Advertisement

CaixaBank, S.A. (BME:CABK) Passed Our Checks, And It's About To Pay A €0.12 Dividend

It looks like CaixaBank, S.A. (BME:CABK) is about to go ex-dividend in the next three days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. This means that investors who purchase CaixaBank's shares on or after the 14th of April will not receive the dividend, which will be paid on the 20th of April.

The company's next dividend payment will be €0.12 per share. Last year, in total, the company distributed €0.15 to shareholders. Based on the last year's worth of payments, CaixaBank has a trailing yield of 4.5% on the current stock price of €3.235. If you buy this business for its dividend, you should have an idea of whether CaixaBank's dividend is reliable and sustainable. As a result, readers should always check whether CaixaBank has been able to grow its dividends, or if the dividend might be cut.

Check out our latest analysis for CaixaBank

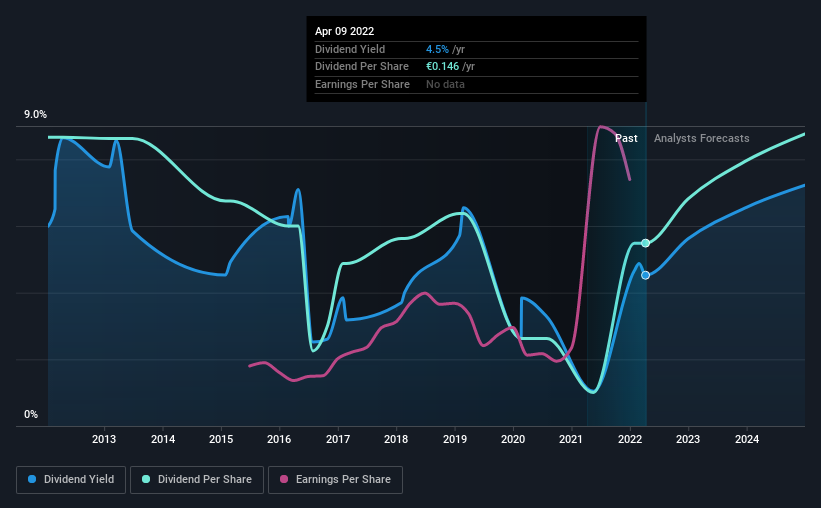

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. CaixaBank is paying out just 22% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events.

Companies that pay out less in dividends than they earn in profits generally have more sustainable dividends. The lower the payout ratio, the more wiggle room the business has before it could be forced to cut the dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. It's encouraging to see CaixaBank has grown its earnings rapidly, up 28% a year for the past five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. CaixaBank has seen its dividend decline 4.5% per annum on average over the past 10 years, which is not great to see. It's unusual to see earnings per share increasing at the same time as dividends per share have been in decline. We'd hope it's because the company is reinvesting heavily in its business, but it could also suggest business is lumpy.

The Bottom Line

Has CaixaBank got what it takes to maintain its dividend payments? Typically, companies that are growing rapidly and paying out a low fraction of earnings are keeping the profits for reinvestment in the business. This is one of the most attractive investment combinations under this analysis, as it can create substantial value for investors over the long run. In summary, CaixaBank appears to have some promise as a dividend stock, and we'd suggest taking a closer look at it.

On that note, you'll want to research what risks CaixaBank is facing. Every company has risks, and we've spotted 4 warning signs for CaixaBank (of which 1 is a bit unpleasant!) you should know about.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:CABK

CaixaBank

Provides various banking products and financial services in Spain and internationally.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor