Advertisement

- Spain

- /

- Hospitality

- /

- BME:AMS

Amadeus IT Group's (BME:AMS) Returns Have Hit A Wall

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after investigating Amadeus IT Group (BME:AMS), we don't think it's current trends fit the mold of a multi-bagger.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Amadeus IT Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

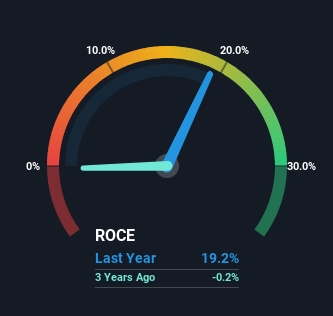

0.19 = €1.7b ÷ (€12b - €3.0b) (Based on the trailing twelve months to December 2024).

Thus, Amadeus IT Group has an ROCE of 19%. In absolute terms, that's a satisfactory return, but compared to the Hospitality industry average of 15% it's much better.

View our latest analysis for Amadeus IT Group

Above you can see how the current ROCE for Amadeus IT Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Amadeus IT Group .

What The Trend Of ROCE Can Tell Us

Over the past five years, Amadeus IT Group's ROCE and capital employed have both remained mostly flat. This tells us the company isn't reinvesting in itself, so it's plausible that it's past the growth phase. So don't be surprised if Amadeus IT Group doesn't end up being a multi-bagger in a few years time. With fewer investment opportunities, it makes sense that Amadeus IT Group has been paying out a decent 48% of its earnings to shareholders. Unless businesses have highly compelling growth opportunities, they'll typically return some money to shareholders.

The Bottom Line

We can conclude that in regards to Amadeus IT Group's returns on capital employed and the trends, there isn't much change to report on. Since the stock has gained an impressive 64% over the last five years, investors must think there's better things to come. Ultimately, if the underlying trends persist, we wouldn't hold our breath on it being a multi-bagger going forward.

One more thing to note, we've identified 2 warning signs with Amadeus IT Group and understanding them should be part of your investment process.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:AMS

Amadeus IT Group

Operates as a transaction processor for the travel and tourism industry in Europe, Central and South America, the Middle East, Africa, and Asia Pacific.

Good value with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.672.0% undervalued

40 followersusers have followed this narrative

2 commentsusers have commented on this narrative

20 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2685.7% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3410.9% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

CE

Ceazar on Sparc Al ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on MSCI ·

MSCI 04-2026

Fair Value:US$267112.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WI

WIn2026 on CoreWeave ·

Deep Dive: Assessing the Sustainability of CRWV’s Compute-as-a-Service Model

Fair Value:US$7067.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.8% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5727.9% undervalued

1372 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GT

GT1 on Gulf Keystone Petroleum ·

Have been in and out of this one and Genel for years. I think that delayed and non payments are a bi...

0

|0