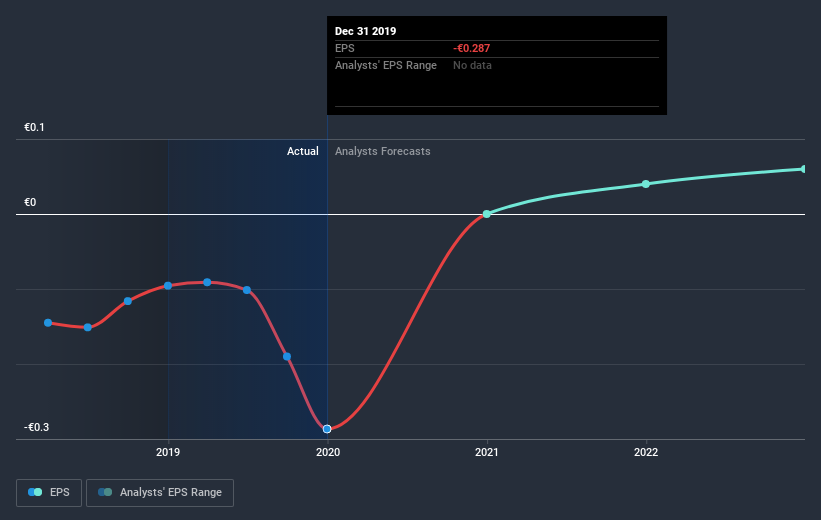

We feel now is a pretty good time to analyse Pangaea Oncology, S.A.'s (BME:PANG) business as it appears the company may be on the cusp of a considerable accomplishment. Pangaea Oncology, S.A., a medical services company, provides a range of services to cancer patients, and pharmaceutical and biotech clients worldwide. The €28m market-cap company announced a latest loss of €4.8m on 31 December 2019 for its most recent financial year result. The most pressing concern for investors is Pangaea Oncology's path to profitability – when will it breakeven? In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

Check out our latest analysis for Pangaea Oncology

Pangaea Oncology is bordering on breakeven, according to some Spanish Life Sciences analysts. They expect the company to post a final loss in 2020, before turning a profit of €700k in 2021. Therefore, the company is expected to breakeven roughly 12 months from now or less. At what rate will the company have to grow in order to realise the consensus estimates forecasting breakeven in under 12 months? Using a line of best fit, we calculated an average annual growth rate of 109%, which is rather optimistic! If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

We're not going to go through company-specific developments for Pangaea Oncology given that this is a high-level summary, however, bear in mind that generally a life science company has lumpy cash flows which are contingent on the product and stage of development the company is in. So, a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before we wrap up, there’s one issue worth mentioning. Pangaea Oncology currently has a relatively high level of debt. Typically, debt shouldn’t exceed 40% of your equity, which in Pangaea Oncology's case is 45%. A higher level of debt requires more stringent capital management which increases the risk around investing in the loss-making company.

Next Steps:

There are key fundamentals of Pangaea Oncology which are not covered in this article, but we must stress again that this is merely a basic overview. For a more comprehensive look at Pangaea Oncology, take a look at Pangaea Oncology's company page on Simply Wall St. We've also put together a list of essential aspects you should look at:

- Valuation: What is Pangaea Oncology worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Pangaea Oncology is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Pangaea Oncology’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you decide to trade Pangaea Oncology, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BME:PANG

Pangaea Oncology

A medical services company, provides a range of services to cancer patients in Spain and the rest of European Union countries.

Adequate balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative