Ringkjøbing Landbobank (CPSE:RILBA) has delivered a steady performance lately, drawing interest from investors evaluating its recent returns and sustained profitability. Shares have seen moderate moves, which invites a closer look at fundamental trends and valuation.

After a strong run-up earlier this year, Ringkjøbing Landbobank’s share price has cooled in recent weeks, hinting that investor momentum is pausing as the market waits for fresh catalysts. Despite this dip, long-term shareholders are still enjoying an impressive 24.43% total return over the past year, with gains compounding to 196.48% over five years. This serves as a reminder that patient investors have been well rewarded.

If you’re scouting for other stocks with potential for strong long-term returns and insider conviction, broaden your horizons with our fast moving fast growing stocks with high insider ownership.

With shares trading below analyst targets and its recent dip, is Ringkjøbing Landbobank now undervalued, or has the market already priced in all of the company’s future growth possibilities?

Advertisement

Price-to-Earnings of 15.1x: Is it justified?

Ringkjøbing Landbobank is currently trading at a price-to-earnings (P/E) ratio of 15.1x, which is noticeably higher than both its industry peers and fair value benchmarks.

The price-to-earnings ratio helps investors assess how much they are paying for each unit of current earnings. For a bank like Ringkjøbing Landbobank, this metric signals the market's expectations for future growth, profitability and risk.

A P/E ratio of 15.1x stands out when set against the Danish banks peer average of 9.6x and the European banks industry average of 9.8x, suggesting the stock commands a premium. According to our fair P/E estimate of 10.9x, the market is valuing the company well above where its earnings profile alone might justify, hinting that other factors such as quality of profits or management strength may be influencing investor sentiment.

However, risks such as lower-than-expected revenue growth or sudden shifts in banking sector sentiment could quickly alter the current valuation outlook.

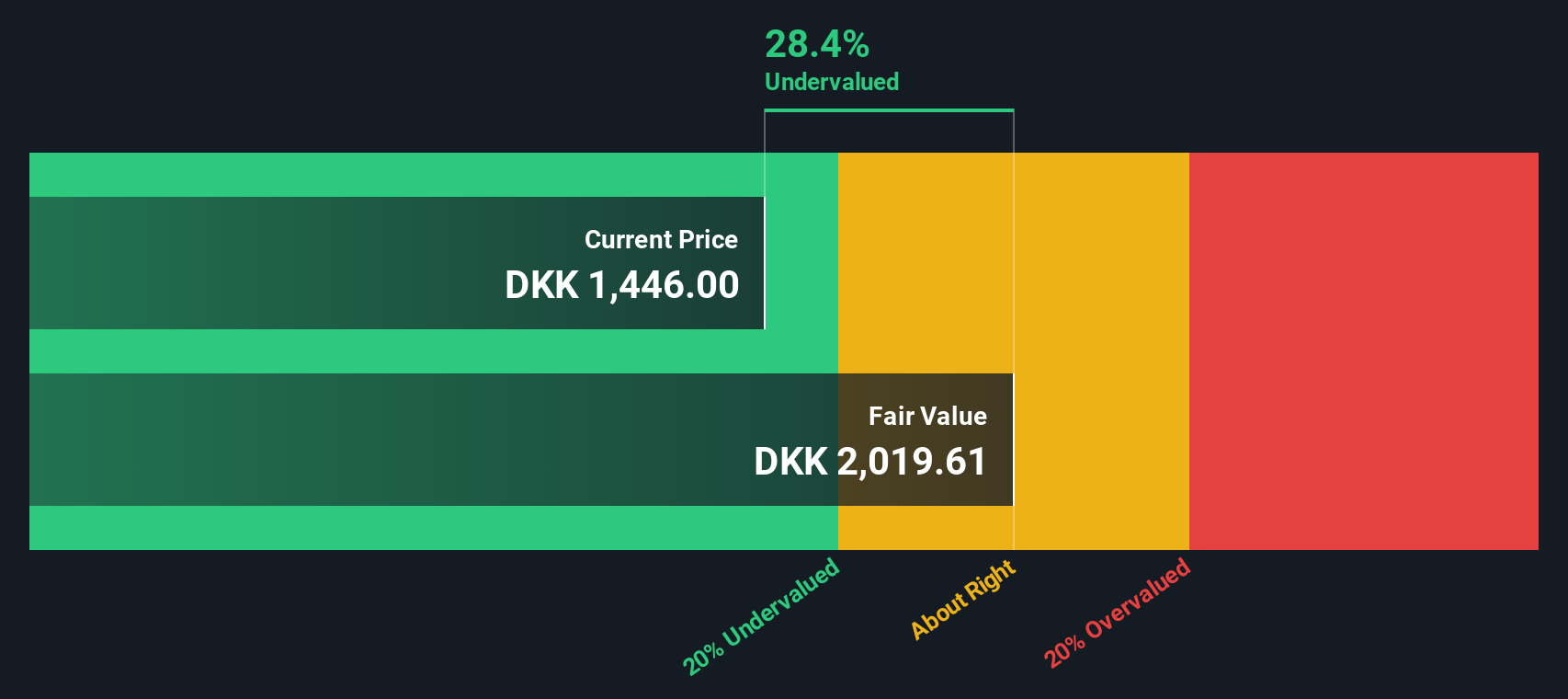

While the current price-to-earnings ratio suggests Ringkjøbing Landbobank may be expensive relative to peers and historic norms, our SWS DCF model offers a very different view. According to this methodology, shares are trading at a 35.5% discount to fair value, which implies the market may be underpricing the company’s future cash flows. Could this mean there is more upside if long-term fundamentals play out?

If these conclusions do not quite align with your perspective or you'd rather take a hands-on approach, you can explore the numbers and craft your own story for Ringkjøbing Landbobank in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Ringkjøbing Landbobank.

Looking for more investment ideas?

Don’t let opportunity pass you by. Expand your investing toolkit with stock ideas that target strong growth, innovation, and future income streams.

Tap into the power of artificial intelligence by tracking these 27 AI penny stocks. These are gaining momentum as AI reshapes entire industries and market trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies